Charts of the Week

Current economic trends from 9 to 12 February 2021: production volume in manufacturing, exports and imports of goods, electricity consumption, traffic of electronically tolled vehicles, fiscal verification of invoices and registered unemployment

In the last quarter of last year, activity in the export-oriented part of the economy increased further, while manufacturing production and goods exports reached pre-crisis levels from the last quarter of 2019. At the end of last year, the recovery of goods imports came to a halt, particularly due to lower household consumption. The continuation of relatively favourable movements of the export-oriented part of the economy at the beginning of this year is indicated by data on electricity consumption and freight traffic on Slovenian motorways, which were at roughly the same levels year on year at the beginning of February. With the opening of some shops and services, the year-on-year fall in turnover according to the fiscal verification of invoices also declined at the end of January and the beginning of February. After a seasonal increase at the end of last and the beginning of this year, the number of unemployed persons declined seasonally in the first half of February.

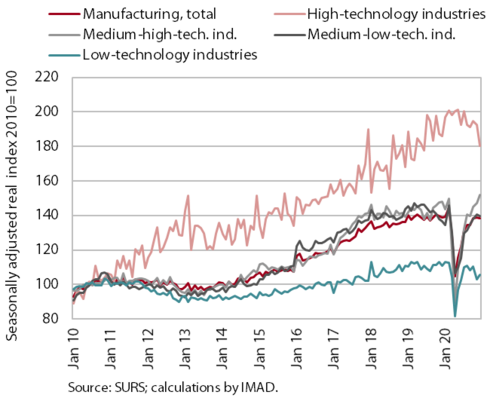

Production volume in manufacturing, December 2020

With a further increase in the last quarter of 2020, manufacturing production recovered to pre-crisis levels. In the last quarter, the recovery of production otherwise came to a halt in high-technology industries (which were the least affected during the first wave of the epidemic) and low-technology industries, while strengthening further in medium-technology industries. The latter thus exceeded the levels from the same period of 2019. Despite a sharp increase in the second half of the year, in 2020 production in medium-high and medium-low industries was lower year on year in all sectors, particularly in the manufacture of motor vehicles and the metal industry. Lower production was also recorded in low-technology industries, with the exception of the wood-processing industry. High-technology industries remained the only industries that increased production year on year in 2020 (despite more modest year-on-year results of the pharmaceutical industry in the second half of the year).

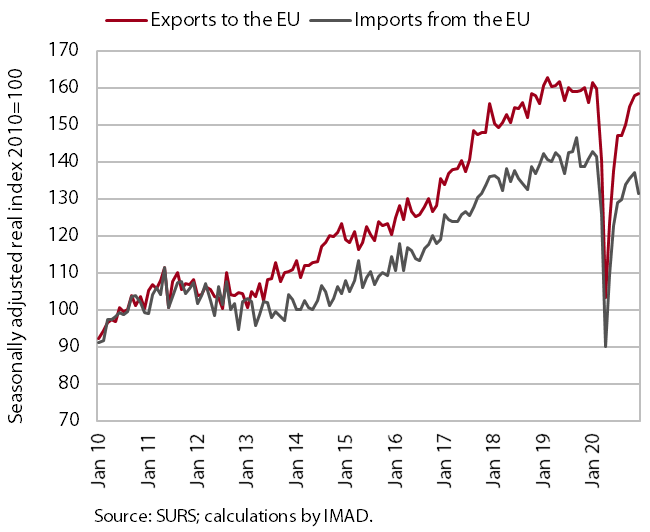

Exports and imports of goods, December 2020

The recovery of goods exports continued in the last quarter of 2020, while the recovery of imports came to a halt. Export activity was not significantly affected by the resurgence of the epidemic and the adoption of containment measures in the last quarter. After a pronounced decline in the spring, exports to EU countries recovered to pre-crisis levels by the end of 2020. A stronger recovery was recorded for most main product groups, particularly goods for intermediate consumption. Exports were 7.7% lower on average in 2020. In the last quarter, the recovery of imports came to a halt, which is mainly related to a fall in private consumption in Slovenia due to containment measures. Imports from EU countries thus fell by 11.7% in the year as a whole. In January, export expectations improved somewhat further, pointing to a continuation of export recovery at the beginning of this year.

