Charts of the Week

Current economic trends from 9 to 13 November 2020: registered unemployment, electricity consumption, traffic of electronically tolled vehicles, exports and imports of goods and other charts

After a marked decline in September, the number of unemployed persons remained practically unchanged at the beginning of November, despite the restrictions on business operations imposed in mid-October due to the deteriorating epidemiological picture. Nor has there been any significant change in electricity consumption and freight transport on Slovenian motorways in recent weeks, which suggests that the economic impact of the renewed spread of the epidemic may be less intense than in the spring. After the revival of most export-oriented parts of the economy during the summer months, in September growth in external trade in goods also slowed in our main trading partners amid a rise in the number of infections and a consequent tightening of measures, while the recovery in manufacturing came to a halt. By contrast, activity in construction continued to strengthen in September.

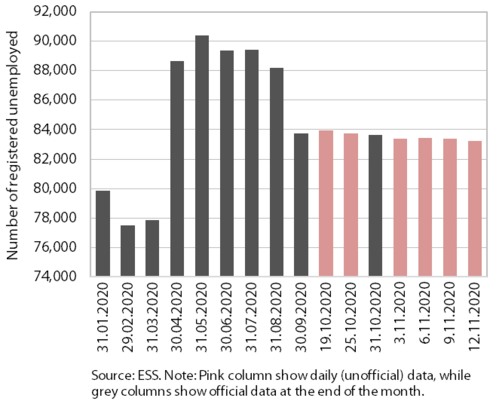

Registered unemployment, November 2020

At the beginning of November, the number of registered unemployed remained at almost the same level as in the previous two months, despite the renewed restrictions on operations. After strong growth in the first wave of the epidemic, the number of registered unemployed persons has been falling gradually since mid-year following the adoption of intervention job retention measures and the lifting of restrictions. Since mid-October, when the second wave of the epidemic was declared, the number has remained more or less unchanged. This was, amid the adaptation of businesses and consumers to changes in the modes of operation, largely due to the extension of intervention measures. According to ESS unofficial (daily) data, 83,233 persons were unemployed on 12 November, which is 0.5% less than at the end of October and around 15% more than in the same period last year.

Electricity consumption, November 2020

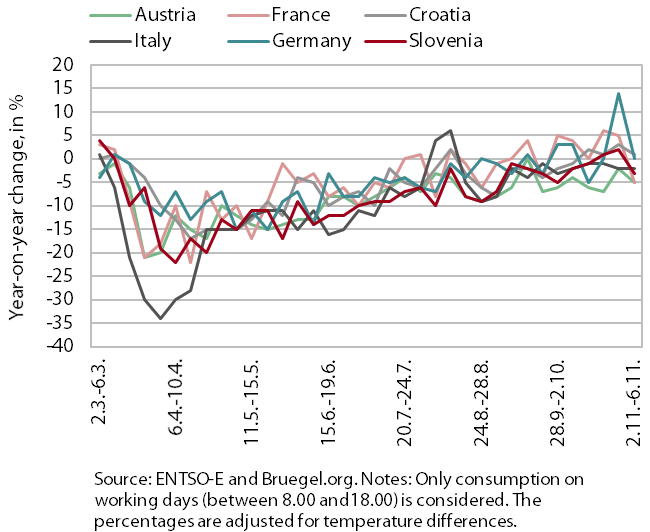

The year-on-year decline in weekly electricity consumption increased somewhat at the beginning of November, but it remained significantly smaller than at the beginning of the spring wave of the epidemic. In the first week of November, weekly electricity consumption was 3% lower year on year, while at the beginning of April, the decline was more than 20%. A smaller decline in consumption than in the spring was also seen in Slovenia's main trading partners. At the beginning of November, the largest decline in weekly electricity consumption was recorded in Austria and France (5%), followed by Italy (around 2%). Consumption in Germany and Croatia was roughly the same as last year.

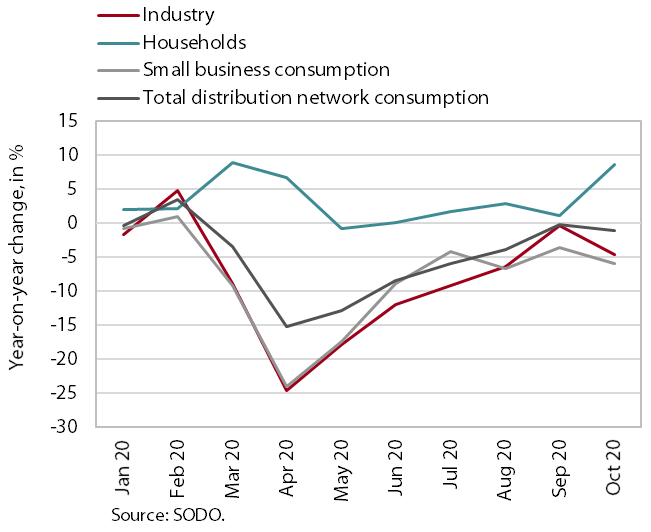

Electricity consumption by consumption group, October 2020

After the renewed declaration of the epidemic, the year-on-year fall in electricity consumption at the end of October was smaller than at the beginning of the first wave of the epidemic in March. After falling sharply in April, industrial electricity consumption almost reached last year’s level in September. In October, the decline increased again (4.6%) but was smaller than in March (8.8%). Small business consumption also declined less year on year (6%) than in March (9.1%). Household consumption increased by roughly the same percentage as in March (just over 8% year on year), as people spent more time at home due to the epidemic.

