Charts of the Week

Current economic trends from 10 to 14 May 2021: traffic of electronically tolled vehicles, electricity consumption, electricity consumption by consumption group, registered unemployment and other charts

The first quarter of this year saw a continuation of relatively favourable movements of the export-oriented part of the economy, which reached pre-crisis levels at the end of last year. Goods exports to EU countries increased further quarter on quarter, as did manufacturing production. After strengthening in the second half of last year, activity in construction fell in the first quarter, particularly in non-residential buildings. Current data on economic activity indicate considerably higher levels of freight traffic on Slovenian motorways and electricity consumption year on year at the beginning of May, which can be mainly attributed to last year’s low activity due to more stringent measures to contain the spread of the epidemic. The values of these two indicators are close to pre-epidemic levels or slightly lower. In the first half of May, the number of registered unemployed persons fell further but remained higher than before the epidemic.

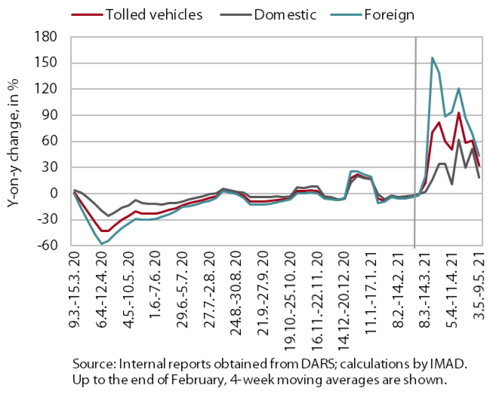

Traffic of electronically tolled vehicles on Slovenian motorways, May 2021

Freight traffic on Slovenian motorways in the first week of May was 32% higher than in the same period of last year but 3 % lower than in the same period of 2019. Between 3 and 9 May, domestic vehicle traffic was 18% higher and foreign vehicle traffic 44% higher year on year. This strong year-on-year growth was still mainly due to lower traffic in the same period last year as a consequence of containment measures during the first wave of the epidemic, although their negative impact on industry and freight transport was already decreasing. The volume of freight traffic in the first week of May was somewhat higher than this year’s 18-week average but somewhat lower compared with the same week of the pre-crisis year 2019 (in domestic vehicles 2% higher and in foreign vehicles 6% lower).

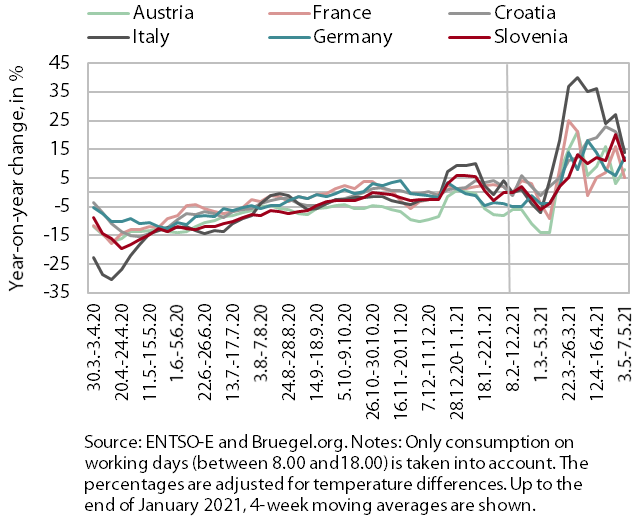

Electricity consumption, May 2021

Electricity consumption in the first week of May was 11% higher compared with the same week of 2020 but 3% lower compared with the same week of the pre-crisis year 2019. The year-on-year higher consumption between 3 and 7 May is attributable to the low base effect; despite the relaxation of a number of containment measures, it has not yet achieved the level seen before the epidemic. As a result of the base effect, higher consumption year on year was also recorded in our main trading partners, from 5% in France to 15% in Croatia. Relative to the same week of 2019, consumption was down in most trading partners (in Italy, France and Croatia by around 4% and in Austria and Germany by 2%).

