Charts of the Week

Charts of the week from 11 to 14 April 2023: production volume in manufacturing, activity in construction, current account of the balance of payments and other charts

Manufacturing output increased on average in January and February compared to the fourth quarter of last year. It remained largely unchanged year-on-year. It was higher in both high-technology industries, namely the manufacture of ICT equipment and, in our assessment, the pharmaceutical industry, but lower in other groups, especially in more energy-intensive industries. Construction activity further increased in February, with the construction of residential buildings in particular standing out compared to previous years. In March, electricity consumption in the distribution network was lower year-on-year in all consumption groups. As in previous few months, industrial consumption declined the most, which we estimate is mainly due to the fact that the energy-intensive part of the economy has adjusted to the high energy prices by increasing energy efficiency and reducing production. The 12-month current account surplus (until February) was lower year-on-year, amounting to EUR 154.1 million (0.2% of estimated GDP).

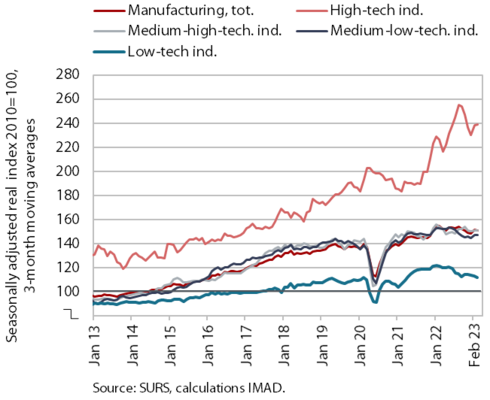

Production volume in manufacturing, February 2023

Manufacturing output in the first two months was higher than in the last quarter of last year and similar to the same period last year. Output was higher y-o-y in both high-technology industries (pharmaceutical industry and manufacture of ICT equipment), which are less affected by the slowdown in external demand growth and the energy crisis. Output was lower on average in all other industry groups in terms of technological intensity. In particular, it was lower in more energy-intensive industries and in the manufacture of motor vehicles. Output was lower than a year ago also in certain low-technology industries (wood-processing and furniture industries, other manufacturing, manufacture of wearing apparel) and – after high growth in 2022 – the manufacture of electrical equipment.

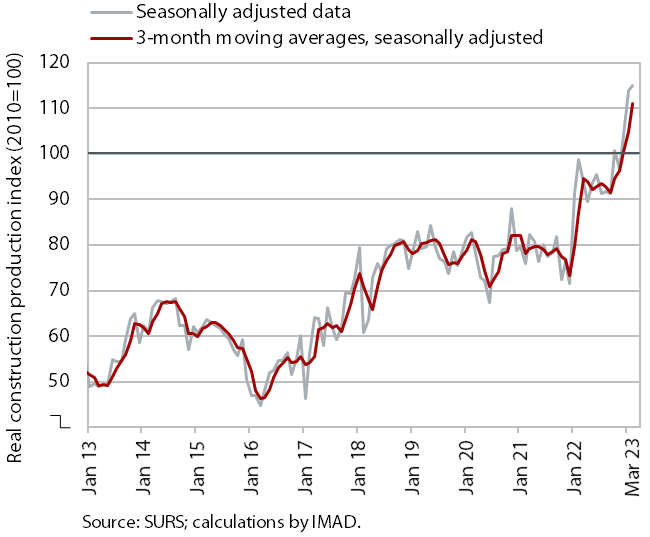

Activity in construction, February 2023

According to data on the value of construction work put in place, construction activity further increased in February. After a sharp upturn at the beginning of 2022, the value of construction work remained roughly unchanged throughout the year before rising sharply towards the end of last year and the beginning of this year. In February, it was 18% higher year-on-year. Compared to previous years, construction of buildings, especially of residential buildings stood out in terms of the level of activity. The implicit deflator of the value of construction work put in place used to measure prices in the construction sector was 12% in February, which was slightly below the 2022 average.

However, some other data suggest significantly lower growth in construction activity. Data on the value of industrial production in two activities traditionally strongly linked to construction do not point to such high growth. Production in other mining and quarrying was 2% lower in February than in the same month of 2022, while it was 7% lower in the manufacture of other non-metallic mineral products.

