Charts of the Week

Charts of the week from 6 to 10 March 2023: trade in goods, production volume in manufacturing, value of fiscally verified invoices and other charts

Exports to EU Member States continued to decline at the beginning of the year, while imports remained roughly unchanged from the previous months, with consumer goods imports increasing and intermediate goods imports decreasing. Manufacturing output increased slightly in January and was at a similar level than in January last year. Year-on-year growth in freight traffic on Slovenian motorways slowed and stood at only slightly more than one percent in February. Year-on-year growth in the value of fiscally verified invoices slowed significantly due to the high base last year when some of the restrictive measures related to the epidemic were lifted. In February, the number of unemployed continued to fall and was 17.6% lower compared to the same month of 2022. The number of long-term unemployed also fell by almost one third, indicating a significant labour shortage.

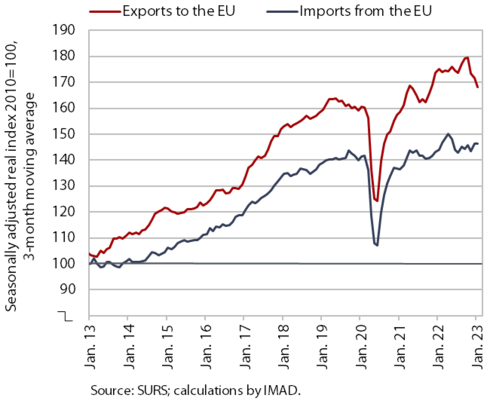

Trade in goods – in real terms, January 2023

Exports to EU Member States continued to fall at the beginning of the year, while imports remained largely unchanged from the previous months. In January, trade in goods with EU Member States further declined month-on-month (seasonally adjusted) amid uncertainty about the recovery in Slovenia’s main trading partners. The decline in exports in recent months was mainly due to lower exports of intermediate products, especially metals and metal products, and trade in petroleum products was also significantly lower than in the second and third quarters of last year. On the import side, imports of consumer goods increased slightly, while imports of intermediate goods declined, similarly to exports, reflecting a slowdown in manufacturing activity. Exports to EU Member States were noticeably lower in January compared to the same period last year, while imports from these countries increased slightly. Sentiment in export-oriented activities remained low in February and export expectations were also low.

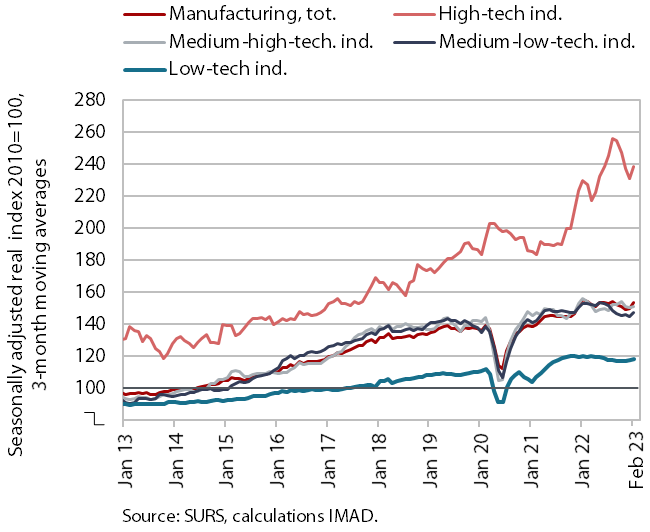

Production volume in manufacturing, January 2023

Manufacturing output rose slightly in January and was similar than a year ago. The increase was largely driven by high technology industries, where output remained higher year-on-year. The energy crisis, and thus the slowdown in demand growth, continues to have the greatest negative impact on energy-intensive industries, where output was lower than a year ago. The largest decline (by more than a fifth) was recorded in the paper industry and the smallest (by just over 3%) in the rubber industry and the manufacture of other non-metallic mineral products (a decline of about 15% in the chemical industry and the manufacture of basic metals). The manufacture of motor vehicles also remained a tenth lower than a year ago, reflecting slower demand growth and, to a lesser extent, supply chain disruptions. Manufacturing companies’ expectations for future output growth remain subdued, influenced to a large extent by the prospects for exports, which remain low.

