Slovenian Economic Mirror

Slovenian Economic Mirror 3/2020

In March, the consequences of the coronavirus epidemic and the measures taken to contain its spread already had a significant negative impact on activity in both the euro area and Slovenian economy. The spread of the epidemic in neighbouring countries and main trading partners contributed to a fall in demand and disrupted supply chains. In the middle of the month, Slovenia adopted measures that, among other things, banned all non-essential service activities. Some enterprises decided to shut down production. Transport by domestic and foreign trucks also declined strongly. A fall in economic activity is also indicated by data on electricity consumption, which has been around one fifth lower year on year since the middle of March. Labour market conditions also began to deteriorate in the middle of March, with the number of unemployed persons starting to increase more noticeably. In the second half of April and the beginning of May, the increase moderated somewhat. In total, 88,648 persons were unemployed at the end of April, one fifth more than one year earlier, and by 10 May their number increased to 89,635 according to unofficial EES data. In April, confidence continued to deteriorate strongly in all sectors. Consumer confidence also fell to a 15-year low.

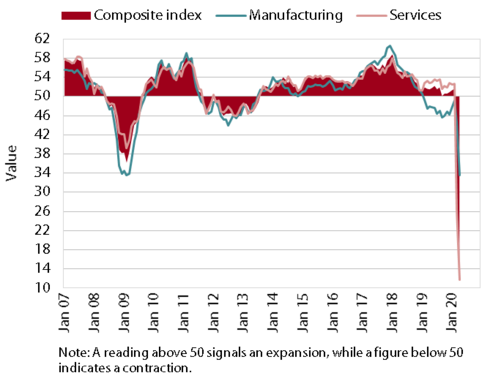

The composite Purchasing Managers’ Index (PMI) for the euro area

Economic sentiment in the euro area continued to deteriorate strongly in April, which points to a significant decline in economic activity in the first half of the year. With the largest monthly decline thus far, the composite PMI fell to an all-time low and was thus significantly lower than in 2009. Confidence in service activities reached its lowest level since records began, while the indicator for manufacturing fell to roughly the same level as at the time of the global financial crisis. The economic sentiment indicator (ESI) recorded the steepest monthly decline since the beginning of measurement and approached the values seen during the economic and financial crisis in 2009. Confidence fell sharply in all sectors and among consumers, most notably in service activities and trade. As a result of lower demand and extensive lockdowns in the economy, euro area GDP contracted by 3.8% in the first quarter compared with the previous quarter, according to Eurostat’s flash estimate, which is the sharpest decline since records began. In the second quarter, it is set to contract even more, judging by confidence indicators.

IMF forecasts for economic growth

International institutions predict a recession of historic proportions for the global economy this year. Recession will affect both advanced and developing countries. According to IMF and EC forecasts, the euro area economy will contract by 7.5%–7.7% this year under the assumption of a slowdown in the epidemic, and then recover by 4.7%–6.3% next year. All euro area countries will experience a recession, but the drop in economic activity in 2020 and its rebound in 2021 are expected to differ markedly. The EC predicts that the unemployment rate in the euro will increase from 7.5% to 9.5% this year, before falling slightly again in 2021. Inflation (HICP) in the euro area will total only 0.2% this year (1.1% in 2021) according to EC forecasts, given the decline in demand and the fall in oil prices. The forecasts of institutions are associated with exceptionally high uncertainty and mostly negative risks, as a longer lasting epidemic or a new outbreak could have a far greater negative impact on economic growth.

Prices of Brent Crude

In April, oil prices plummeted to record lows. The average dollar price for a barrel of Brent crude fell by 43% at the monthly level in April, to USD 18.5, the lowest value since June 1999. Dollar prices of oil were 74% lower year on year. The decline in euro prices was similar. The plunge in oil prices was mainly due to low demand and thus excess supply of oil on global markets and the price war between the world’s top oil producers. International institutions expect oil prices to remain low and volatile until the imbalance between supply and demand is eliminated.

