Charts of the Week

Current economic trends from 13 to 17 May 2019: labour market, wages, construction, current account

In the first quarter, favourable labour market developments continued; employment increased and the growth of wages strengthened. The construction sector recorded further growth in both the construction of civil-engineering works and the construction of buildings; the indicators of future activity in construction are favourable as well.

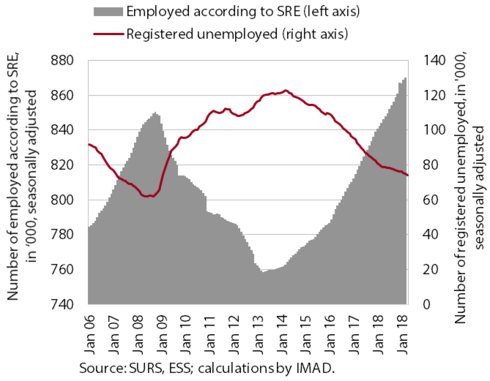

Labour market, March – April 2019

Labour market conditions continued to improve at the beginning of the year. In the first quarter, the number of employed persons increased further – the most in construction, transportation and manufacturing. Labour market conditions continued to be marked by labour shortages amid high demand for labour, which is also indicated by the high job vacancy rate and increased hiring of foreigners. In the first four months, the number of registered unemployed declined further, though more slowly than in previous years amid the already low level of unemployment. At the end of April, 73,965 persons were registered as unemployed, 5.8% fewer than in the same period of 2018.

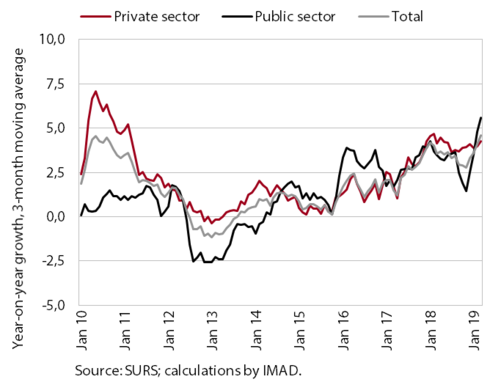

Wages, March 2019

Wage growth strengthened in the first three months of this year, in line with expectations. Wage growth in the private sector was – in addition to economic and demographic factors (good business results and gradual productivity growth, labour shortages and thus upward pressure on wages) – also due to the increase in the minimum wage. Wages rose the most in sectors that face the greatest labour shortages and have a high share of minimum wage recipients, i.e. trade, accommodation and food service activities and administrative and support service activities. Wage growth in the public sector, on the other hand, was mainly a consequence of strong wage growth in the government sector owing to the agreed wage rises at the end of last year; to some extent, it was also due to the increase in the minimum wage.

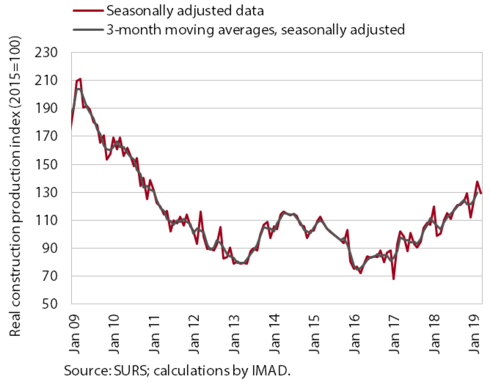

Construction, March 2019

In the first quarter, construction activity increased further, with considerable monthly fluctuations. After February’s strong growth, the value of construction output declined in March, but remained high. The first quarter recorded further growth in the construction of civil-engineering works, driven by higher investment by the government, municipalities and infrastructure companies. Further growth was also recorded in the construction of buildings. In residential construction, this was related to the strong demand for flats and the low construction of flats in previous years, while growth in non-residential construction was mainly due to good business results. The vigorous growth in activity, amid signs of labour shortages, is also reflected in pressures on prices: price growth in construction has not been so high since 2008. The values of the indicators of contracts, which suggest future activity in construction, also strengthened at the beginning of the year, the most in residential construction.

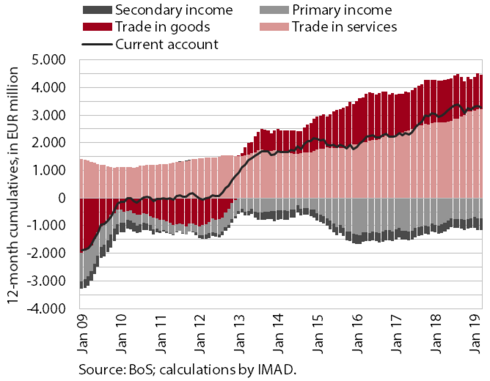

Current account, March 2019

In the first quarter, the current account surplus widened further year-on-year. The year-on-year increase arose mainly from a higher surplus in trade in goods and services. This was attributable primarily to volume factors (higher growth in exports than imports), while growth in import prices exceeded growth in export prices (deterioration in the terms of trade). The surplus also strengthened owing to a further narrowing of the deficit in primary income, particularly net interest receipts. This was a consequence of lower government debt servicing costs and a net inflow of interest into the private sector due to a considerable decline in external debt of commercial banks and increased financial investment in foreign securities. The higher net outflows of secondary income were marked particularly by higher VAT- and GNI-based payments into the EU budget in the first quarter of the year.