Charts of the Week

Current Economic Trends from 11 to 15 March 2019: Exports and imports of goods, Manufacturing, Construction, Earnings

The movement of the export-oriented part of the economy at the beginning of the year remains under the impact of accelerated growth in production of pharmaceutical and medical goods and modest activity in the European car industry, which is reflected in low production of motor vehicles and some intermediate goods. Activity in construction is strengthening further.

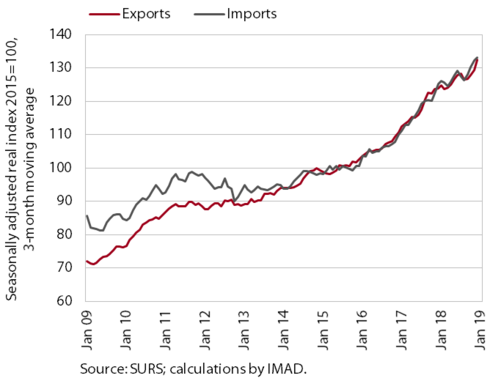

Exports and imports of goods, January 2019

Following the moderation in the second half of last year, exports recorded fairly strong growth in January; the strong growth of imports also continued. Last year’s moderation, amid the slowdown of economic activity in Slovenia’s main trading partners, was affected by lower growth in most key manufactured goods and significantly lower vehicle exports (owing to the petering out of a one-off factor). Meanwhile, exports of medical and pharmaceutical products and some primary products strengthened significantly, including at the beginning of the year according to our estimate. Growth in imports was affected particularly by further growth in imports of consumer goods, as growth in intermediate and investment goods imports slowed notably towards the end of the year.

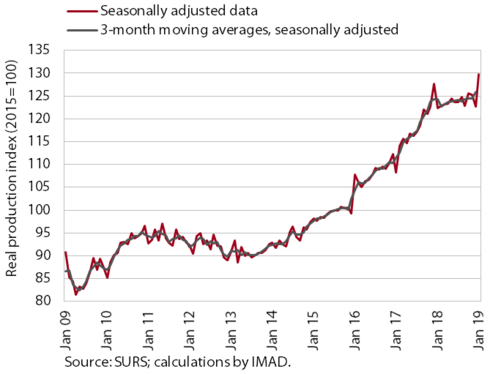

Manufacturing, January 2019

After the modest strengthening in the second half of 2018, manufacturing output increased notably at the beginning of this year, the most in high-technology industries, where it was more than one-fifth higher year on year (according to our estimate, mostly as a result of the pharmaceutical industry). The movement of the production of motor vehicles and most intermediates, particularly for the European car industry, reflects the petering out of the one-off effect of the start of the production of a new passenger car in 2017, which was still strongly felt in the first months of last year, and the new global standard for measuring fuel consumption and emissions introduced in September 2018. In these industries, January’s production was lower than or similar to that one year before.

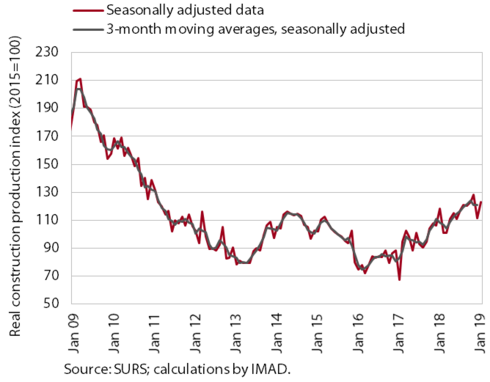

Construction, January 2019

The value of construction output rose again in January after December’s decline. Activity increased in all three segments (civil engineering works, residential and non-residential buildings), over a longer period (one year) the most in the construction of civil-engineering works.

The indicators of contracts, which suggest future activity in construction dropped both in January and towards the end of last year. The stock of contracts in construction was thus down year on year in January.

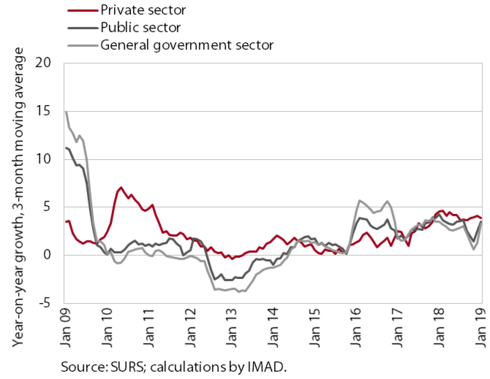

Earnings, January 2019

In January, wage growth was notably higher year on year. Wage growth in the private sector was, in addition to favourable economic factors such as low unemployment (and the related impacts of labour shortages) and good business results also due to the increase in the minimum wage. Wages rose the most in those sectors that have the largest labour shortages and employ a large number of workers with below-average wage (in trade, transportation, accommodation and food service activities, manufacturing and administrative and support service activities). In the public sector, wage growth was affected by strong wage growth in the government sector as a result of the wage rises agreed at the end of last year and, to a lesser extent, a higher minimum wage.