News

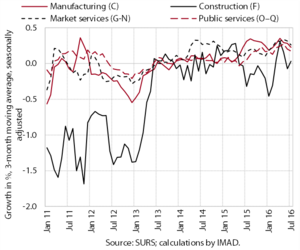

Manufacturing industries have exceeded the pre-crisis production level

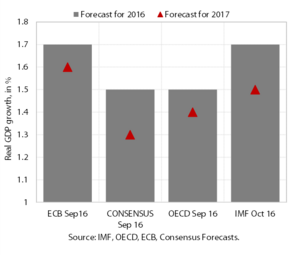

The prospects for economic growth in the euro area remain favourable; the risks are on the downside and arise mainly from outside the euro area. In July activity in retail trade and construction climbed to the highest level this year while activity in manufacturing remained unchanged. Confidence indicators also indicate further growth in economic activity in coming months. Autumn forecasts by international institutions for GDP growth in the euro area have not changed significantly, predicting growth rates of between -1.5% and 1.7% for 2015 and between 1.3% and1.6% for 2016. According to the OECD, the ECB and the IMF, the key risks to growth are weak foreign demand and the potential negative implications of the referendum decision in the UK. Thus far the UK’s vote to leave the EU has not significantly affected confidence or economic activity in the euro area.

Most short-term indicators of economic activity in Slovenia increased further at the beginning of the third quarter. Growth in merchandise exports continued, as did growth in manufacturing output, which exceeded the 2008 figures for the first time. Turnover in market services remained high. Improved labour market conditions and growth in private consumption were reflected in further growth in some segments of trade. Turnover also increased further in tourism-related services, which was also attributable to higher spending of foreign tourists in Slovenia. In recent months activity has also been picking up in construction, and growth prospects for this sector improved further. Confidence in the economy and among consumers remains high and suggests a continuation of favourable trends.

Labour market conditions remain favourable. In July the number of employed rose further, particularly in manufacturing, professional, scientific and technical activities, and accommodation and food service activities. Expectations about employment also remain high. Registered unemployment continued to decline, 95,125 persons being registered as unemployed at the end of September, 9.2% less than one year before. Average gross earnings have not changed significantly in the last few months and remain at the same level as at the end of 2015.

Consumer prices remain at a similar level to one year ago. In September, service and food prices were up year-on-year while prices of durable and semi-durable goods were down. Price movements were affected by year-on-year declines in energy prices, but their negative contribution has decreased in the last few months.

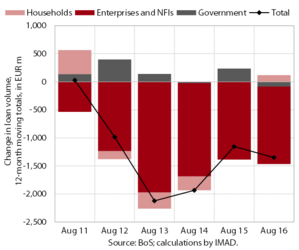

Lending activity remains modest amid further deleveraging of the corporate sector; the maturity of deposits is shortening. The volume of household housing and consumer loans is rising while the volume of corporate and NFI loans continues to fall. The share of non-performing claims is declining as well: at the end of July they accounted for 7.3% of all bank claims. The maturity structure of deposits continues to deteriorate, since mainly overnight deposits are increasing. This could hamper the rebound in longer-term bank lending, according to our estimate. Among bank sources of finance, deposits of domestic non-banking sectors play an increasingly important role, while the volume of inter-bank financing and liabilities to the euro-system contracts.

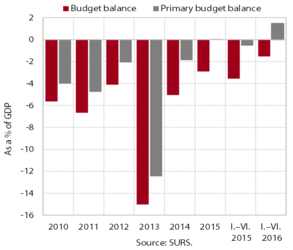

The favourable economic situation and labour market conditions are increasing tax revenues and social security contributions, but as receipts from the EU budget declined by around 40% during the transition to the new financial perspective, total general government revenue did not change significantly this year. General government expenditure was lower, owing mainly to approximately half lower investment expenditure and, partly, lower payments into the EU budget, amid a significant increase in expenditure on wages and social transfers. Specifically, after the partial removal of austerity measures, some transfers to individuals and households increased considerably despite the improvement in labour market conditions. The general government deficit (on a cash basis) was thus EUR 235 million lower year-on-year in the first seven months.