News

Slovenian Economic Mirror 6/2021: The outlook for economic growth remains favourable, with most short-term indicators pointing to a high year-on-year growth

Economic activity in the international environment strengthened in the second quarter. After contracting in the first quarter, economic activity in the euro area recovered significantly in the second quarter, according to available economic indicators. In Slovenia, most short-term indicators point to a relatively high year-on-year growth and the outlook for economic growth remains favourable. The export-oriented part of the economy was less affected by the epidemic, and the volume of trade in goods and manufacturing production in May were also well above comparable levels before the outbreak of the epidemic. Confidence in manufacturing and construction remained high compared to a year ago. Preliminary data on turnover in trade and service activities for May and data on sales according to data on the fiscal verification of invoices for June also point to growth. The situation on the labour market is much better than last year, with the number of unemployed and employed people almost the same as before the crisis. In addition to seasonal influences, which were not significantly different from those in the pre-epidemic period, the decline can also be attributed to the gradual relaxation of containment measures and the economic recovery. Consumer price growth slowed slightly to 1.4% in June and continues to be driven mainly by higher energy prices. In June, the prices of food and services remained lower year-on-year, although they gradually approached year-earlier levels. The growth in industrial producer prices intensifies with the growth of commodity prices. The overall deficit of the consolidated balance of public finances amounted to EUR 1,266 million in the first five months and was slightly lower than a year ago.

Economic activity in the international environment strengthened in the second quarter. After contracting in the first quarter, economic activity in the euro area recovered significantly in the second quarter, according to available economic indicators. The composite Purchasing Managers' Index (PMI) showed a marked upturn in the services sector in May and June and a continued favourable trend in manufacturing. Economic sentiment also improved significantly across all sectors in June. International institutions expect growth to pick up further in the second half of the year due to progress in vaccination; 4.6% and 4.8% growth is forecast, with similar growth next year. Despite disruptions in global supply chains, growth of global trade in goods continued and is expected to continue in the coming months.

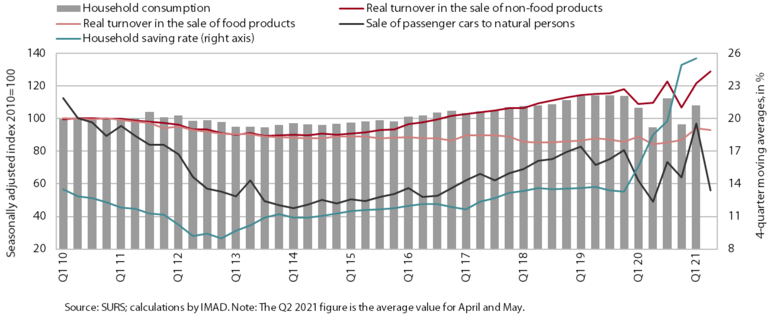

In Slovenia, the outlook for economic growth remains favourable, with most short-term indicators pointing to a relatively high year-on-year growth. Data on the export-oriented part of the economy, which was less affected by the epidemic, show that Slovenia's export market share in the EU market continued to strengthen in the first quarter of this year. With a monthly decline, the volumes of trade in goods and manufacturing production in May were still well above the comparable pre-epidemic levels. Export expectations improved again in June, and the continued favourable trends in the export-oriented part of the economy can also be seen in the volume of freight traffic on Slovenian motorways and in electricity consumption. Both were higher year-on-year, with the former already surpassing the level of the same period in 2019 and the latter narrowing its gap as tourism recovered. Confidence in manufacturing and construction remained high compared to a year ago. Preliminary data on turnover in trade and service activities for May and data on sales according to data on the fiscal verification of invoices for June also point to growth. This is due to the easing of measures in these sectors, which has also led to an improvement in confidence indicators in trade and service activities. Consumer confidence is still low, but has been improving in recent months. All this, together with better conditions on the labour market, also points to higher private consumption. Households held back on spending over the past year, partly because of uncertainty. With a relatively high level of disposable income, the volume of household deposits therefore rose sharply to almost EUR 24 billion in May.

Figure 1: As measures ease, household consumption gradually recovers.

The situation on the labour market is much better than last year, with the number of unemployed and employed people almost back to pre-crisis levels. In addition to seasonal influences, which were not significantly different from those in the pre-epidemic period, the decline can also be attributed to the gradual relaxation of containment measures and the economic recovery. At the end of June, 71,094 people were unemployed, which is a fifth less than a year ago and similar to the end of June 2019. The largest year-on-year decline was recorded in the sectors most affected by the containment measures, namely accommodation and food service activities and administrative and support service activities, while employment increased the most in human health and social work activities. After a strong year-on-year increase in average wages in previous months, growth remained moderate in April. It was lower in the private sector and relatively high in the public sector despite the high base last year.

Consumer price growth slowed slightly, down to 1.4% in June from 2.1% in May, but industrial producer price growth is being boosted by the rise in commodity prices. In June, the prices of food and services remained lower year-on-year, although they gradually approached year-earlier levels. Year-on-year price increases for semi-durable goods were broadly unchanged, while price increases for durable goods nearly halved compared with the previous month. The contribution from energy prices, which, with a high year-on-year increase in the prices of petroleum products, contribute the most to current inflation, decreased significantly in June due to the base effect. Year-on-year growth in Slovenian industrial producer prices continued to strengthen in May, reaching 3.5%, the highest level since 2011. Higher commodity prices contributed the most to the growth, with metal production prices rising 15% year-on-year.

The overall deficit of the consolidated balance of public finances amounted to EUR 1,266 million in the first five months and was slightly lower than a year ago. Turnover in the first five months was a fifth higher than a year ago, with tax revenues rising in particular as containment measures gradually eased. On the expenditure side, the largest increase was recorded in wages and current transfers, mainly due to payments for the implementation of measures to contain the second wave of the epidemic. Slovenia’s net budgetary position against the EU budget was positive in the first five months.