Charts of the Week

Current economic trends from 13 to 17 June 2022: labour market, construction, the balance of payments and other charts

The number of persons in employment continues to increase. Hiring of foreign workers contributed more than 50% to the year-on-year increase in April, with a particularly high share of foreign workers in construction. Construction activity declined slightly but remained higher than in the same months last year. Compared to previous years, the highest growth in activity was seen in the construction of buildings. Cost pressures in the construction sector continue. The current account surplus of the balance of payments is declining mainly due to the trends in trade in goods. Strengthening of domestic consumption and rising prices of energy and other commodities are having a negative impact on net trade in goods. The value of fiscally verified invoices at the end of May and in the first third of June was about one-fifth higher than in the same periods of 2021 and 2019, given soaring prices.

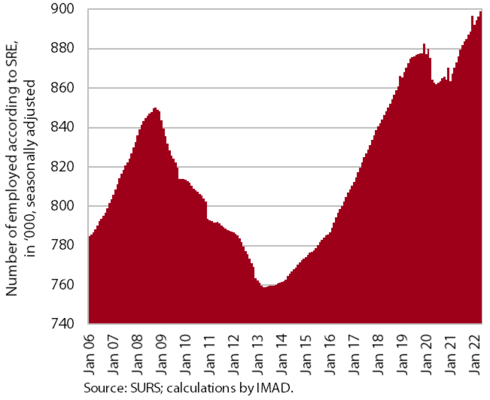

Labour market, April 2022

Year-on-year growth in the number of persons in employment in April was the same as in March (2.9%) and slightly lower than at the beginning of the year. It was still very high in accommodation and food service activities and in construction. As the economy recovered, growth in the number of persons in employment again depended largely on the employment of foreign workers, whose contribution to overall year-on-year growth was 58% in April. The share of foreigners among all persons in employment is also increasing, by 1.3 p.p. to 13.1% (in April 2022) compared to last year. This was largely due to the shortage of local labour, which (given the high vacancy rates) is greatest in construction, accommodation and food service activities and administrative and support service activities. The activities with the largest share of foreigners are construction (46%), transportation and storage (31%) and administrative and support service activities (25%).

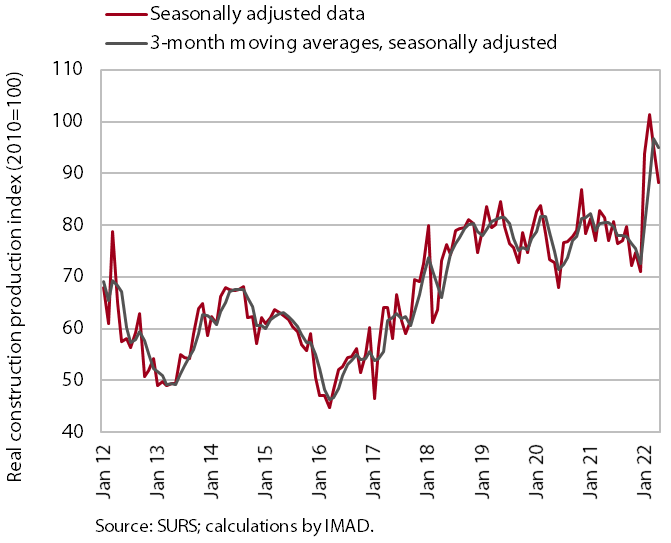

Construction, April 2022

According to figures on the value of construction put in place, construction activity decreased in April but remained higher year-on-year. After a strong pick-up in construction activity at the beginning of this year, the value of construction put in place declined on a monthly basis in March and April, but remained higher than in the same months of the previous year. Compared to previous years, construction of buildings stands out in terms of growth in activity. Activity also increased in civil engineering, while it was lower in specialised construction work (installation works, building completion, etc.).

Cost pressures continue to increase. The implicit deflator of the value of construction put in place (used to measure prices in the construction sector) was 22% in April, the highest level in the last 20 years. According to business trends in construction, high material costs were reported as a limiting factor by 69% of companies in May, while material shortage was reported by 40% of companies. Both indicators have risen sharply in the past year, reaching their highest level in the last 20 years.