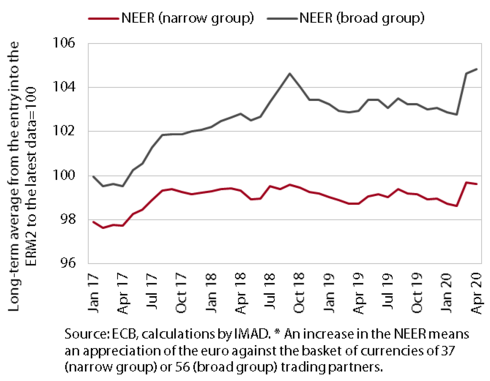

Nominal effective exchange rate

Following a more marked depreciation of the currencies of individual trading partners against the euro, the nominal effective exchange rate stabilised in April. The spread of the coronavirus across the world has also caused major exchange rate fluctuations. In March, a significant depreciation against the euro was experienced particularly by currencies of energy exporting countries (e.g. Russia), countries with previously unstable macroeconomic and financial environments (e.g. Turkey) and the United Kingdom (as a consequence of Brexit-related uncertainties). The exchange rate of the euro against safe haven currencies such as the US dollar, the Swiss franc and the Japanese yen remained relatively stable. In April, exchange rate fluctuations were generally less pronounced. The nominal effective exchange rate, which indicates the ratio of the euro to a basket of currencies of trading partners weighted by their importance in Slovenia’s foreign trade, remained similar to that in March.

Short-term indicators of economic activity

The spread of the coronavirus and the adoption of measures to contain the epidemic affected activity in most sectors, particularly certain market services. Owing to the ban on most service activities, turnover in non-essential trade segments fell in March. A significant fall in turnover is therefore also expected in accommodation and food service activities, which will also be affected by the plunge in tourist arrivals. Through a decline in foreign demand and disruptions in supply chains, the coronavirus epidemic in Europe had a significant adverse impact on production volume in manufacturing and exports of goods. The decline in economic activity in mid-March is also confirmed by data on electricity consumption, which in Slovenia has been around one fifth lower year on year since the outbreak of the epidemic. Freight traffic on Slovenian motorways also declined in the same period. It has increased gradually with the easing of measures after Easter, but remains markedly lower year on year.

Trade in goods with the EU – real

Trade in goods, especially with EU countries, declined markedly in March with the spread of the coronavirus epidemic. After goods exports to EU countries had already been slowing gradually for several months, the noticeable decline in March was mainly due to measures to contain the epidemic in Slovenia’s main trading partners. The sharpest decline was recorded for exports to Italy, where, in addition to the closure of most shops, all non-essential production came to a standstill in the second half of the month. Owing to disruptions in international transport, significantly worse expectations about orders and the adoption of measures to contain the epidemic in Slovenia, imports also fell markedly in March.

Trade in services – nominal

Growth in trade in services already slowed down before the epidemic spread. As a result of the slowdown in international trade, growth in exports of transport services, which account for more than a quarter of total services exports, eased significantly in the first two months of this year. The beginning of the coronavirus epidemic in neighbouring countries did not yet have any visible impact on transport and tourism in February, as spending by foreign tourists, same-day visitors and transit passengers remained similar to last year. On the other hand, the first two months recorded much stronger growth in exports and imports of ICT services, especially services related to information activities. Growth in imports of services also eased under the influence of the slowdown in international trade.

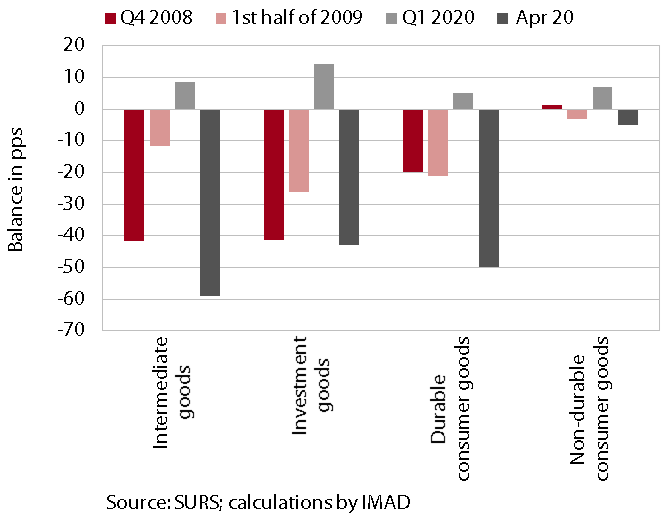

Production volume in manufacturing, by industrial group

Manufacturing output declined sharply with the spread of the coronavirus in March. Due to a decline in foreign demand and disruptions of supply chains, production fell in most industrial groups, as some companies decided to halt production. The decline was most pronounced in industries producing investment goods and durable consumer goods and somewhat smaller in those producing intermediates. Meanwhile, growth continued in industries that produce non-durable consumer goods, such as food and pharmaceuticals.