Traffic of electronically tolled vehicles on Slovenian motorways, November 2020

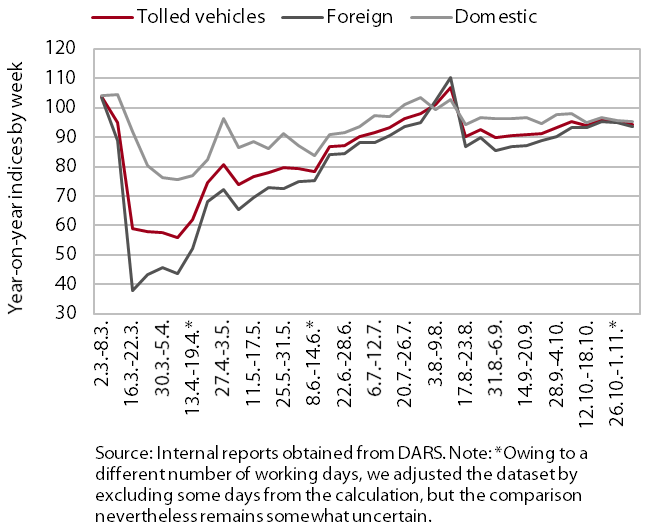

At the beginning of November, freight traffic on Slovenian motorways remained similar to that in October and somewhat smaller than before the first wave of the epidemic. After a sharp fall following the declaration of the epidemic in March, it increased more markedly from mid-June to mid-August. Then it fell again and remained around 10% below last year’s level until the beginning of October, when it increased again slightly. In the week between 2 October and 8 November, it lagged 6% behind last year's level, similarly for foreign and domestic hauliers.

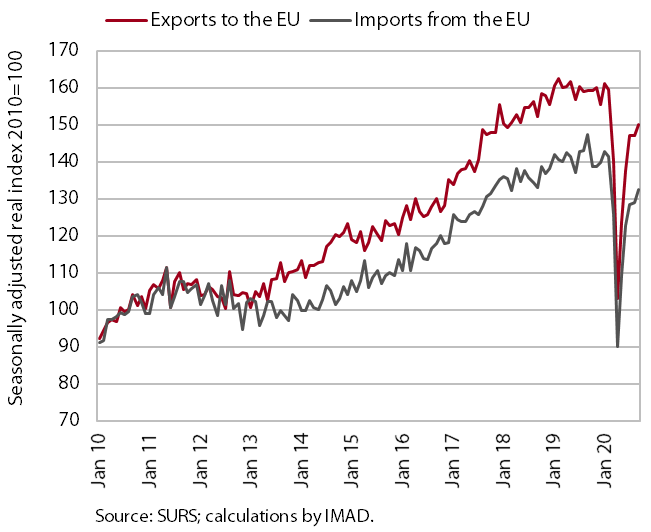

Exports and imports of goods, September 2020

Trade in goods increased noticeably in the third quarter after a decline in the second, but it remained lower year on year. With a rebound in activity in main trading partners, exports to EU countries picked up in particular, though they were still almost 6% lower year on year. Exports recovered in the majority of main activities, the most in the group of motor vehicles (around one quarter of total exports), where they had also decreased the most in the period of containment measures. Exports of motor vehicles increased in particular, more than exports of motor vehicle parts and accessories. Exports of electrical machinery and equipment also rose markedly, while the recovery of some other main manufactured goods was more modest (metals and metal products). In the third quarter, imports also increased considerably, particularly of intermediate goods (excluding oil and oil products). Companies are more optimistic regarding future foreign demand than during the first wave of the epidemic in the spring. This indicates that the renewed containment measures could have a smaller impact on goods trade than those in the spring, as the measures in Slovenia and its main trading partners are for now somewhat less severe and companies more adapted to the situation.