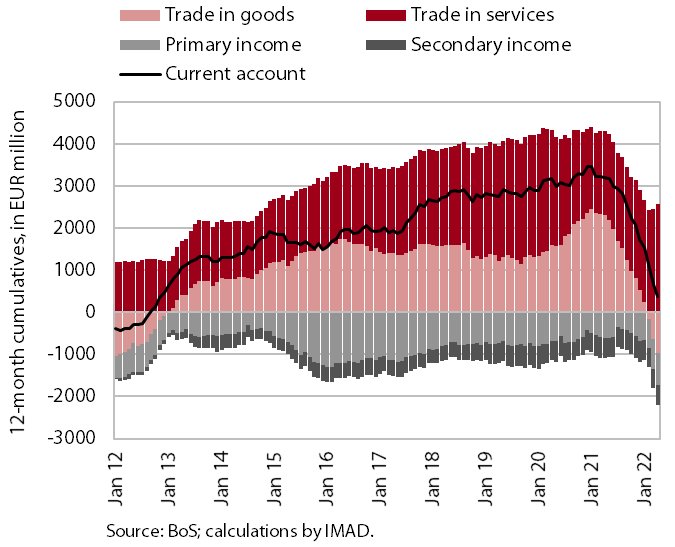

The balance of payments, April 2022

The surplus of the current account of the balance of payments fell again in April, mainly due to the trends in trade in goods. The 12-month current account surplus was lower than a year earlier, amounting to EUR 379.7 million (0.7% of estimated GDP). The year-on-year decline in the surplus in current transactions arose mainly from the goods trade balance, which turned from a surplus to a deficit at the end of last year. This is related mainly to faster real growth of imports, supported by the strengthening of domestic consumption, and rising prices for energy and other commodities, which have a negative effect on the balance of payments due to a relatively rigid demand. The primary income deficit was also higher, largely due to higher payments of dividends and profits to foreign investors and partly also to higher payments of traditional own resources to the EU budget. The surplus in trade in services has increased, especially in trade in travel (lifting of restrictions to contain the spread of COVID-19) and in trade in other business services (lifting of restrictions on business activity). The deficit in secondary income was lower, mainly due to year-on-year lower VAT- and GNI-based contributions to the EU budget.

Value of fiscally verified invoices, in nominal terms, 29 May–11 June 2022

The value of fiscally verified invoices between 29 May and 11 June was 18% higher year-on-year in nominal terms and 21% higher than in the same period of 2019, given the price surge. The nominal 12% growth of turnover in trade, where about three-quarters of the total value of fiscally verified invoices is issued, was the biggest contributor to year-on-year growth, which was similar to the previous two weeks. Another important contributor to growth was also the 78% nominal growth in accommodation and food service activities (mainly due to high growth in accommodation), which was significantly lower than in previous weeks due to the continued lifting of restrictions on business activity last June.

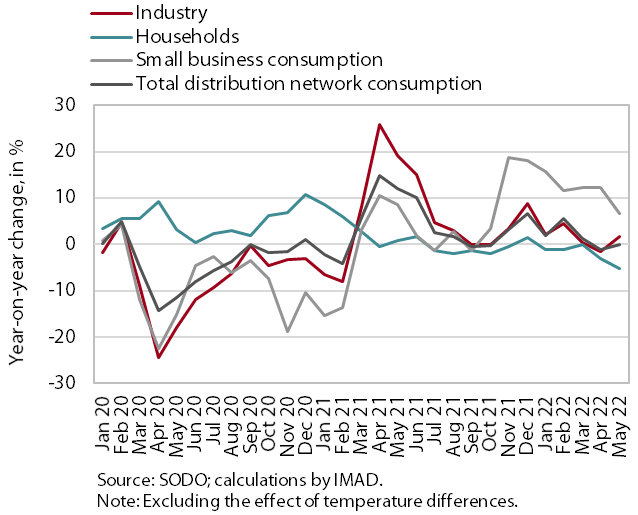

Electricity consumption by consumption group, May 2022

In May, industrial electricity consumption and small business electricity consumption were higher year-on-year, while they were slightly lower compared to the same period of 2019. Industrial electricity consumption was 1.8% higher year-on-year in May and small business electricity consumption was 6.7% higher, with the main reason for the increase in the latter being last year’s restrictions in trade and services. Household consumption was 5.2% lower in May than a year ago due to a better epidemiological situation and the fact that fewer people were working from home. Compared to May 2019, small business consumption was 1.9% lower and industrial consumption was 0.5% lower, which is mainly related to the unstable situation with regards to material supply and the energy crisis. Household consumption in May was similar to the same period in 2019.