Indicator of expected exports of manufactured goods, by industrial group

Manufacturing companies’ expectations deteriorated considerably under uncertain economic conditions at the beginning of the second quarter, the least in the production of non-durable consumer goods. Most indicators of expectations, but also of the current situation, reached similarly low or lower values than at the end of 2008 and in the first half of 2009. Most of the enterprises surveyed were already pessimistic about production in the second quarter in March, and their share increased significantly in April. Export orders, which to a great extent determine the volume of production, as manufacturing activities are highly oriented to exports, were lower than usually in April in most of the enterprises surveyed. The share of enterprises reporting lower export orders was highest in the production of investment goods, but these enterprises were less pessimistic about foreign demand and production in the coming months than enterprises that produce intermediate goods and are highly integrated into global value chains and enterprises that produce durable consumer goods. Those that produce non-durable consumer goods have so far been the least affected by the current situation. Despite a similarly low value of the indicator of new export orders as in other groups, these enterprises are on average the least pessimistic about future foreign demand, production and employment.

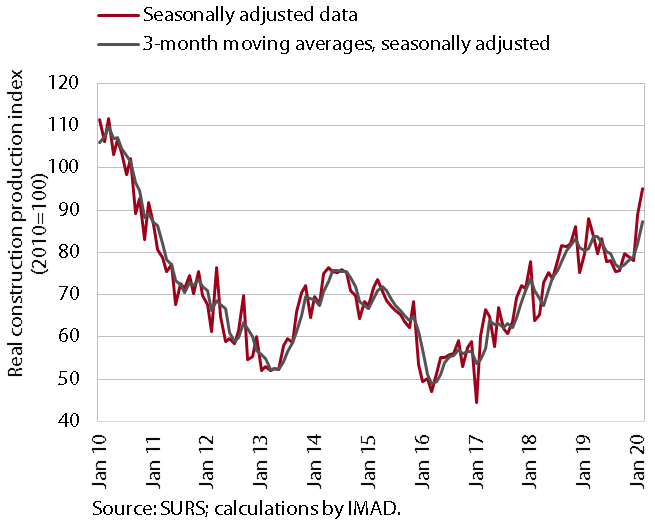

Activity in construction

After a decline in the middle of last year, construction activity increased towards the end of the year and intensified further at the beginning of 2020. Activity increased in all three construction segments, most notably in the construction of civil-engineering works, but also in the construction of non-residential and residential buildings. New contracts and the stock of contracts, which are the indicators of future activity in construction, dropped in the first half of last year before strengthening in the second. Favourable developments also continued in the first two months of this year, when the coronavirus had not yet spread to Europe.

Turnover in trade

At the beginning of the year, turnover in trade remained similar to that at the end of last year, while in March it fell sharply in some segments. The favourable developments in the first two months reflected further moderate growth in private consumption and strong activity in some trade-related sectors (manufacturing, construction, transport, etc.). With the spread of the coronavirus epidemic in Slovenia and the closure of shops selling non-essential goods in the middle of March, the situation in the trade sector changed significantly. Turnover in the sale of food products, which had already increased significantly in February under the impact of uncertainty, rose further in March according to preliminary data. On the other hand, due to the closure of shops selling non-essential goods, turnover in retail sales of non-food products and motor vehicles dropped sharply in March (by more than a quarter and more than a third respectively).