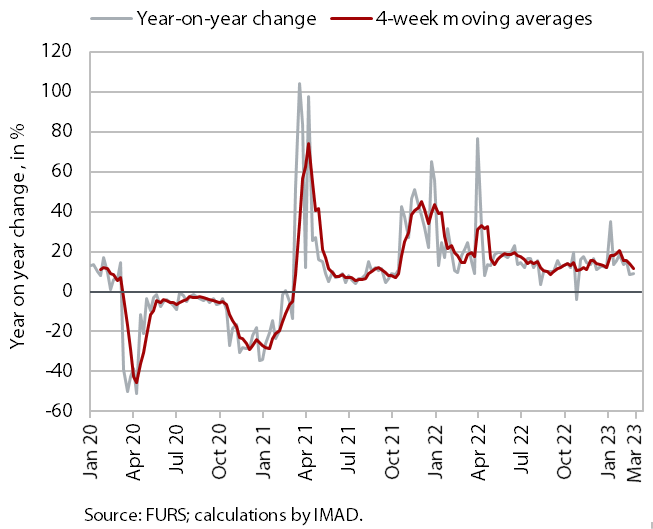

Value of fiscally verified invoices, in nominal terms, 19 February–4 March 2023

Amid high price growth, the nominal value of fiscally verified invoices between 19 February and 4 March 2023 was 9% higher year-on-year. Year-on-year turnover growth slowed significantly due to the high base last year, when some of the restrictive measures related to the epidemic were lifted. Compared to growth at the beginning of the year, nominal turnover growth more than halved in accommodation and food services (13%), certain creative, arts, entertainment, and sports services and betting and gambling (total growth in other service activities was 11%). Growth slowed slightly (from 11% to 9%) in trade, which accounted for almost 80% of the total value of fiscally verified invoices issued.

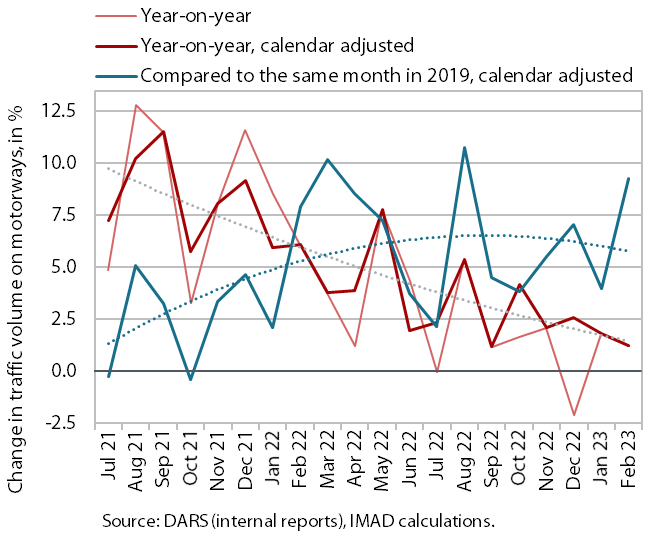

Traffic of electronically tolled vehicles on Slovenian motorways, February 2023

Year-on-year growth in freight traffic on Slovenian motorways has slowed and stood at slightly more than one percent in February 2023. In mid-2021, freight traffic still grew by more than 10% year-on-year, but by February 2023 growth fell to just 1.2%. However, traffic volumes were already significantly higher in this period compared to the same months in 2019, with an average increase of around 6% last year and this year. The share of foreign traffic was noticeably lower only at the beginning of the epidemic and fluctuated slightly from month to month, but otherwise remained very constant and was around 61% in February, suggesting that neither the epidemic nor the energy crisis had a significant impact on the structure of traffic.

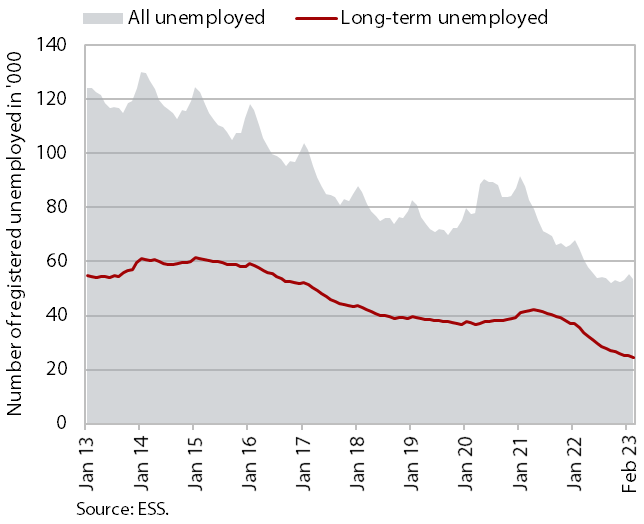

Number of registered unemployed, February 2023

In February, the number of registered unemployed fell further (by 1.4%) according to seasonally-adjusted data. According to original data, 53,404 people were unemployed at the end of February, 3.6% less than at the end of January. Unemployment was down 17.6% year-on-year. According to original data, the number of long-term unemployed also declined (by almost one third year-on-year in February), reflecting a serious labour shortage.