Charts of the Week

Current economic trends from 12 to 16 October 2020: electricity consumption, traffic of electronically tolled vehicles, road and rail freight transport, labour market and other charts

The available indicators of activity for the beginning of October indicate that electricity consumption and freight traffic on motorways continue to lag behind last year’s levels, with traffic increasing slightly again, while the gap in electricity consumption has widened. Labour market conditions did not change significantly in the summer months, which we estimate is related to job-retention measures and the increase in activity after April’s sharp decline. In August, the number of employed persons remained similar to that in the previous two months, while the number of unemployed persons fell slightly further in September. The strengthening of activity in construction, which had started in July, continued in August, but activity remained considerably lower than before the epidemic.

Electricity consumption, October 2020

The deepening of the year-on-year decline in weekly electricity consumption, which had started in mid-September, continued at the beginning of October. Weekly electricity consumption was down 8% year on year in the first week of October (one week earlier, down 5%). Among Slovenia’s main trading partners, Austria had a similar year-on-year decline (-9 %), while the declines in Croatia and France were smaller (-2% and -4 % respectively). In other main trading partners, consumption exceeded last year’ level, in France by 5% and in Germany by 2%.

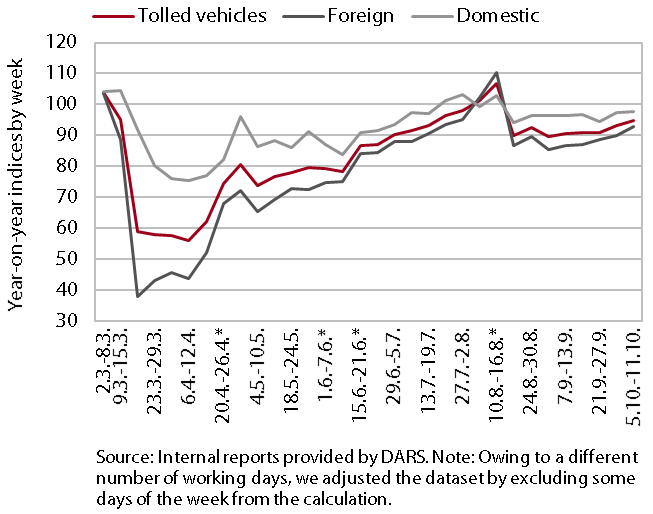

Traffic of electronically tolled vehicles on Slovenian motorways, October 2020

Freight traffic on Slovenian motorways increased further in the first half of October but remained somewhat lower than before the epidemic. After a sharp fall after the declaration of the epidemic, it was rising more markedly from mid-June to mid-August. Then it fell again and remained around 10% below the comparable last year’s level until the beginning of October, when it started to increase gradually again. In the second week of October, it was 5% below the comparable last year’s level, with the number of kilometres travelled by foreign hauliers falling more than that travelled by domestic hauliers (by 7% and 2% year on year respectively).

Road and rail freight transport, Q2 2020

In the second quarter of 2020, the volume of road freight transport decreased significantly due to the measures to contain the epidemic in the EU, while the volume of railway transport declined less than in the first quarter. Slovenian hauliers carry out almost nine tenths of their journeys abroad. The decline in road transport, which had started in the first quarter, continued in the second amid limited cross-border flows as a result of containment measures in individual countries. Road transport performed by Slovenian hauliers abroad declined more sharply, by 22% year on year. The volume of road transport that is at least partially connected to the territory of Slovenia (exports, imports and national transport together) decreased by 10%. The containment measures had a lesser impact on freight transport by rail, but this had already been falling for several quarters before the epidemic.

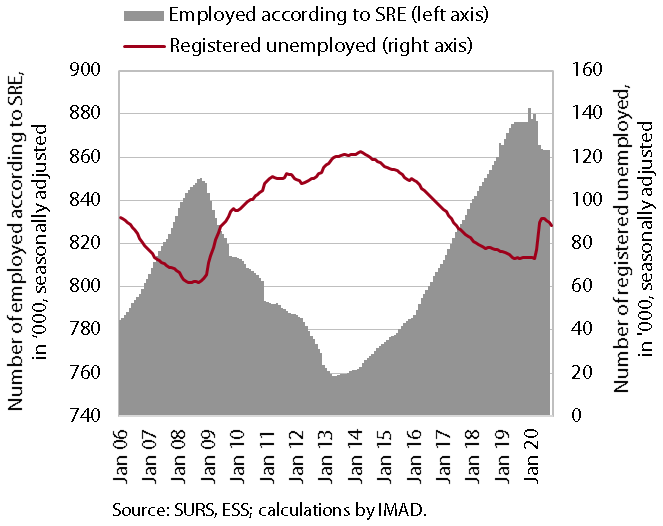

Labour market, August 2020

In August, employment remained at a similar level to that in the previous two months; unemployment fell in September. The number of employed persons was down 1.6% year on year in August, which is similar to the previous few months. Administrative and support service activities and accommodation and food service activities continue to stand out with the largest year-on-year declines (-11.4% and -6.2% respectively). An above-average fall was also recorded in manufacturing (-3.7%). A total of 83,766 persons were unemployed at the end of September, 5% fewer than at the end of August. The gradual decline in the number in the last two months was due not only to the recovery of economic activity, but also to measures to preserve jobs. Year on year, unemployment was up 20% at the end of September.