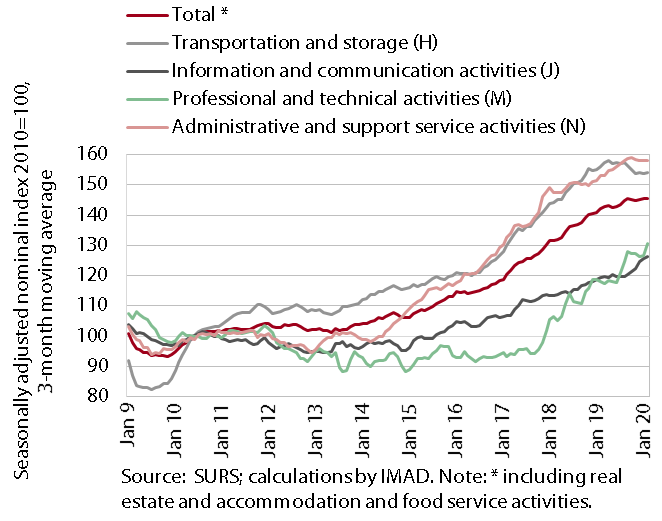

Real turnover in market services

The weak growth of turnover in market services continued in February, when the impact of the coronavirus spread was not yet felt, but we expect a decline in the coming months. In February, turnover in transportation and administrative and support service activities remained at the same level as at the end of last year. With rising export revenues in computer services, turnover growth in information and communication activities remained high. Because of considerable growth in architectural and engineering services, growth in professional and technical activities even accelerated. We expect that the decline in economic activity in Slovenia and the EU in March and April will have a significant negative impact on service activities (especially transportation and business activities).

Selected indicators of private consumption

Further growth in household consumption was interrupted by a declaration of epidemic in the middle of March. Amid further growth in disposable income, household consumption increased further in the first two months of the year. The increase in household resources reflected the growth of the net wage bill (also due to the increase in the minimum wage and a change in personal income tax rates) and social transfers paid during this period. With more resources available, households strengthened expenditure on most non-food products, catering services and, amid rising uncertainty, food and beverages. According to preliminary data, the consumption of food and beverages also increased further in March, while the consumption of other types of goods and services dropped markedly with the introduction of measures to contain the coronavirus epidemic.

Selected indicators of tourism

Because of the coronavirus epidemic, the number of tourist arrivals plunged in March, which will affect turnover in accommodation and food service activities; this had otherwise increased further in February. February’s growth was related to further spending by the domestic population and the increase in overnight stays and consumption of foreign tourists, same-day visitors and transit guests. In February the coronavirus epidemic was reflected only in a fall in overnight stays of Asian tourists in Slovenia (year on year almost by one fifth), while the number of all foreign tourist overnight stays together was 3.7% higher than one year earlier. With the spread of the coronavirus in Europe and the closure of all hotels and restaurants in Slovenia, the number of all overnight stays dropped by two thirds year on year in March, which will have a significant impact on turnover in accommodation and food service activities.

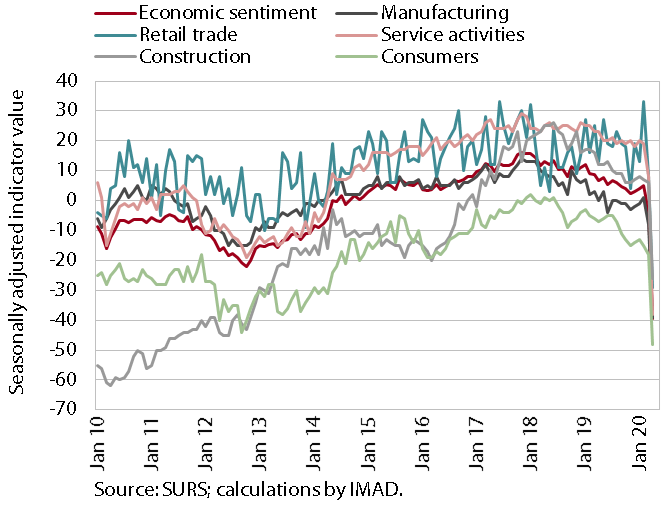

Economic sentiment

Confidence in the economy deteriorated strongly in April, reaching a 15-year low. Due to the spread of the coronavirus epidemic, all activities recorded not only a significant deterioration in the situation indicators, but also a sharp decline in expectations. Confidence dropped the most in service activities and retail trade. In April, it was lower in all activities (with the exception of construction) than ten years earlier, during the economic and financial crisis. Consumer confidence also fell, to its lowest level since the first measurement (since 2005).

