Charts of the Week

Current Economic Trends from 15 to 19 July 2019: labour market, wages, construction, current account of the balance of payments and Slovenian industrial producer prices

The improvement in labour market conditions continues, while employment growth has moderated somewhat. The hiring of foreign labour, amid labour shortages, is strengthening. Demographic trends, alongside economic factors and the increase in the minimum wage, are contributing to wage growth in the private sector. Favourable company performance, with the lack of building in previous years and increased investment activity in the public and private sectors, is reflected in the high level of activity in construction.

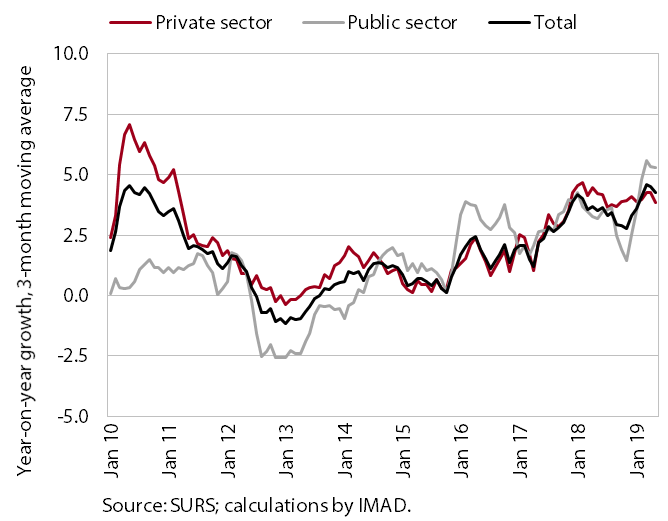

Labour market, May–June 2019

Labour market conditions continue to improve, albeit at a slower pace than in previous years. In the first five months, the number of employed persons increased (3.0%) somewhat less than in the same period of last year (3.5%) – the most in manufacturing and construction. Labour shortages, amid high labour demand, are reflected in increased hiring of foreigners, who already contribute more than two-thirds to total employment growth. In the first half of the year, the number of the registered unemployed declined further. It was 70,747 at the end of June, 5.7% lower than in the same period of last year.

Wages, May 2019

In the first five months, year-on-year wage growth was higher than in the same period of last year. In the private sector, wage growth was – in addition to economic and demographic factors (good business results, labour shortages and thus upward pressure on wages) – also due to the increase in the minimum wage at the beginning of the year. Wages rose the most in the sectors with the greatest labour shortages and a high share of minimum wage recipients (administrative and support service activities, accommodation and food service activities, trade, and manufacturing). In the public sector, wage growth mainly reflected strong growth in the government sector as a result of the agreed wage rises at the end of last year and, to a lesser extent, the increase in the minimum wage.

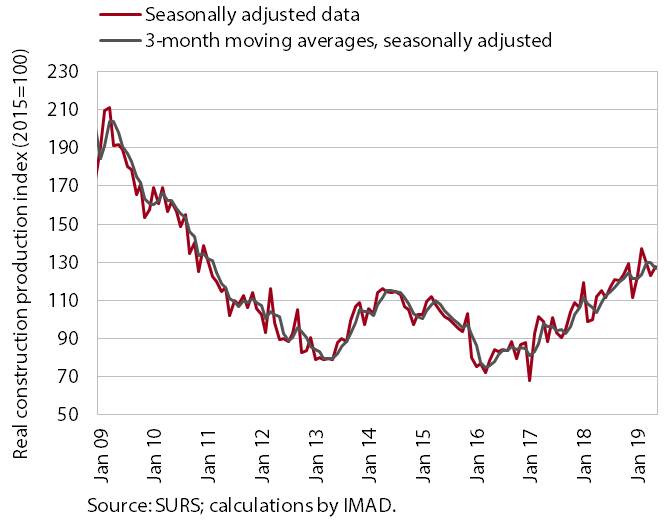

Construction, May 2019

Following the exceptionally strong activity at the beginning of the year, the value of construction output moderated in the spring but remained high. After the strong growth early in the year, which was partly due to favourable weather conditions, the value of construction output declined in March and April, before rising again in May to be 11.1% higher than in May 2018. The high level of activity is attributable to higher investments on the part of the government, municipalities and infrastructure companies, but it is also related to favourable results of the corporate sector and the lack of building in previous years.

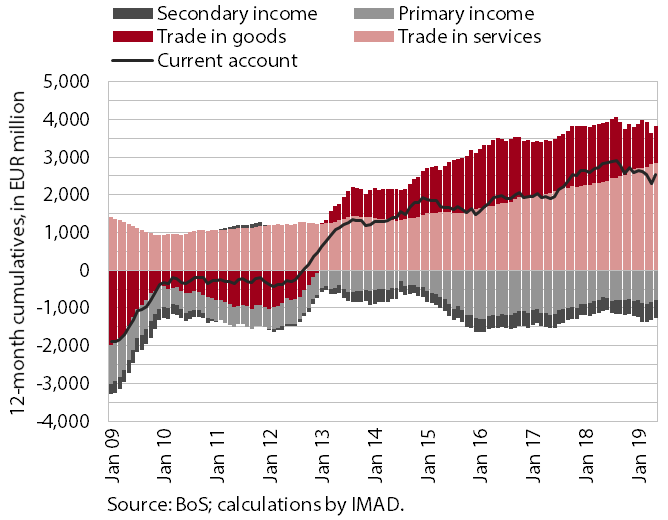

Current account of the balance of payments, May 2019

The surplus of the current account of the balance of payments was lower year on year in the twelve months to May (5.2% of estimated GDP). The lower surplus was mainly due to the lower surplus in trade in goods. The deficit in primary income was higher year on year primarily owing to the net outflows of dividends and profits abroad. The higher net outflows of secondary income were a consequence of higher payments into the EU budget. The surplus in service trade rose further, especially in trade in transport, travel and construction services.

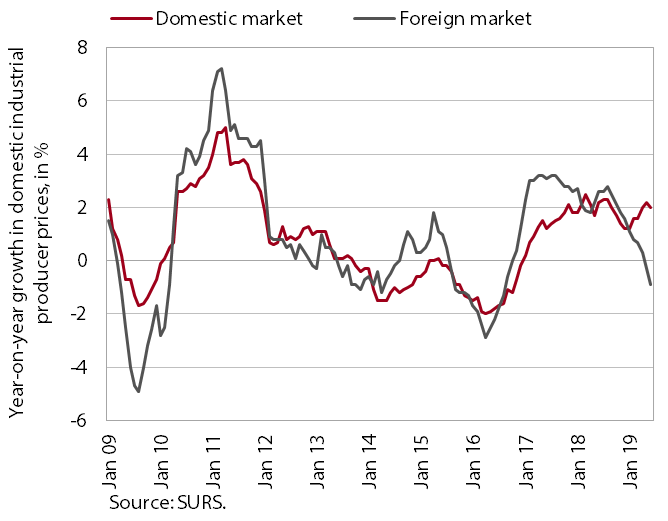

Slovenian industrial producer prices, June 2019

The total year-on-year growth of Slovenian industrial producer prices moderated further in the middle of the year. The moderation was mainly due to a further decline of prices on foreign markets. Producer prices declined across all product groups, which we estimate is related to slower growth in foreign demand. Price growth on the domestic market remained at around 2%, driven mainly by strong growth in energy prices (owing to higher electricity prices), but also year-on-year price rises in all other product groups.