News

Slovenian Economic Mirror: At the beginning of the year, favourable domestic economic conditions and growth in revenue and household consumption; further moderation of growth in the international environment

Economic conditions were favourable at the beginning of the year. Confidence in the economy has remained almost unchanged since mid-2018, except in manufacturing. In this sector, confidence deteriorated again due to lower export orders, while the moderation of growth in main trading partners in the euro area also had a negative impact on business expectations about future exports. Registered unemployment continues to decline while higher household disposable income as a consequence of growth in wages and social transfers has a favourable impact on private consumption.

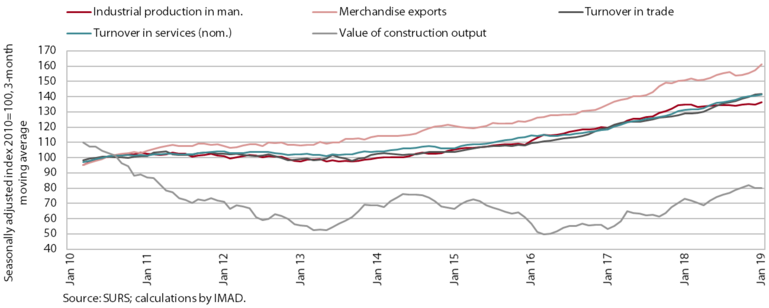

Favourable economic conditions continued at the beginning of the year. Activity growth in construction and manufacturing, while modest in the second half of 2018, strengthened significantly at the beginning of the year. Further growth was also recorded for turnover in market services and trade. The growth of goods exports also strengthened in January; the growth of services exports moderated but remained high. With regard to the expected developments in main trading partners in the euro area, the growth of exports is otherwise expected to moderate in the remainder of the year, given the steady decline in business and consumer confidence indicators in recent months. This was also one of the reasons for a considerable lowering of international institutions’ forecasts for euro area GDP for 2019.

Picture: Favourable developments in most sectors at the end of 2018 and at the beginning of 2019

Confidence in the Slovenian economy has remained almost unchanged since the middle of last year. At the beginning of the year, confidence increased only in retail trade, with sales expectations also improving amid higher sales, while consumer confidence and confidence in other sectors remained basically unchanged. The exception was manufacturing, where confidence fell again due to lower export orders, with the slowdown of growth in foreign demand also deteriorating business expectations regarding future exports. Specifically, global growth continues to moderate, especially in manufacturing and trade, which is also evident from the dynamics of the economic sentiment indicator (ESI), which declined again in all our main trading partners in the first quarter of 2019. The main reasons for lower expectations remain uncertainty about trade disputes and the UK’s withdrawal from the EU and more and more apparent signs of a moderation in China's economy.

Economic growth was also reflected on the labour market, where rising demand for labour contributed to high employment and a further decline in registered unemployment. The ILO unemployment rate came close to the pre-crisis level in the last quarter of 2018 and register data indicate a continuation of the positive labour market trend at the beginning of the 2019. In the first three months of the year, the number of registered unemployed dropped further and the number of employed remained high. The shortage of labour is reflected in a further increase in the employment of foreigners and upward pressure on wages. January’s year-on-year wage growth was besides by labour shortages also affected by a rise in the minimum wage and the increase in general government wages agreed at the end of 2018.

Stronger wage growth, alongside growth in social transfers, is increasing disposable income, which – amid relatively high consumer confidence – has a favourable impact on household spending. With more money available, also on account of higher consumer loans, households are mainly increasing spending on durable goods (passenger cars, furniture and household appliances) and tourist services at home and abroad. Growth in household consumption is thus affecting price rises in both goods and services. Year-on-year inflation therefore rose somewhat in March but remained relatively low.

The surplus of the current account of the balance of payments remains high. The strengthening of the positive current account balance in the twelve months to January was primarily a consequence of a higher surplus of trade in services, particularly trade in transport services and net inflows from travel, and a lower deficit in primary income related to lower costs of external debt servicing and higher net inflows of labour income. On the other hand, the surplus of trade in goods narrowed somewhat year on year with the moderation of exports of most key manufactured goods, especially vehicles (due to the petering out of a one-off factor), and a concurrent significant increase in growth of consumer goods imports.