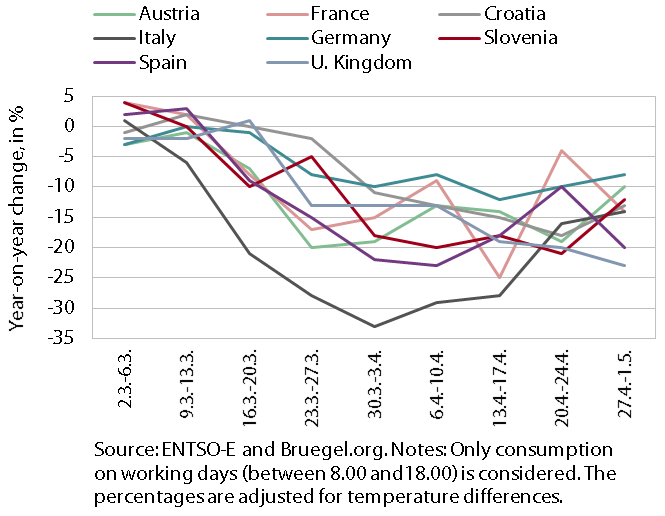

Electricity consumption

Electricity consumption decreased with the shutdown of public life and part of production due to the coronavirus epidemic. Electricity consumption, one of the indicators of economic activity, began to fall with the declaration of the epidemic in the third week of March, when it was 10% lower year on year. The decline then increased to around 20% by the beginning of April and remained roughly unchanged for most of the month before dropping to 12% in the last week of April. Of the selected countries shown in the chart, Italy, the first coronavirus hotspot in Europe, recorded the largest decline in consumption since the beginning of the epidemic (even more than 30% in an individual week). In most other countries, consumption fell by around 20%. Germany stands out in this comparison, with consumption generally falling by no more than 10%. With the easing of some containment measures at the beginning of April, the decline started to decrease more markedly especially in Italy and Spain, and towards the end of April, also in some other countries.

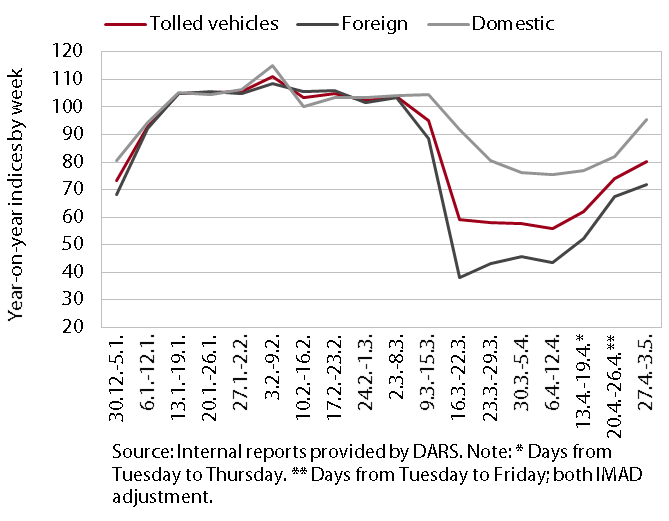

Traffic of electronically tolled vehicles on Slovenian motorways

Freight traffic on Slovenian motorways, which has fallen markedly since the declaration of the epidemic, started to increase again in the middle of April. After a more than 40% decline in the first weeks following the declaration of the epidemic, it was around a fifth lower in the week of the Labour Day holidays compared with the same period of last year. The distance of journeys performed by foreign trucks was approximately 30% lower year on year, while that performed by domestic trucks already approached the levels seen before the epidemic. The decline in foreign truck traffic, which was significantly larger than in domestic truck traffic at the beginning of the epidemic, decreased under the impact of EU measures to ensure the free flow of goods across borders and due to the relaxation of measures in some neighbouring countries.

