Charts of the Week

Charts of the week from 20 to 24 February 2023: average gross wage per employee, Slovenian industrial producer prices, economic sentiment and other charts

The year-on-year decline in wages deepened slightly in December, and in 2022 as a whole the average wage fell by 5.6% in real terms. The year-on-year increase in Slovenian producer prices slowed further at the beginning of the year (to 18.2%). This was entirely due to a high base, as prices rose by 1.2% month-on-month. The value of the sentiment indicator in February remained roughly the same as in January, but was lower year-on-year. Confidence was lower among consumers, in manufacturing and construction, while it was higher in trade and services. In February, the nominal value of fiscally verified invoices was 14% higher year-on-year, by a good tenth in trade; growth remained relatively high also in services due to the low base.

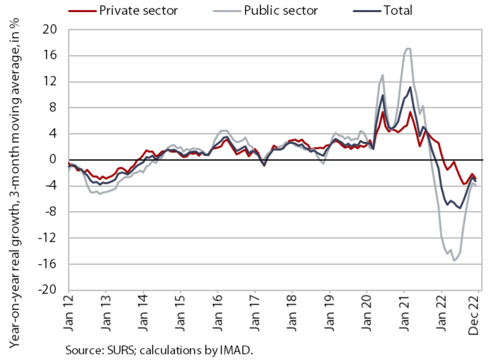

Average gross wage per employee, December 2022

Amid high inflation, the average gross wage fell by 5.2% year-on-year in real terms in December. The year-on-year decline was the same in both the private and public sectors and was more pronounced compared to the previous months. This was mainly due to a relatively high December 2021 base. Only administrative and support service activities recorded positive real wage growth in December. These are also among the activities experiencing above-average labour shortages. In 2022 as a whole, the average gross wage was 2.8% higher in nominal terms, but 5.6% lower in real terms (10.4% in the public sector and 2.4% in the private sector).

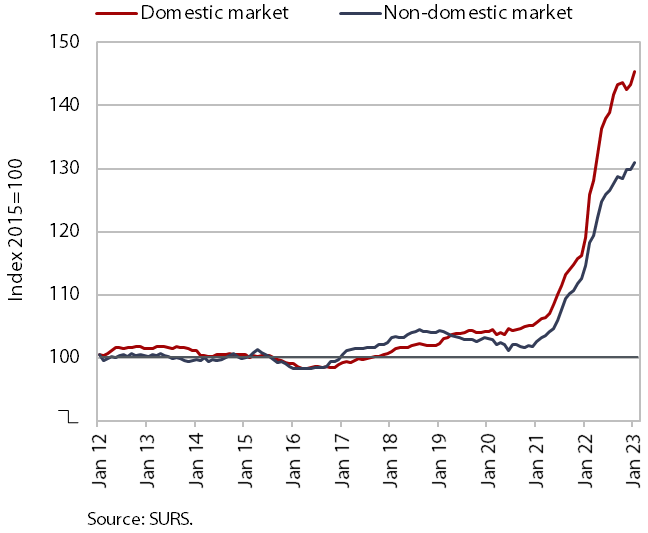

Slovenian industrial producer prices, January 2023

The year-on-year growth of Slovenian industrial producer prices continued to gradually weaken at the beginning of the year and stood at 18.2% in January. The slowdown was entirely due to last year’s high base, as prices rose by 1.2% month-on-month (prices of products increased in all industrial groups). This was the highest monthly increase since August 2022 and, in our estimation, was due to the conclusion of new business contracts at the beginning of the year. Price growth slowed year-on-year in both domestic (22.1%) and foreign markets (14.3%). Price growth in the groups intermediate goods (17.4%) and capital goods (9.4%) continues to weaken. Growth in the prices of energy (79.2%) and consumer goods (14.3%) remained broadly unchanged.

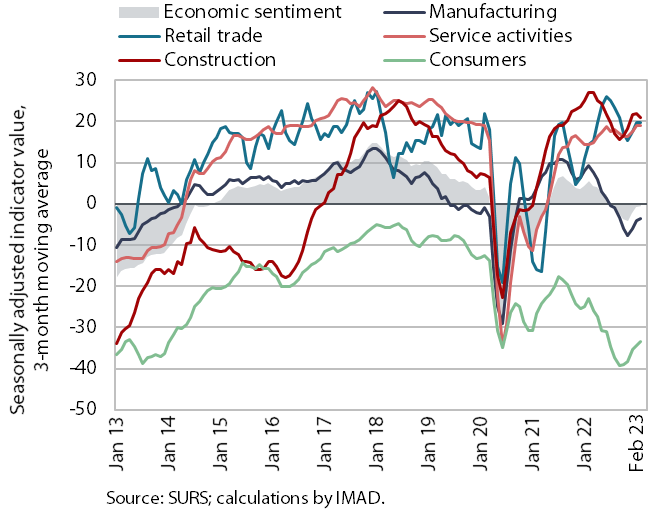

Economic sentiment, February 2023

The economic sentiment indicator remained broadly unchanged in February compared to January (-0.2 p.p.), while it was almost 8 p.p. lower year-on-year. Month-on-month, confidence fell slightly in manufacturing, retail trade and construction, while it rose among consumers and in services. Compared to February last year, confidence was lower among consumers, in manufacturing and construction. Lower consumer confidence is mainly related to the loss in the purchasing power due to high inflation and greater caution when deciding to make major purchases. Confidence in manufacturing is affected mainly by the current international environment (i.e. high commodity and energy prices and subdued expectations regarding future production and exports). Confidence in trade and services was slightly higher year-on-year due to last year’s peak of the COVID-19 epidemic in January–February and the operating restrictions in these sectors (recovered/vaccinated/tested rule, restrictions on opening hours, etc.).

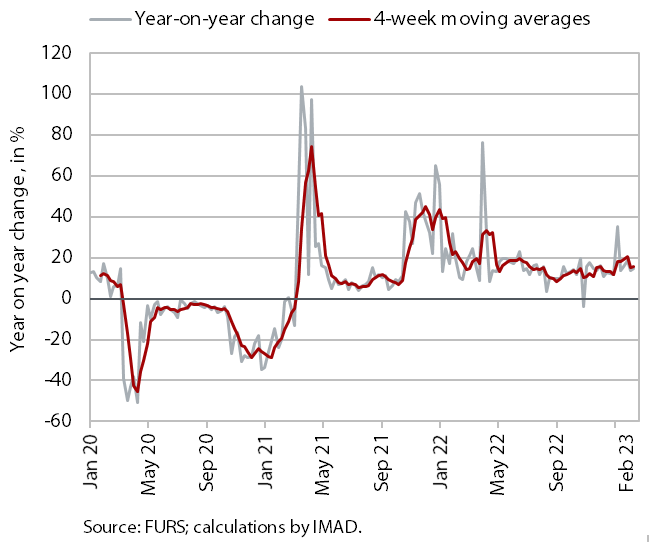

Value of fiscally verified invoices, in nominal terms, 5–18 February 2023

Amid high price growth, the nominal value of fiscally verified invoices between 5 and 18 February 2023 was 14% higher year-on-year. In trade (11% overall year-on-year growth), growth in the sale of motor vehicles weakened significantly (to 11%) after recording high growth at the beginning of the year, while growth in retail and wholesale trade remained largely unchanged from the end of last year (just over 10%). Nominal turnover growth remained high, although slightly lower month-on-month in accommodation and food services (31%), certain creative, arts, entertainment, and sports services and betting and gambling (total growth in other service activities was 40%).