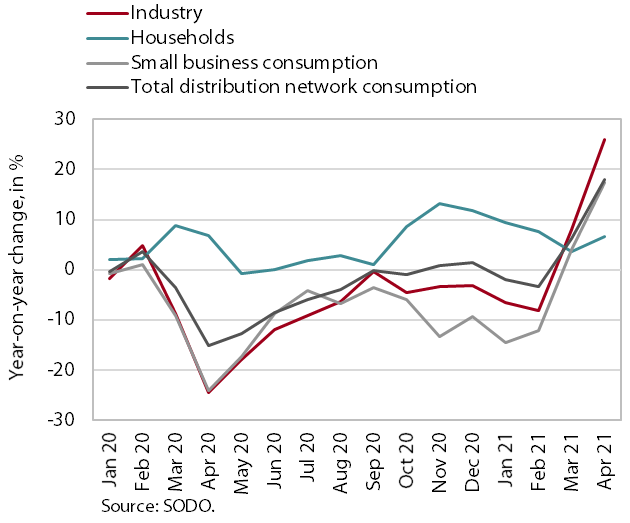

Electricity consumption by consumption group, April 2021

In April, electricity consumption by all consumption groups was higher year on year, while compared with the same period of the pre-crisis year 2019, the lags in industrial and small business consumption were larger than a month earlier. In April, industrial electricity consumption was 25.9% and small business electricity consumption 17.3% higher year on year. The main reason was the base effect, as in April last year electricity consumption dropped notably as a result of stringent containment measures. Household consumption was also higher year on year, by 6.6%. Relative to April 2019, however, industrial consumption was down 4.9% (in March 1.4%) while small business consumption was down 10.9% (in March 5.3%), largely due to the temporary tightening of measures at the beginning of this April. Household electricity consumption was 13.8% higher than in April 2019, as people spent more time at home due to the epidemic.

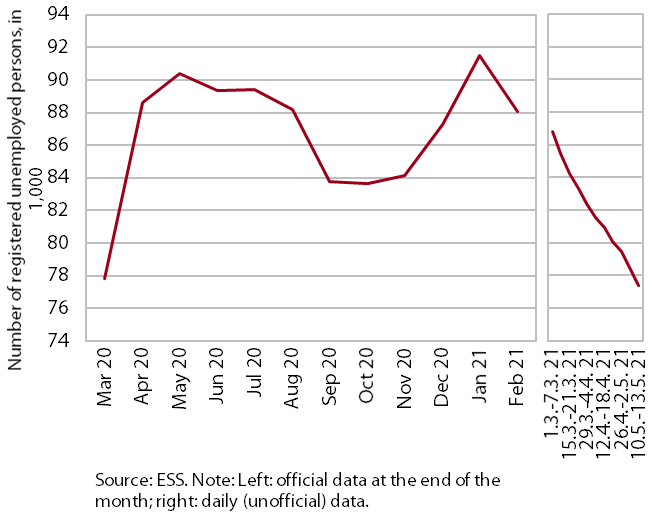

Registered unemployment, May 2021

The number of registered unemployed persons fell further at the beginning of May. Following the increases in December and January, which amid the retention of intervention measures did not differ much from seasonal increases in the same period of previous years, the number of unemployed continued to fall from February to April. Similar developments were also seen in the first half of May. The decline is, in addition to seasonal factors, also related to the gradual easing of containment measures. On 13 May, 77,048 persons were unemployed according to ESS unofficial (daily) data, which is 2.8% less than at the end of April and around 15% less than in the same period last year. Compared with May 2019, the number was, however, around 7% higher.

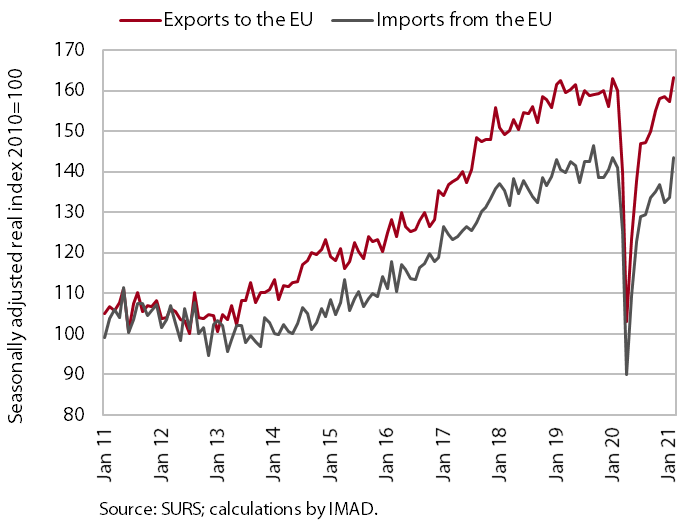

Goods trade, March 2021

Goods trade continued to recover in the first quarter of this year. Real goods exports to EU countries rose further in March and exceeded pre-crisis levels in the first quarter. We estimate that exports rebounded in most main sectors. Meanwhile, the recovery of vehicle exports came to a halt. Particularly the movements of exports of intermediate goods remained favourable. Export expectations, which have been improving in recent months, did not change significantly in April, but companies were more optimistic regarding future foreign demand than before the beginning of the epidemic. Goods imports also recovered further, which is attributable particularly to the recovery of industrial activities and consequently higher imports of intermediate goods.

