Charts of the Week

Charts of the week from 21 to 25 November 2022: economic sentiment, slovenian industrial producer prices and average gross wage per employee

Economic sentiment stopped deteriorating in November and confidence indicators rose in all segments. At the same time, the value of the economic sentiment indicator remains significantly lower than a year ago, mainly due to lower confidence in manufacturing and among consumers. After almost two years of continuous growth, Slovenian industrial producer prices fell in October, although year-on-year growth was still relatively high. In the face of high inflation, the average gross wage fell again in real terms year-on-year in July. The decline was more pronounced in the public sector due to last year’s high base related to the payment of COVID-19 bonuses.

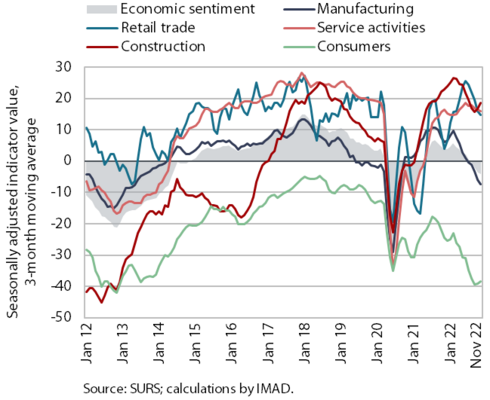

Economic sentiment, November 2022

Economic sentiment stopped deteriorating in November. Confidence increased month-on-month in most activities and was also higher among consumers. We believe that this is partly related to the decline in uncertainty about the supply of energy products this winter. Year-on-year, confidence is higher in retail trade, services and construction, while confidence is still significantly lower in manufacturing and among consumers. In manufacturing, this is related to the current situation in the international environment (high prices of intermediate goods and energy, uncertainty about economic growth in Slovenia’s main trading partners), while lower confidence among consumers is related to the decline in purchasing power due to high prices.

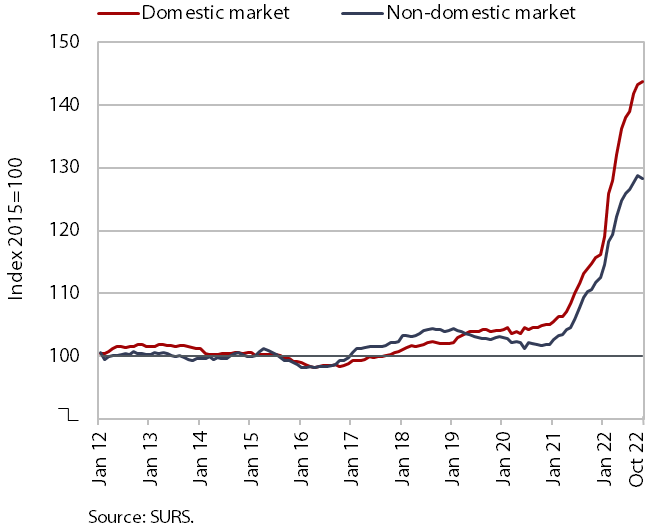

Slovenian industrial producer prices, October 2022

After almost two years of continuous growth, Slovenian industrial producer prices remained unchanged month-on-month in October, while year-on-year growth remains high (20.6%), although it fell slightly in the last month. Amid the slowdown in economic activity, this was mainly due to the gradual slowdown in the year-on-year increase in the prices of intermediate goods (20.9%) and capital goods (10.0%). Growth in the prices of energy (96.4%) and consumer goods (13.5%) was slightly more pronounced. On domestic markets, the year-on-year price increase since May this year has been around 25%. On the foreign markets, the price increase has weakened more notably in this period and was 16% year-on-year in October.

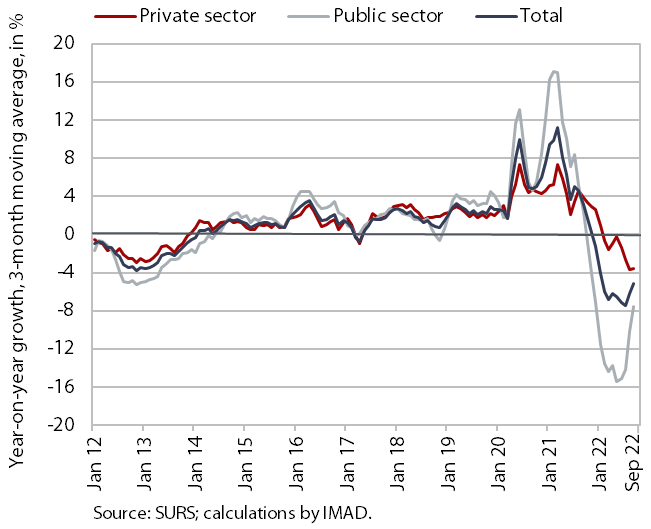

Average gross wage per employee, September 2022

Amid high inflation, the average gross wage fell by 3.5% year-on-year in real terms in September, more in the public sector than in the private sector. In the private sector, the real year-on-year decline (2.9%) was somewhat smaller than in the previous months. It was lowest in transportation and storage and in administrative and support service activities, which are facing major labour shortages. In the public sector, however, the year-on-year decline in real terms (4.5%) was smaller than in previous months, which is related to the year-on-year effect of the cessation of payment of most COVID-19 bonuses in July last year. The decline was smallest in health and social work activities, where wages were raised in December 2021 to address labour shortages. Compared to September last year, gross wages increased by 6.1% in nominal terms – by 5% in the public sector and by 6.8% in the private sector.