Charts of the Week

Current economic trends from 10 to 14 June 2019: manufacturing production, construction, current account

Activity in construction, which deteriorated for the second consecutive month in April due to worse weather conditions, remains high. After the strong growth early in the year, manufacturing output increased further, yet at a more moderate pace. The dynamics of goods exports followed the same pattern, which – amid strong growth in goods imports – contributed to the lower surplus of the current account.

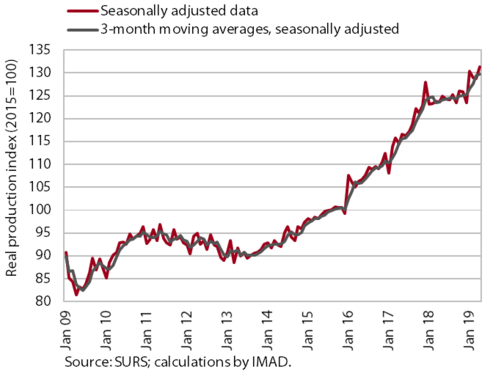

Manufacturing production, April 2019

In April manufacturing production increased further, after the surge at the beginning of the year. Its growth was mainly driven by high-technology industries, particularly the pharmaceutical industry according to our estimate. Production also strengthened in most other industries. In the first four months it was up 6.4% year on year, on average, in addition to the pharmaceutical industry, the most in some industries of lower technological intensity (in the wood processing and leather industries, the manufacture of other non-metallic mineral products and the repair and installation of machinery and equipment). The production of motor vehicles was down year on year, while the production of some intermediate goods (particularly in the metal and rubber industries) remained roughly the same, to a great extent due to the slowdown in the EU car industry.

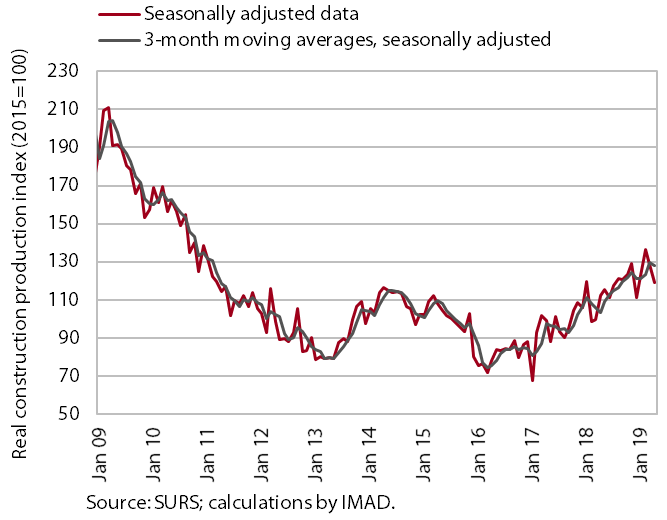

Construction, April 2019

The value of construction output declined in April but remained high. After the strong growth at the beginning of the year, also on account of favourable weather conditions, it otherwise declined in March and April but remained high. The high level of activity is attributable to higher investments of the government, municipalities and infrastructure companies, but also to favourable results of the corporate sector and the lack of building in previous years. The value of the indicators of contracts, which suggest future activity in construction, increased this year. The values of the stock of contracts and new contracts, having declined towards the end of last year, strengthened again this year, the most in residential buildings.

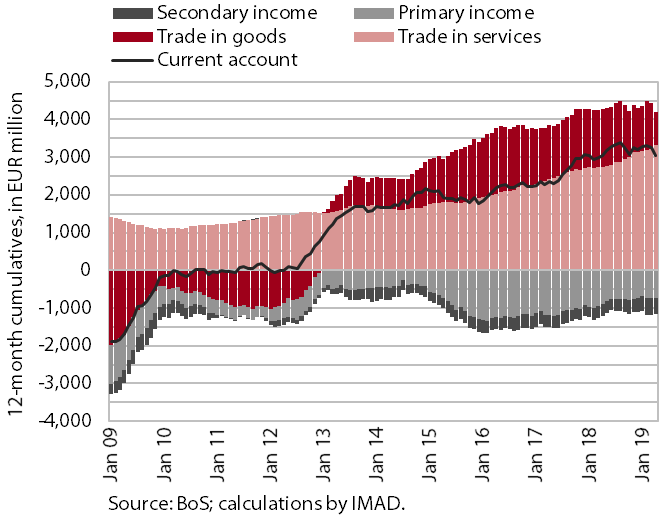

Current account, April 2019

The surplus of the current account of the balance of payments declined again in April; in the last 12 months, it was lower year on year (at 6.2 % of estimated GDP). The lower surplus in comparison with the previous 12-month period was mainly due to the lower surplus in trade in goods. The contribution of the terms of trade also remained negative, given the higher growth of import than export prices amid a rise in energy prices. The lower current account surplus year on year was also due to the higher net outflow of secondary income, mainly owing to higher VAT- and GNI-based payments into the EU budget. The surplus of services was higher, mainly as a result of the higher surplus in trade in transport and construction services and higher net revenues from travel. Net outflows of primary income remained lower due to lower net interest payments on external debt.