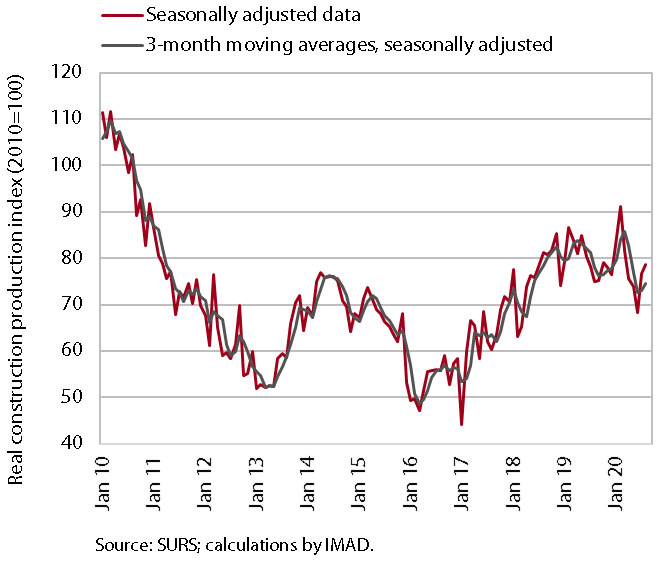

Construction, August 2020

After falling in the spring months, construction activity picked up in July and August. In August, activity was 13.9% lower compared with February, the last month before the outbreak of the epidemic. In comparison with 2018 and 2019, in the last few months, construction activity has been significantly lower in non-residential buildings, at more or less the same level in civil-engineering works and higher in non-residential buildings (where data for the last months are less reliable). Short-term prospects remain favourable for civil-engineering works, but the prospects for the construction of buildings, especially non-residential buildings, are not so good. In the last year, the stock of contracts in the construction of civil-engineering works has increased by more than 50%, while in the construction of non-residential buildings it remained almost unchanged. In the last months, the total floor area of buildings planned by issued building permits was still lower than in the same period of last year. The total floor area of residential buildings was 12% and that of residential buildings 6% lower year on year.

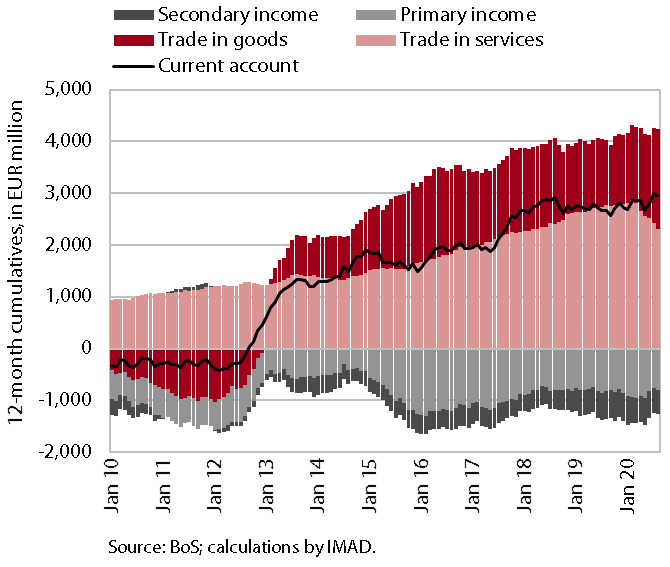

Current account, August 2020

In the current account, the measures to contain the epidemic were mainly reflected in the segment of goods and services trade and in primary income. In August, the current account surplus declined but remained high, amounting to EUR 3 billion in the last 12 months (6.5% of estimated GDP). Despite a further widening of the surplus in trade in goods, the year-on-year decline in the surplus in current transactions mainly arose from a lower surplus in services due to a decline in trade in services (exports fell more than imports) as a consequence of the coronavirus crisis, particularly in the segment of travel and transport services. It should be noted that the increase in trade in goods was a consequence of a larger real fall in goods imports than exports and the improved terms of trade. The deficit in primary income was up year on year, mostly due to higher net inflows of income from equity capital of direct investment. The lower deficit in secondary income was again marked by lower VAT- and GNI-based contributions to the EU budget.