The number of employed persons and the number of registered unemployed persons

Labour market conditions have rapidly deteriorated since the adoption of measures to contain the coronavirus epidemic in the middle of March. In the first two months of this year, the number of persons in employment was still 1.6% higher year on year (most notably in construction and in transportation and storage activities), which is half less than in the same period of 2019. Before the epidemic, employment increased mainly due to the hiring of foreigners amid a shortage of domestic workers. After the outbreak of the epidemic in Slovenia, registered unemployment started to rise rapidly in the second half of March and was higher at the end of the month than at the end of February. Although its rapid increase slowed in the second half of April, the number of unemployed persons amounted to 88,648 at the end of April, 19.9% more than one year before and 14.4% more than in February 2020. The slowdown in growth seen in recent weeks could be related to the expected easing of some containment measures and the adoption of the second legislative package to alleviate the economic impact of the crisis.

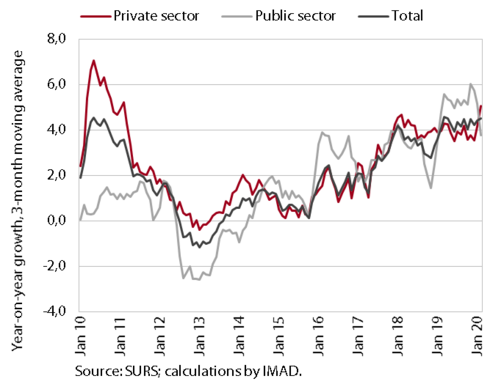

Average gross wage per employee

Year-on-year wage growth continued in the first two months. Wage growth in the private sector was higher year on year (5.7%; last year 4.3%); amid the still relatively low unemployment and the shortage of workers, it was also attributable to January’s increase in the minimum wage according to the Minimum Wage Act from 2018. Wages rose the most in some activities with above-average shares of minimum wage recipients (manufacturing, administrative and support service activities, trade and accommodation and food service activities). The increase in the minimum wage also contributed to wage growth in the public sector, but this was considerably lower than last year due to a lower volume of promotions paid at the end of the year (3.2%; last year 5.2%).

Consumer prices

Consumer prices were lower year-on-year in April. The consequences of countries’ measures to stem the spread of the coronavirus epidemic significantly contributed to a decline in prices of oil products, while the Slovenian Government measures also led to a fall in electricity prices. Together they contributed 2.2 percentage points to deflation. Without the adjustment of excise duties on oil products, the negative contribution would have been a further 0.1 of a percentage point higher. Durable goods prices remained lower year on year (–2%). This time prices of semi-durable goods also declined year on year (–2.8%). We estimate that this is to a great extent due to differences in data collection due to the closure of a large part of this type of stores and, partly, to lower demand for such goods. Food price growth continued to strengthen under the impact of increased demand and exceeded 5%. Growth in prices of services slowed further. However, for a certain part of prices that vary depending on the season (package holidays, accommodation services, flights), monthly changes from April 2019 were taken into account as data collection was not possible due to the measures to contain the epidemic.

Slovenian industrial producer prices

Slovenian industrial producer prices were lower year on year in March (by 0.6%), for the first time in more than three years. The fall was mainly due to a pronounced moderation of price growth on the domestic market, where electricity prices declined due to the government measures to mitigate the consequences of the epidemic. The drop of raw material prices also deepened slightly. The growth of consumer goods prices strengthened somewhat further. On foreign markets, the decline in Slovenian producer prices increased slightly again, mostly due to a larger decline in prices of consumer goods.

Current account

The current account surplus in the twelve months to February was the highest to date, at EUR 3.5 billion (7.0% of estimated GDP). In comparison with the same period one year before, the higher surplus continued to arise mainly from a higher surplus in external trade in services, particularly the surplus in trade in travel, telecommunication, computer, information and construction services. The higher surplus in goods trade reflected the strengthening of net exports of goods under merchanting. Net outflows of primary income were lower particularly due to lower net payments of income on equity. Net payments of interest on external debt were also lower. The deficit in secondary income was also down year on year, primarily on account of February’s lower VAT- and GNI-based contributions to the EU budget.

