Charts of the Week

Current economic trends from 11 to 15 April 2022: electricity consumption by consumption group, manufacturing, construction, current account and other charts

In March, industrial electricity consumption was still behind that of the same period before the epidemic, which is related to supply chain disruptions and, consequently, shortages of raw materials that have significantly hampered business operations. Small business consumption was higher, as was household consumption due to the still high number of active COVID-19 infections and more people working from home. In February, manufacturing output fell for the second month in a row. It declined in high- and medium-high technology industries amid ongoing supply chain disruptions. Following a decline last year, construction activity continued to pick up in February, and after a prolonged period, non-residential construction activity also increased; cost pressures in the construction sector are increasing. The current account surplus narrowed in recent months, which is related to rising prices for energy and other primary commodities, and consequently faster growth of import than export prices.

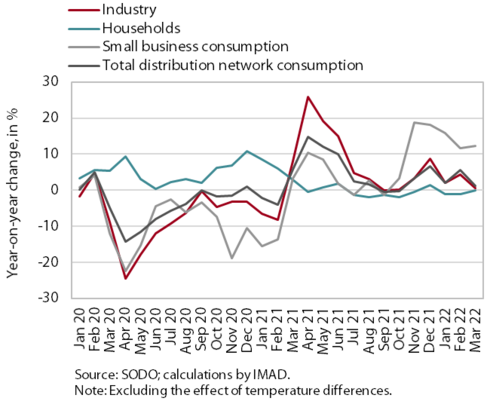

Electricity consumption by consumption group, March 2022

In March, industrial electricity consumption was still behind that of the same period before the epidemic, while small business consumption was higher. Industrial electricity consumption remained almost unchanged year-on-year, as did household consumption. Small business electricity consumption was 12.3% higher year-on-year in March, mainly due to last year’s low base. Compared to March 2019, small business consumption was 2.8% higher as a result of the easing of containment measures in February as well as two more working days. Nevertheless, industrial consumption was about 1% lower than in March 2019, most likely due to supply problems and a shortage of raw materials. Household consumption was 8.5% higher in March than in the same period of 2019, due to the ongoing COVID-19 infections and the fact that some workers were still working from home.

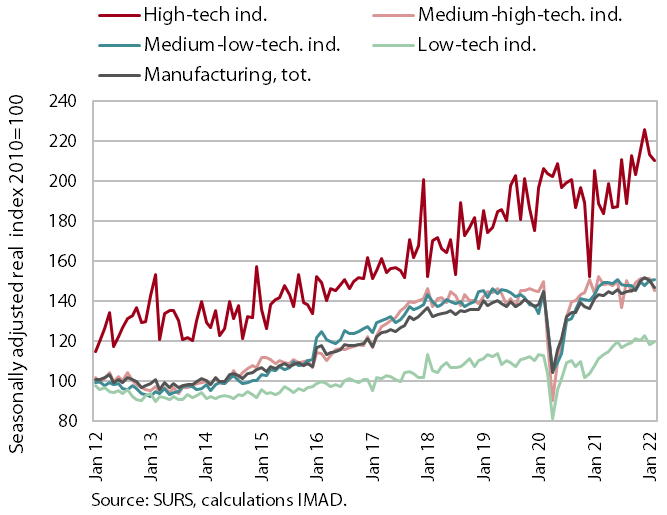

Manufacturing, February 2022

Manufacturing output fell for the second month in a row in February. Given the ongoing supply chain disruptions, the volume of production compared to January declined in high- and medium-high technology industries, while it increased slightly in medium-low and low-technology industries. Year-on-year, manufacturing growth was 2.4%, the lowest since October last year, with production volume rising the most in high-technology industries and falling in medium-high technology industries. The decline was mainly due to the automotive industry, which recorded the sharpest year-on-year decline since September last year (22.1%), while the manufacture of electrical equipment and the manufacture of machinery and equipment n.e.c. were also negative.