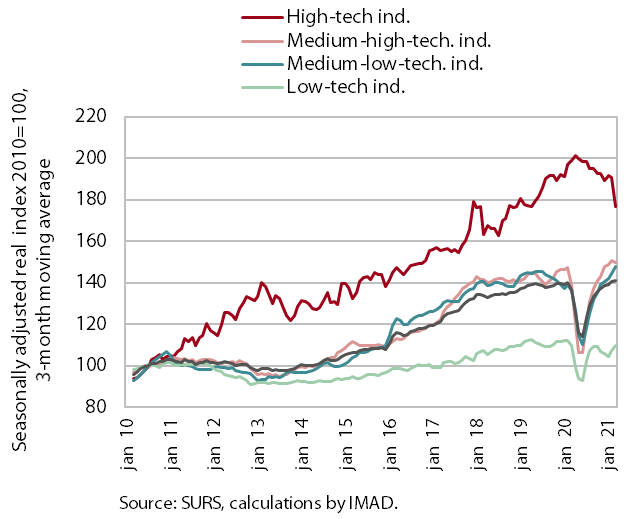

Production volume in manufacturing, March 2021

Production volume in manufacturing increased further in the first quarter of this year, despite somewhat weaker activity in March. After strengthening at the beginning of the year, in March activity declined, reflecting a fall in high-technology industries. Production in medium-high industries also decreased slightly. In high-technology industries, activity also contracted in quarterly terms, while activity in medium-high, medium-low and low-technology industries increased. In the first quarter, activity of high-technology industries was also lower year on year, according to our estimate mainly due to the worse performance of the pharmaceutical industry and last year’s high base. A minor year-on-year fall was also seen in low-technology industries, where it was more broadly based. Activity in medium-high and medium-low technology industries was up year on year in the first quarter, worse results being recorded only for the automotive industry and the manufacture of non-metallic mineral products.

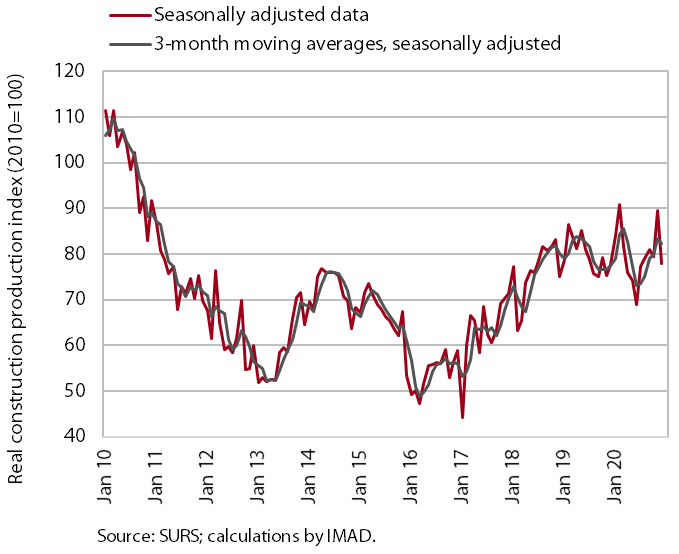

Construction, March 2021

Construction activity fell somewhat in the first quarter. The value of construction output declined by 2.2% and was 4.0% lower than a year before. The decline reflected lower activity in non-residential buildings, while in all other construction segments (civil engineering, residential buildings and specialised construction activities) activity strengthened both at the current level and year on year. Data on the number of contracts suggest a continuation of relatively low activity in the construction of non-residential buildings, while other segments, particularly the construction of civil-engineering works and specialised construction activities, are expected to fare better.

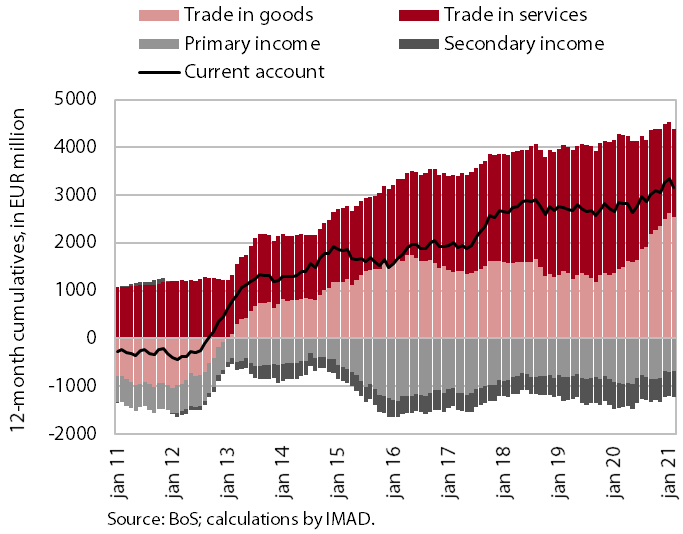

Current account, March 2021

In the first quarter, the current account surplus remained higher year on year, its growth being mainly driven by the surplus in trade in goods. The increase in the surplus in trade in goods was a consequence of higher real growth in exports than imports amid deteriorated terms of trade. The surplus in trade in services narrowed further. The measures to contain the epidemic significantly affected particularly trade in travel services, which was 80% lower year on year. Quarter on quarter, the surplus in trade in travel services was the lowest thus far, at EUR 35 million. Net outflows of primary income dropped further, mostly owing to lower net payments of income on equity and interest on external debt. The surplus also strengthened due to lower net outflows of secondary income, which fell mainly as a consequence of higher revenue (social receipts) from the EU budget.