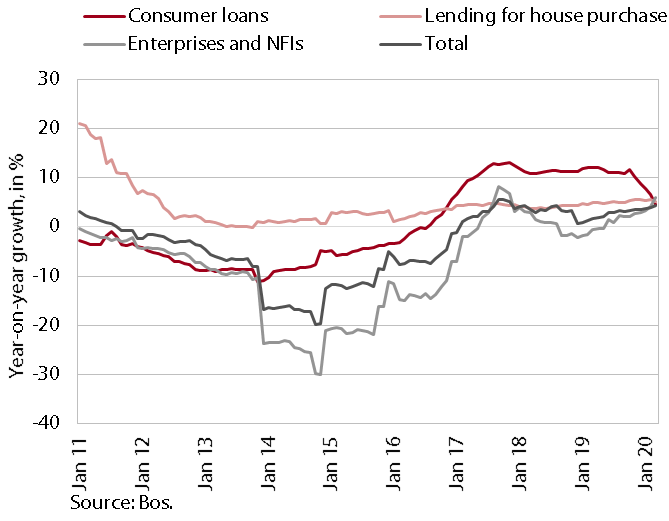

Year-on-year growth rates of loans in the Slovenian banking sector

As a result of rising corporate borrowing, year-on-year growth in loans to domestic non-banking sectors continued to strengthen gradually in the first three months. While a somewhat more pronounced strengthening of corporate borrowing has already been observed since the beginning of this year, the monthly growth in March was among the highest in the last 12 months. Household borrowing has gradually slowed since the introduction of a binding macroprudential instrument, mainly due to a marked slowdown in the growth of consumer loans, which fell by almost two thirds, to 4.5%, in the five months from November 2019 to March 2020. The growth of housing loans remained above 5%. Deposits of domestic non-banking sectors continued to grow at a more than 6% rate. The rapid growth of overnight deposits, which already account for almost three quarters of all non-banking sector deposits, continued. The share of arrears of more than 90 days in the banking system remained slightly above one percent in the first two months. However, there is a high risk, despite the intervention measures, that it will start rising again due to the deterioration in economic conditions at the outbreak of the epidemic.

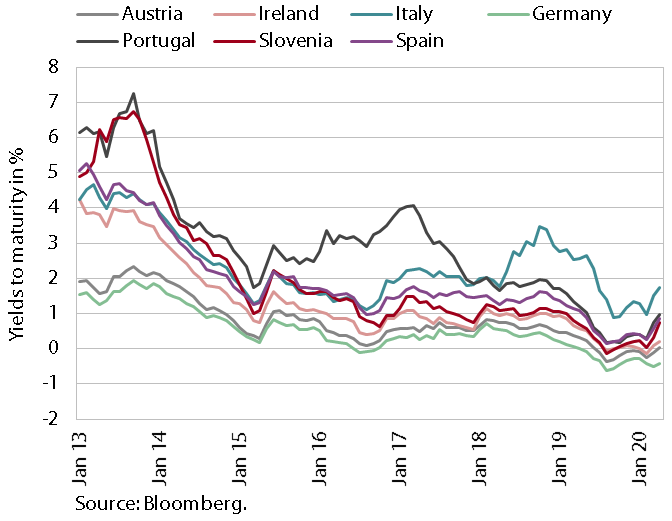

Yields to maturity of ten-year government bonds

Yields to maturity of euro area government bonds increased in April due to the coronavirus epidemic. Because of the high level of uncertainty, part of demand shifted to safer investments, including bonds of core euro area countries. Amid increased borrowing requirements of all countries, only yields to maturity of peripheral countries thus increased more noticeably. The rise in the yield to maturity of Slovenian bonds was among the most pronounced, as it more than doubled in April compared with March, its spread to the German bond reaching 120 basis points.

Revenue of the consolidated general government budgetary accounts

Owing to a decline in tax revenue, the deficit of the consolidated balance of public finance doubled year on year in the first quarter. Total revenue growth derived mainly from social contributions. Non-tax revenues were also higher. Owing to a decline in tax revenues as a result of lower revenues from VAT and excise duties, where the consequences of the coronavirus epidemic first became apparent, total revenue increased significantly less than in the first quarter of last year. Among tax revenues that were higher year on year was revenue from corporate income tax, which increased as a result of advance tax payments for 2019, while the growth of revenue from personal income tax slowed significantly as a result of the adopted changes to lower the tax burden on taxpayers. Receipts from the EU budget dropped year on year. Half of them were resources for the implementation of the Common Agricultural Policy.

