Charts of the Week

Charts of the week from 19 to 23 December 2022: economic sentiment, Slovenian industrial producer prices and other charts

Economic and consumer sentiment continued to improve in December. The improvement in the economic sentiment indicator was mainly due to increased consumer confidence, which is attributable particularly to lower uncertainty related to energy supply this winter and measures to mitigate rising prices. Compared to last year, however, economic sentiment was still lower. The year-on-year growth in Slovenian producer prices slowed further in November, but remains relatively high. Amid high inflation, the average gross wage in October was lower year-on-year in real terms, but the decline was slightly less pronounced than in previous months.

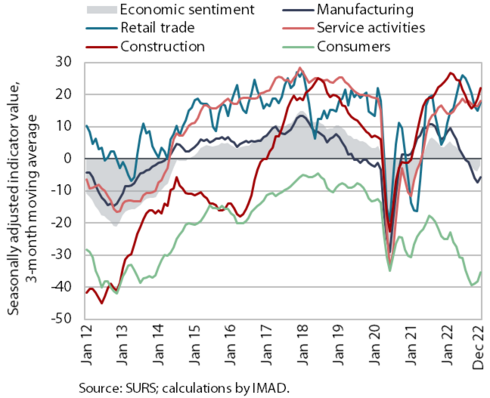

Economic sentiment, December 2022

The value of the Economic Sentiment Indicator rose for the second month in a row in December, but remained down year-on-year. However, the gap with the previous year was the smallest in seven months. Confidence rose for the second month in a row in all activities, but remained unchanged in services in December, while it was significantly higher among consumers. We assume that this is mainly related to lower uncertainty regarding the supply of energy this winter and measures to mitigate rising prices. Year-on-year, confidence remained higher in retail trade and services, while it was lower in manufacturing, among consumers and slightly in construction. In manufacturing, this is related to the current situation in the international environment (high prices of intermediate goods and energy, uncertainty about economic growth in Slovenia’s main trading partners), while lower confidence among consumers is related to lower purchasing power due to high prices.

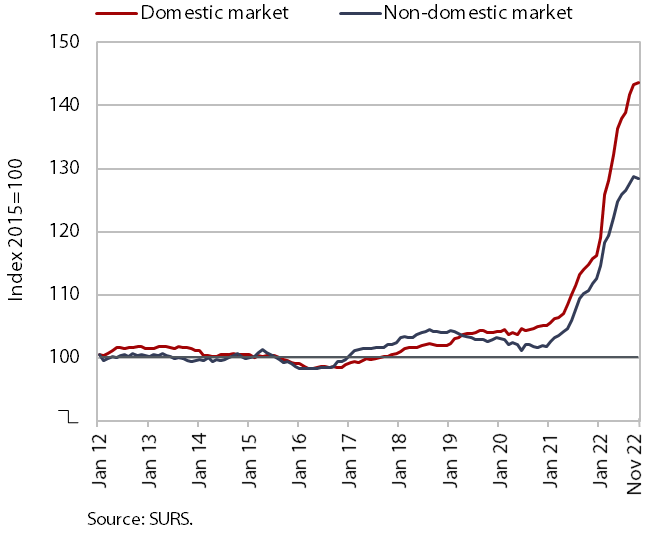

Slovenian industrial producer prices, November 2022

The year-on-year growth of Slovenian industrial producer prices continues to gradually weaken and was 19.7% in November. In November, price growth on the domestic market was lower year-on-year than in October (22.7%), while it strengthened slightly on foreign markets (16.2%). Amid a monthly price decline of about 7%, the year-on-year increase in energy prices has slowed down, but still amounts to almost 80%. However, price increases of intermediate goods continued to slow gradually in the face of subdued economic activity, with prices 21.3% higher year-on-year. After slowing in recent months, growth in prices for capital goods accelerated slightly in November (10.5%). The increase in consumer goods prices continues to strengthen (14%), especially of non-durable goods (14.4%), while price growth in durable goods remains at slightly above 12%.

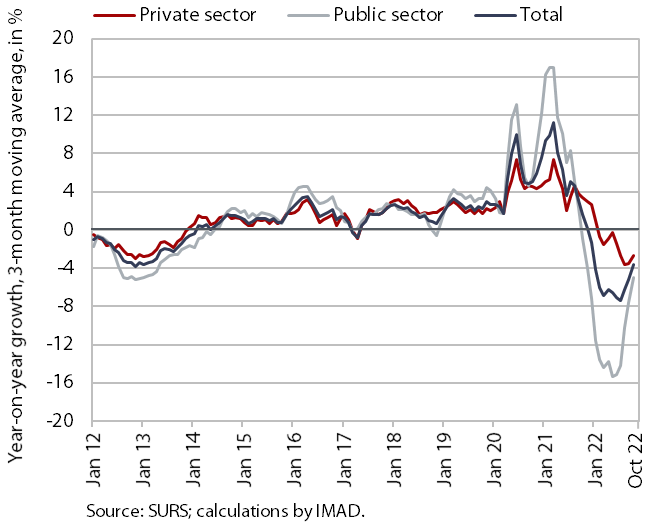

Average gross wage per employee, October 2022

Amid high inflation, the average gross wage fell by 2.4% year-on-year in real terms in October; the decline was more pronounced in the public sector than in the private sector. In the private sector, the year-on-year real decline (1.9%) was lower than in the previous months, while in transportation and storage, an activity with above-average labour shortages, wages increased year-on-year. In the public sector, the year-on-year real decline (3.1%) was also lower than in previous months, mainly due to the agreement on wage increases from October this year. The average wage in the health and social work activities was higher year-on-year in real terms, where wages also increased in December 2021 (though not for all employees). Compared to October last year, the average gross wage increased by 7.3% in nominal terms – by 6.5% in the public sector and by 7.9% in the private sector.

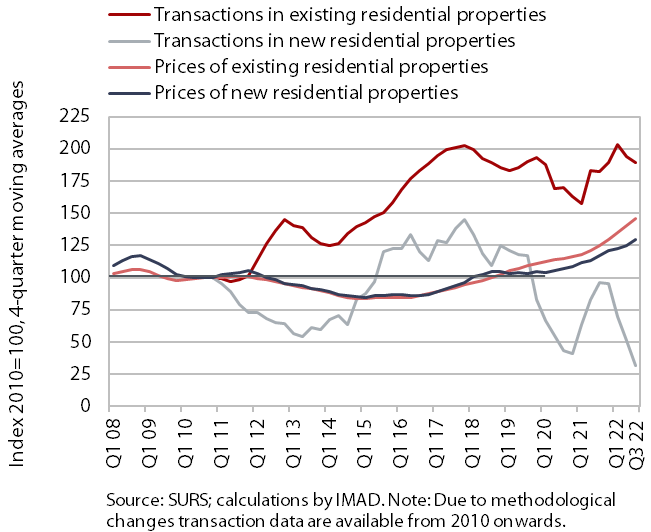

Real estate, Q3 2022

Amid a further decline in the number of transactions, the growth in prices of dwellings continued in Q3 2022. Prices increased by 2.4% compared to the second quarter and, following an increase of 11.5% in 2021 as a whole, were 15.4% higher year-on-year. The high growth was mainly due to higher prices of existing dwellings (by 15.6%), where the number of transactions was the lowest in 18 months (10% lower year-on-year). Prices of newly built dwellings were also higher (by 13.7%), but these dwellings accounted for only 1% of all transactions (39 transactions) due to insufficient supply. The total value of housing transactions for all types of dwellings sold in the third quarter was EUR 385 million, about 5% less than in the same quarter last year.