Charts of the Week

Charts of the week from 21 to 25 August 2023: economic sentiment, value of fiscally verified invoices, Slovenian industrial producer prices and other charts

The economic sentiment indicator improved slightly in August, while it remained lower year-on-year. The nominal value of fiscally verified invoices remained roughly unchanged year-on-year between 6 and 19 August, mainly due to lower turnover in trade. The monthly decline in Slovenian industrial producer prices continued in July and the year-on-year growth rate is also slowing further. The average wage in June was higher year-on-year in real terms. The increase in the public sector was more significant than in the private sector, mainly due to the wage increase agreed last year.

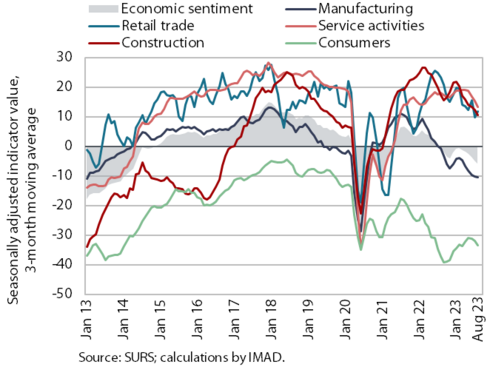

Economic sentiment, August 2023

The value of the economic sentiment indicator rose slightly in August, while it remained lower year-on-year. Compared to July, confidence was higher in retail trade and manufacturing, while it fell in construction, services and among consumers. Compared to August 2022, the value of the sentiment indicator was lower by 5.8 p.p. (according to original data). Confidence was lower in all segments except among consumers, but here the indicator is still well below its long-term average.

Value of fiscally verified invoices – in nominal terms, 6–19 August 2023

The nominal value of fiscally verified invoices between 6 and 19 August 2023 was similar to that in the same period last year. The result was weaker than in the previous 14-day periods, which may be partly related to lower sales after the floods that hit Slovenia in the beginning of August. Turnover in trade, which accounted for 68% of the total value of fiscally verified invoices, was 1% lower year-on-year. Turnover growth further moderated in accommodation and food service activities (to 3%) and in certain creative, arts, entertainment, and sports services and betting and gambling (total growth in other service activities was 4%).

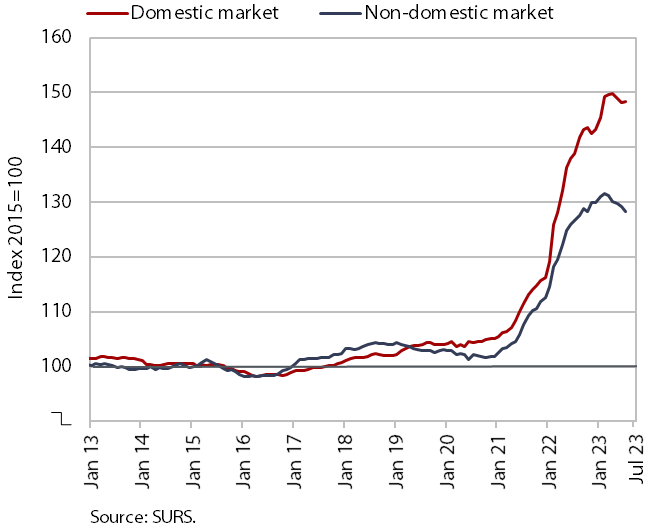

Slovenian industrial producer prices, July 2023

The monthly decline in Slovenian industrial producer prices continued in July. Compared to June, prices fell by 0.2%. They fell by 0.6% on foreign markets, while on the domestic market they rose by 0.2%. The year-on-year growth rate weakened further to 4.1%. Prices on the domestic market increased by 6.2% year-on-year and prices on foreign markets by 1.4%. Broken down by product group, the strongest year-on-year price increase was still in the energy group (by 17.2 %), and there was also a relatively strong increase in the consumer goods group (by 9% for durable goods and by 7.3% for non-durable goods). The prices of capital goods went up by 4.2% year-on-year, while the prices of intermediate goods by only 0.4%.

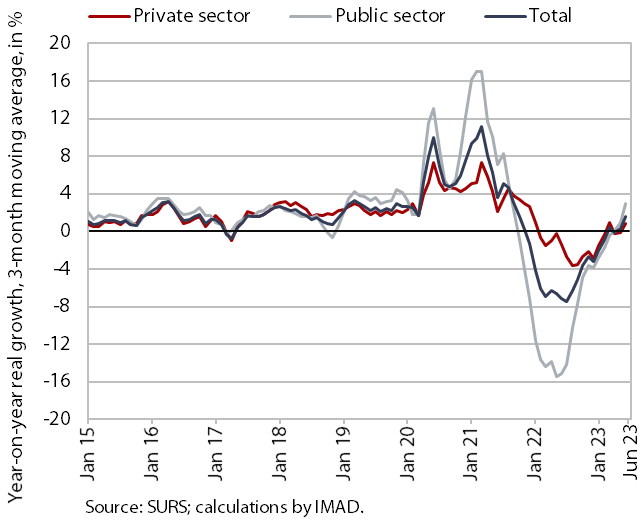

Average gross wage per employee, June 2023

The average gross wage increased by 2.8% year-on-year in real terms in June. In the private sector, the average gross wage increased by 1.9% year-on-year in real terms. Growth was strongest in administrative and support service activities, which face severe labour shortages. The average gross wage in the public sector increased by 4.4% year-on-year in real terms, mainly due to the last year’s agreement on wage increases. Compared to June last year, the average gross wage increased by 9.9% in nominal terms – by 11.6% in the public sector and by 8.9% in the private sector. In the first six months, the average year-on-year gross wage growth was 1% (0.9% in the private sector and 1.2% in the public sector).