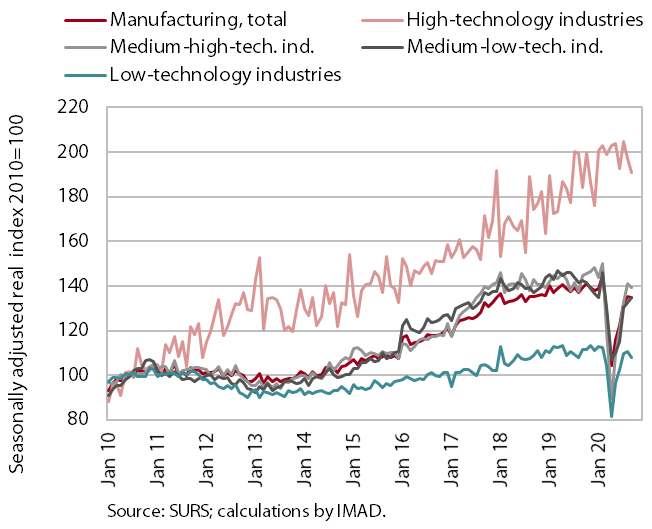

Production volume in manufacturing, September 2020

Manufacturing production increased strongly in the third quarter, but in September growth came to a halt in most industries. High-technology production, which had been the least affected during the first wave of the epidemic, decreased somewhat in the last months but remained higher than last year. Last year’s levels were also exceeded by the manufacture of machinery and equipment and some low-technology industries, where production had contracted less during the first wave of the epidemic (the food- and wood-processing industries). In the third quarter, the majority of other industries were still lagging behind last year's levels despite a significant increase in production. The decline remained largest in the metal and leather industries, while decreasing notably in motor vehicle and electrical equipment manufacturing. At the beginning of the last quarter, i.e. already before the tightening of measures in most EU countries, the improvement in business expectations about future demand and production slowed amid uncertain economic conditions and insufficient demand.

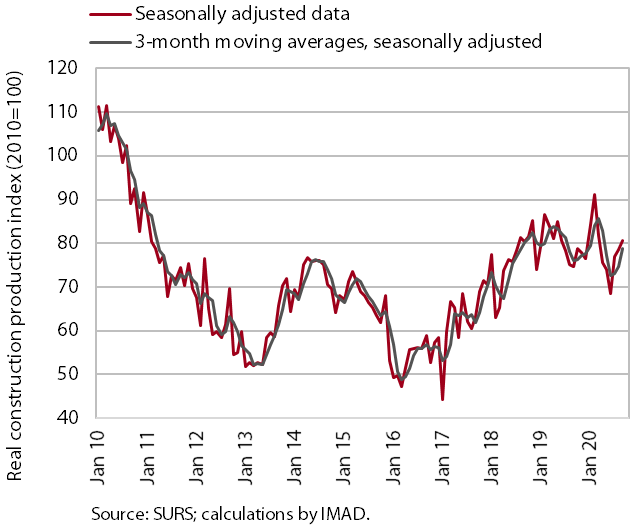

The value of construction put in place, September 2020

After a decline in the spring months, construction activity strengthened in the third quarter. The value of construction output increased in all three months of the third quarter. In September, it was 11.6% lower than in February, the last month before the outbreak of the epidemic. Compared with 2018 and 2019, in the last months, construction activity was significantly lower in non-residential buildings, at more or less the same level in civil-engineering works and higher in residential buildings (where data for the last months are less reliable).

Short-term prospects remain favourable for civil-engineering works, while they look worse for the construction of buildings, particularly non-residential buildings. The stock of contracts in the construction of civil-engineering works has increased by almost 50% in the last year, while in the construction of non-residential buildings it has declined by 10%. In the second quarter, the total floor area of buildings planned by issued building permits was considerably lower than in the second quarter last year, while in the third quarter, the lag behind last year’s level decreased.

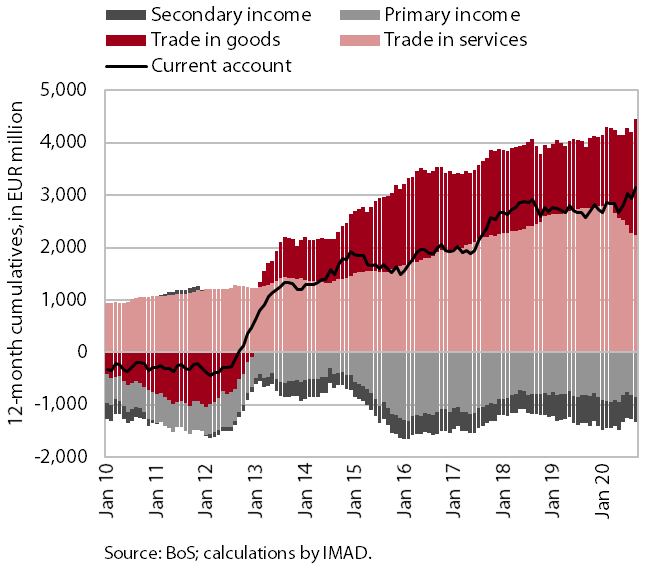

The balance of payments, September 2020

In the third quarter, the movements in the current account of the balance of payments mainly reflected a wider surplus in goods and a much lower volume of trade in travel services due to the measures to contain the spread of the epidemic. The current account surplus, the highest to date, totalled EUR 3.1 billion in the last 12-month period (6.9% of estimated GDP). Amid the improved terms of trade, the higher surplus was mainly attributable to a higher surplus in trade, as the year-on-year fall in real imports was deeper than in exports. The surplus also strengthened due to the net outflows of secondary income, which declined due to lower VAT- and GNI-based contributions to the EU budget and smaller payments of taxes and contributions abroad. The surplus in services declined further mostly due to a fall in trade in travel services. Net outflows of primary income were higher year on year due to a smaller surplus in labour income, as revenue of daily migrants working abroad declined more than revenue of foreigners working in Slovenia. Higher net outflows were also recorded for dividends from investment in securities.