News

Slovenian Economic Mirror: In the first months of 2019, favourable economic developments in most sectors; uncertainties in the international environment are lowering expectations

In the last month international institutions again lowered slightly their forecasts for this year’s economic growth in the euro area. This year uncertainties in the international environment have not yet significantly affected the Slovenian economy. Business expectations are however declining. Given the expected developments in main trading partners in the euro area and deteriorating business expectations regarding production volume and export demand, growth in exports and manufacturing is expected to ease off in the remainder of the year. Activity in sectors that are largely dependent on domestic demand continued to increase at the beginning of the year.

GDP growth in the euro area remained modest in the first quarter, and international institutions have lowered their forecasts for economic growth for this year slightly again in the last month. According to Eurostat’s preliminary flash estimate, GDP in the euro area rose by 0.4% (seasonally adjusted) in the first quarter, which is less than in previous years, but somewhat more than expected. Its growth was mainly driven by domestic demand (construction, private consumption). Confidence indicators remain relatively low, which is also one of the factors contributing to further downward revisions of the forecasts by international institutions, particularly for this year. Growth of the global economy and trade will slacken this year according to IMF and EC forecasts. In its latest forecast, the EC expects a 1.2% increase in euro area GDP this year (0.1 pps less than projected in the winter forecast), and than somewhat stronger growth again in 2020 (1.5%). However, both institutions emphasize that downside risks to the forecast remain elevated, outweighing upside risks.

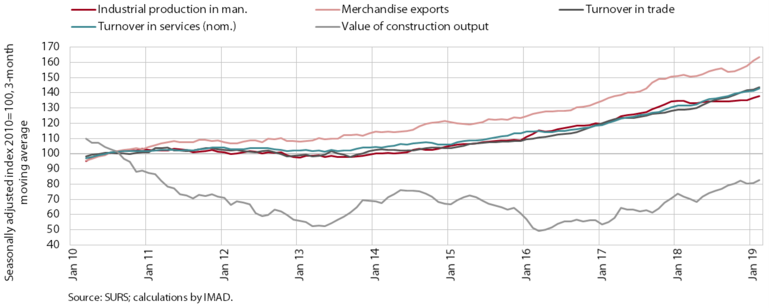

Picture: The movements of economic activity in Slovenia were favourable in most sectors at the beginning of the year

This year the Slovenian economy has not yet been significantly affected by uncertainties in the international environment; business expectations are however declining. The favourable developments in the export-part of the economy at the beginning of the year continue to reflect the accelerated growth in the manufacture of pharmaceutical and medical products. However, owing to modest activity in the EU car industry, exports and the production of motor vehicles and some intermediate goods are lower year on year. Given the expected developments in main trading partners in the euro area and deteriorating business expectations regarding production volume and export demand, growth in exports and manufacturing is expected to ease off in the remainder of the year.

The beginning of the year recorded further activity growth in sectors that are more dependent on domestic demand. The situation is improving in the service part of the economy, with turnover rising in trade, as well as, at accelerated pace, in most market services. Increased spending of domestic and foreign tourists has a favourable impact on accommodation and food service activities. A significant contribution to service sector growth is also coming from road transport and computer services. The prospects for trade and service activities remain favourable, despite a deterioration in the last month. Significantly stronger growth was also recorded for the value of completed works in construction, residential construction in particular, where activity follows the increase in the number of building permits in the past months. The higher activity in construction in February was however also due to the favourable weather conditions.

Labour market conditions improved further at the beginning of the year, which was reflected in stronger growth in disposable income. The rising demand for labour contributed to high employment, with the rising contribution of the recruitment of foreign workers and a further decline in registered unemployment. Wage growth was also notably higher, in the private sector also under the impact of the increase in the minimum wage, amid good business performance, gradual productivity growth and labour shortages. Wage growth in the public sector was a consequence of the agreed rises of wages for the majority of public servants and promotions. With stronger growth in disposable income and consumer loans, household spending also continued to increase at the beginning of the year, which is also reflected in higher prices of services. These account for more than two thirds of total consumer price growth, which reached 1.7% year on year in April.

The situation in the banking system is stable; the volume of loans to domestic non-banking sectors is steadily rising. Household borrowing is on the rise. Corporate borrowing is not rising, as firms are also financing current operations and investment from other sources. The quality of bank assets has also improved further under the impact of favourable economic conditions and the further cleaning of bank balance sheets.

The deficit of the consolidated balance of public finances in the first quarter was similar to that in the same period of last year, while long-term movements indicate a surplus, which is also expected for the end of the year. Revenue growth strengthened in the first quarter (8.3%) as a consequence of revenue from VAT and receipts from the EU budget. Expenditure growth (8.1%) was also significantly higher year on year, with all major expenditure categories contributing equally to growth. The state budget, the main part of the consolidated balance, will turn into surplus (EUR 193.4 million or 0.4% of GDP) by the end of the year according to the adopted revised budget. In the Stability Programme 2019, the surplus is also expected for the broader general government sector (EUR 462.4 million of 0.9% of GDP).