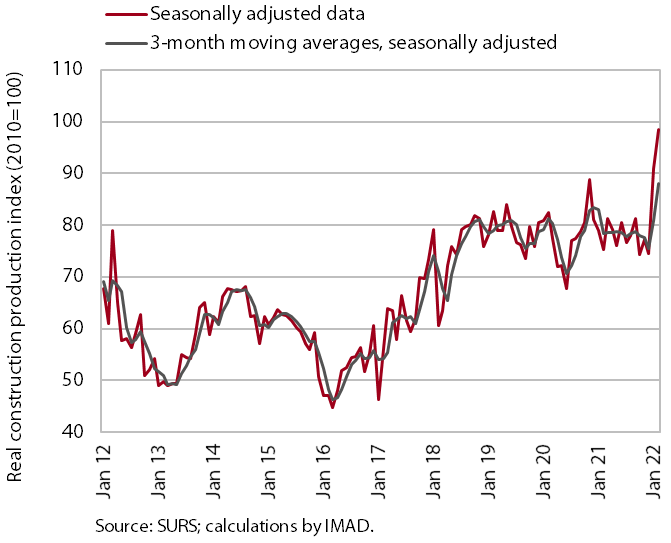

Construction, February 2022

According to figures on the value of construction work completed, construction activity increased in February. After a gradual decline in construction activity last year, the value of completed works increased at the beginning of 2022 and was 32.3% higher in February than in February 2021 given the favourable weather conditions. The beginning of the year saw an increase in non-residential construction activity after a long period of time; this is also the construction segment to have contracted most markedly last year. Activity rose also in the construction of residential buildings and civil-engineering works, while it remained at the level seen at the end of 2021 in specialised construction.

Cost pressures are increasing. The implicit deflator of the value of completed construction works (used to measure prices in the construction sector) was above 15% in February, the highest level in the last 20 years. According to business trends in construction, high material costs were cited as a limiting factor by two-thirds of companies in March, while material shortages were cited by 30% of companies, which in both cases is also the highest level in 20 years.

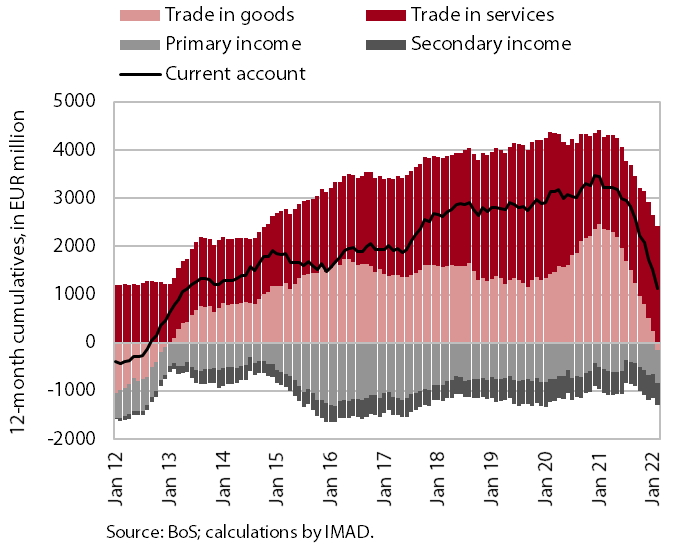

Current account, February 2022

The surplus of the current account of the balance of payments has declined. The 12-month current account surplus was down year-on-year, amounting to EUR 1.1 billion (2.0% of estimated GDP). The year-on-year decline in the surplus in current transactions arose mainly from the trade balance, which turned from a surplus to a deficit. This is related to rising prices for energy and other primary commodities, since import prices have been rising much faster than export prices in recent months. The primary income deficit was also higher, largely due to higher dividend payments and profits by foreign investors. The surplus in trade in services continued to increase, especially in trade in travel and other business services. The deficit in secondary income was lower, mainly due to year-on-year lower VAT- and GNI-based contributions to the EU budget.

Road and rail freight transport, Q4 2021

In the last quarter of 2021, the volume of road freight transport fell slightly for the second consecutive quarter, while the volume of rail transport increased slightly. The volume of road transport performed by Slovenian road freight operators decreased quarter-on-quarter mainly due to a decrease in cross trade transport, while the volume of road transport performed at least partially on Slovenian territory (exports, imports and national transport combined) increased. Compared to the same quarter of 2019, the volume of road transport was 1% higher (transport performed abroad was one-tenth lower, and the other mentioned transport was more than one-tenth higher). Rail freight transport, which was already down before the epidemic, was 3% lower than in the same quarter of 2019. In 2021, the volume of road transport was 4% higher than in 2019, while the volume of rail transport was almost 7% lower.