Charts of the Week

Current economic trends from 13 to 17 January 2020: labour market, wages, construction, current account, road freight transport

Labour market conditions improved further towards the end of last year, albeit less than one year earlier. Wage growth was higher year on year, mainly owing to the increase in the government sector. The current account surplus widened further, especially on the back of higher surpluses in goods and services. After several months of decline, activity in construction started to increase again and the indicator of the stock of contracts was considerably higher year on year.

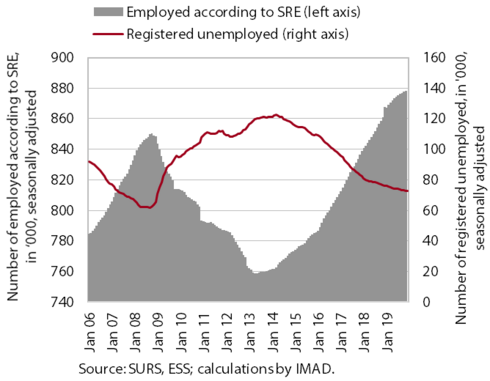

Labour market, November – December 2019

Labour market conditions improved further towards the end of last year, but the improvement was less intense than in the previous year. In the first eleven months, the number of persons employed increased 2.5% year on year (the most in construction, transportation and storage, and accommodation and food service activities), which is less than in the same period of 2018. Employment growth is still largely driven by the hiring of foreigners (their contribution to total employment growth exceeding 70%), which is a consequence of demographic change and the shortage of domestic labour. The number of unemployed persons continues to decline, albeit more slowly than at the beginning of 2019 amid increasingly limited labour supply. At the end of December, 75.292 persons were registered as unemployed, 4.1% fewer than in the same period of 2018.

Wages, November 2019

Last year, wage growth was higher than in 2018 mainly due to wage rises in the government sector. Year-on-year wage growth in the first eleven months as a whole was higher (4.3%) than in the same period of the previous year (3.4%). The higher growth was mainly a consequence of higher growth in the general government sector owing to the agreed wage rises and promotions. To some extent, it was also due to the increase in the minimum wage. With relatively low unemployment and good business performance, wage growth in the private sector remained similar to that one year earlier. Wages rose the most in administrative and support service activities and accommodation and food services activities.

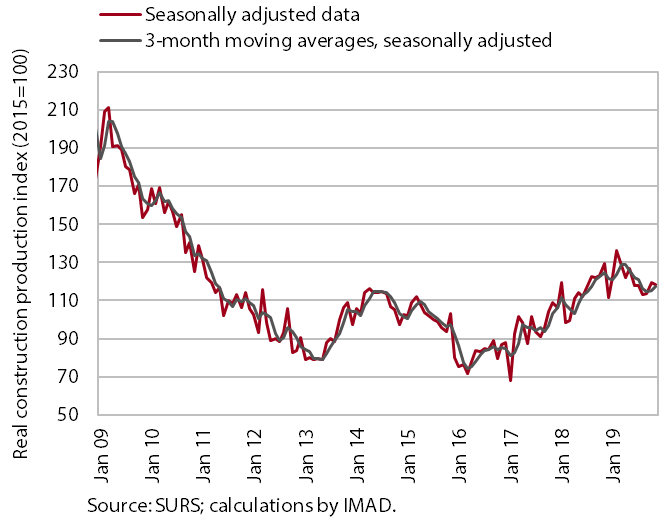

Construction, November 2019

The value of construction output increased towards the end of last year after several months of decline, but was lower than one year before. Following strong growth at the beginning of 2019, also owing to favourable weather conditions, the value of construction output fell in the middle of the year. The decline was the most pronounced in the construction of non-residential buildings, which was related to deteriorated expectations of the business sector and its investment activity. Towards the end of the year, activity strengthened across all construction sectors, the most in the construction of non-residential buildings. After increasing in the middle of the year, the stock of contracts was significantly higher year on year at the end of the year, while the value of new contracts was lower, with strong monthly fluctuations.

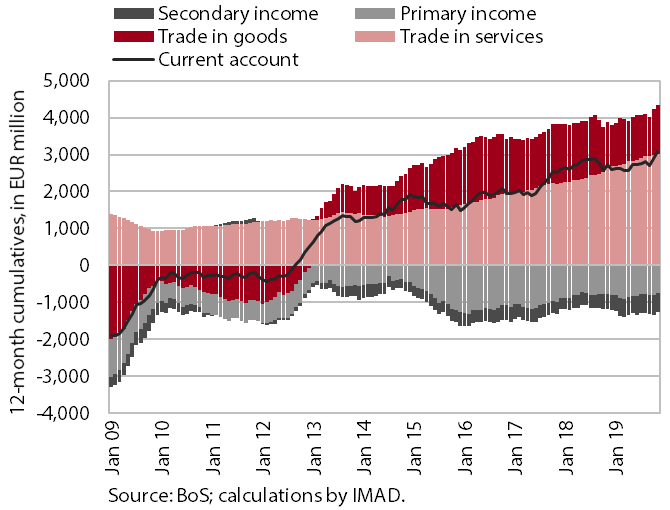

Current account, November 2019

In November, the current account surplus increased further and was higher year on year in the last twelve-month period (at 6.4% of estimated GDP). Amid faster real growth in exports than imports, this was mainly due to higher surpluses in goods and services. The net outflow of primary income declined further, mainly due to higher receipts from the EU budget for the implementation of the common agricultural and fisheries policy and lower net payments of interest on external debt. The deficit in secondary income was higher year on year, particularly due to higher payments into the EU budget (VAT-based and GNI-based contributions).

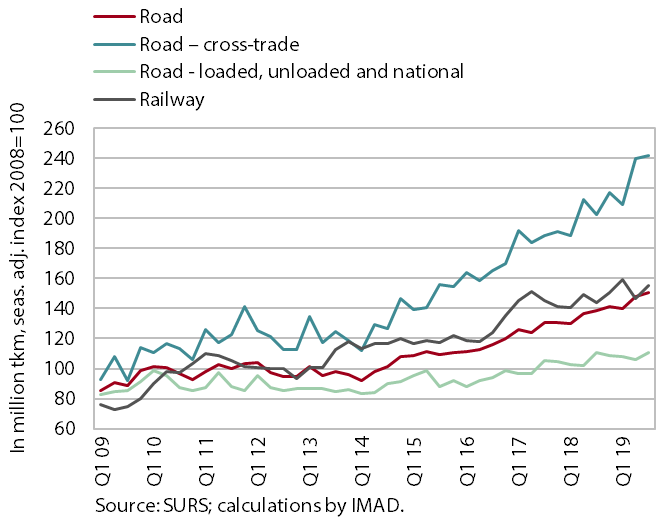

Road freight transport, Q3 2019

The volume of road and rail freight transport increased in the third quarter of 2019. Road transport taking place entirely abroad (cross-trade and cabotage) increased further and was one fifth higher year on year. The volume of road transport that is at least partially connected to the territory of Slovenia (exports, imports and national transport together) also increased, but maintained the level recorded in the same period of 2018. Growth in rail freight transport has slowed in the last two years compared to road transport, despite an increase in the third quarter.