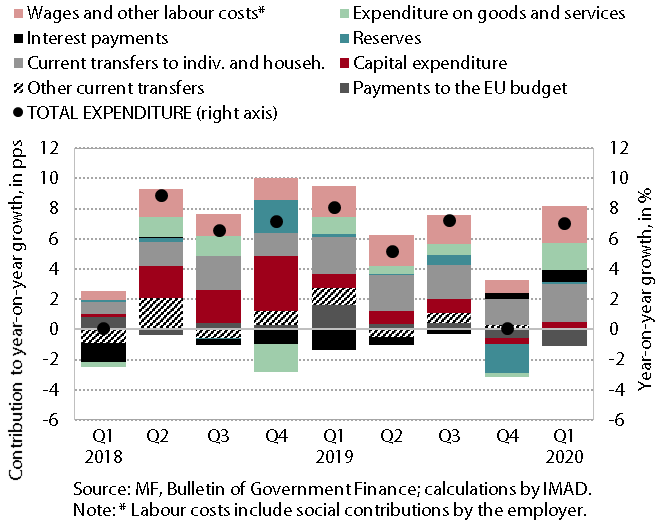

Expenditure of the consolidated general government budgetary accounts

Expenditure growth in the first quarter of 2020 was only slightly lower year on year and for the most part did not yet reflect the consequences of the epidemic. It arose mainly from increased transfers to individuals and households, where it was similar to that last year, and from growth in wages and other employee compensation, where it strengthened slightly. The wage bill increased under the impact of higher payments on the basis of the adopted agreements and higher funds for wages paid by the ZZZS to public health institutes. As a result of the increased ZZZS transfers to public institutes, the growth of expenditure on goods and services also strengthened considerably in the first quarter. On the other hand, the growth of investment more than halved in the first quarter and was solely a result of local government investment. In the remainder of the year, total expenditure growth is expected to strengthen, while revenue will decline year on year, which will increase the deficit of the consolidated balance and the broader government sector. According to the estimate of the Stability Programme 2020, the general government deficit (according to ESA methodology) will reach 8.1% of GDP this year.

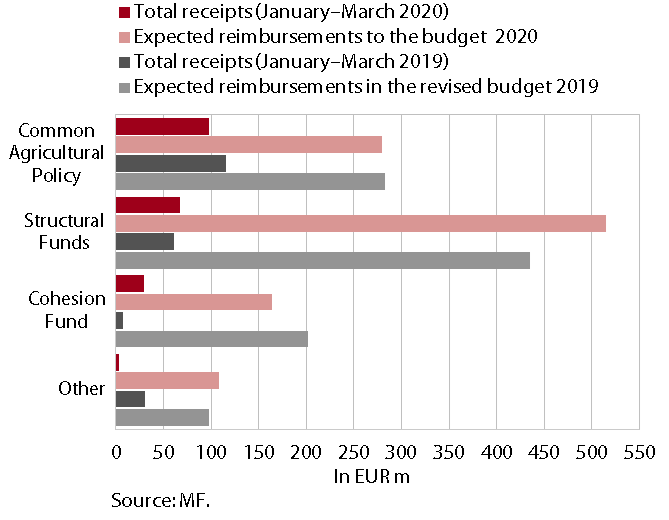

Receipts from the EU budget, January – March 2019 and 2020

Slovenia’s net budgetary position against the EU budget was positive in the first quarter (EUR 43.9 million), largely due to the March receipts for the implementation of the Common Agricultural and Fisheries Policy. In the first quarter, the bulk of receipts were thus funds for the implementation of the Common Agricultural and Fisheries Policy (EUR 97.8 million – 35% of the revenue planned in the budget), which are above average each March mainly due to direct payments to farmers. From the structural funds, the state budget received EUR 67.5 million in the same period (13.1% of the revenue planned) and from the Cohesion Fund, EUR 29.3 (17.9% of the revenue planned). In the first quarter, Slovenia’s receipts from the EU budget amounted to EUR 197.9 million, while its payments to the EU budget amounted to EUR 154.0 million.