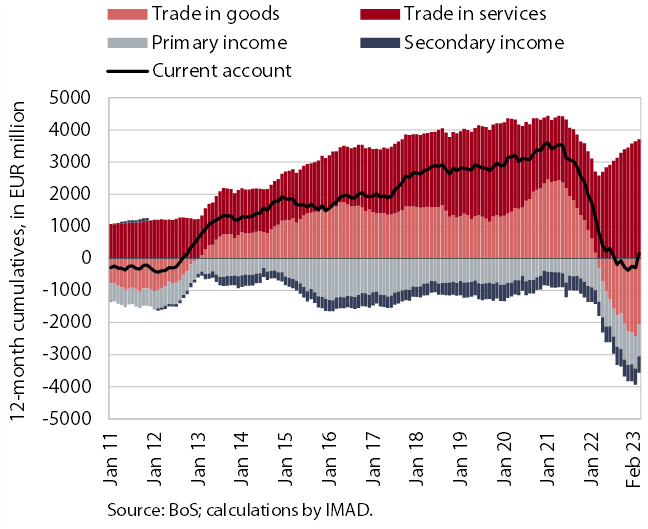

Current account of the balance of payments, February 2023

The 12-month current account surplus (until February) was lower year-on-year, amounting to EUR 154.1 million (0.2% of estimated GDP). The lower surplus was largely attributable to the goods trade balance, which turned from a surplus to a deficit in March last year. The primary income deficit was similar to the previous year, while the secondary income deficit was higher year-on-year due to lower receipts from the EU budget and higher VAT- and GNI-based contributions to the EU budget. The surplus in trade in services continued to increase, especially in trade in travel and transportation services.

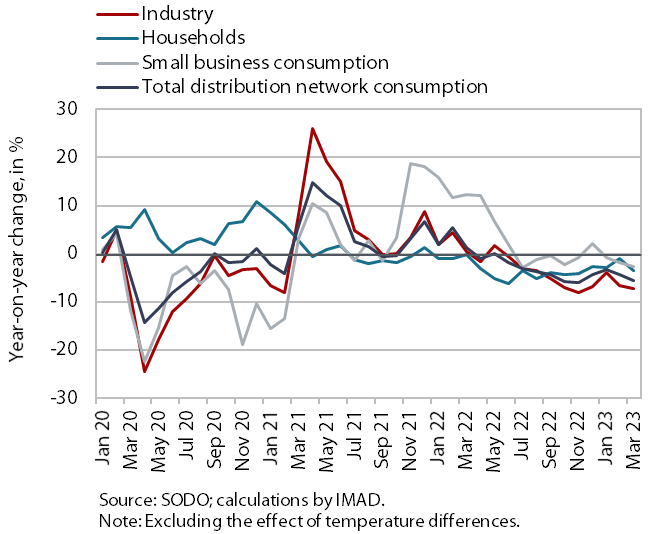

Electricity consumption by consumption group, March 2023

In March, electricity consumption in the distribution network was lower year-on-year in all consumption groups. As in previous months, industrial consumption declined the most (by 7.2%), which we estimate to be mainly due to the energy-intensive part of the economy adjusting to high energy prices by increasing energy efficiency and reducing production. Household consumption was also lower in March than a year earlier (by 3.6%). We estimate that this is due to a more rational energy consumption and the impact of COVID-19 measures (remote work, isolations and absences due to illness) on higher base of last year. Small business consumption was 2.6% lower year-on-year in March.

Road and rail freight transport, Q4 2022

In the last quarter of last year, the volume of road freight transport remained similar to the previous quarter, while the volume of rail freight transport decreased significantly. The volume of road transport performed by Slovenian vehicles decreased slightly quarter-on-quarter due to lower cross-trade, and was 4% below the level of the same quarter in 2019 (cross-trade was 20% lower, while other road traffic performed at least partially on Slovenian territory was 12% higher). With the decline in the volume of cross-trade performed by Slovenian vehicles, its share in total traffic also fell sharply (to 43%) and was again significantly lower than in the pre-epidemic period (when it was 51%). Rail freight transport, already declining before the epidemic, was 8% lower than in the same quarter of 2019.