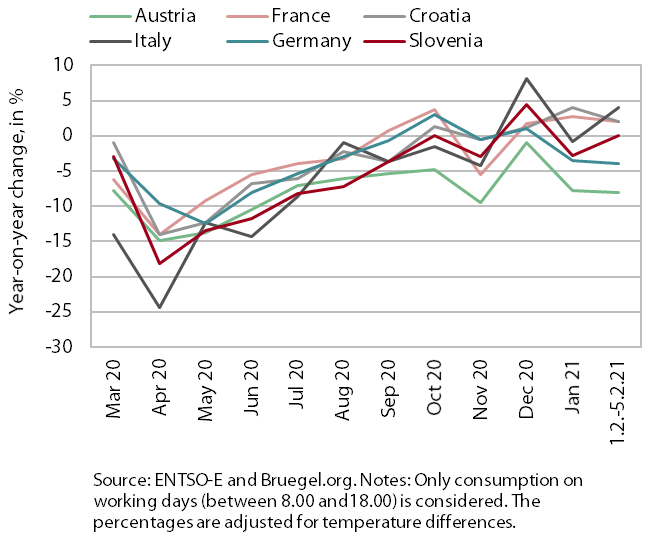

Electricity consumption, February 2021

Electricity consumption in Slovenia in the first week of February was the same as in the same period of last year. Among Slovenia’s main trading partners, the largest year-on-year decline in consumption was recorded in Austria (8%), as during the entire period of the second wave of the epidemic. Germany also had lower consumption than last year (4%). Other trading partners recorded higher consumption than last year, France and Croatia by 2% and Italy by 4%.

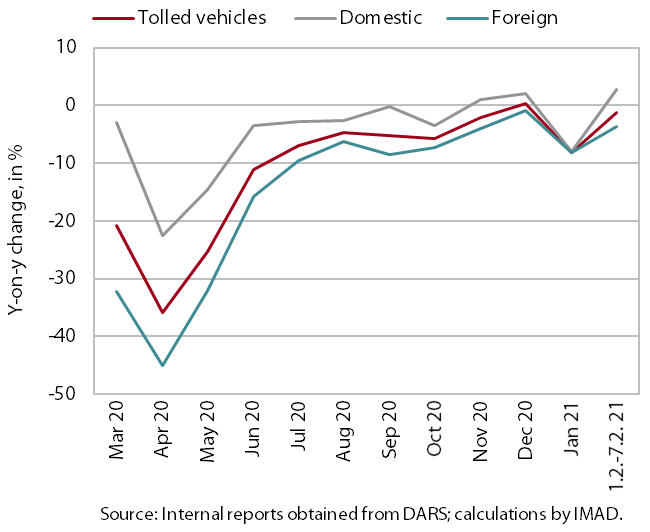

Traffic of electronically tolled vehicles on Slovenian motorways, February 2021

Freight traffic on Slovenian motorways in the first week of February was almost the same as in the first week of February 2020. In the week between 1 and 7 February, it was 1% lower year on year. Domestic vehicle traffic was up 3%, while foreign vehicle traffic was down 4%. The narrowing of the year-on-year gap at the beginning of February was partly related to a different day of the public holiday and hence a different distribution of traffic around it. Part of the decline in foreign vehicles can again also be attributed to poor weather conditions in some neighbouring countries, while the increased traffic of domestic vehicles is partly related to the announced re-opening of shops. A smaller year-on-year decline in freight traffic during the second wave of the epidemic is mainly a consequence of the recovery of industry. The negative impact of measures in services on freight traffic has been insignificant.

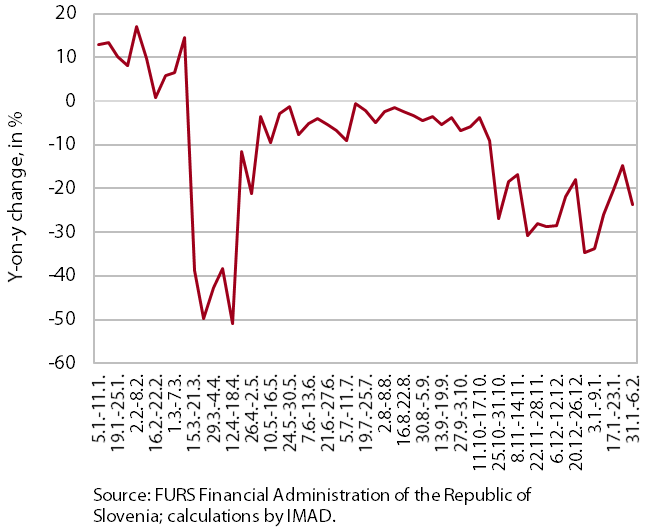

Fiscal verification of invoices, February 2021

According to data on the fiscal verification of invoices, the year-on-year fall in turnover decreased at the end of January and the beginning of February. This was mainly due to the partial opening of some shops and services and hence a decline particularly in trade. With a renewed closure, the year-on-year lag in turnover remained largest in accommodation and travel agency activities.

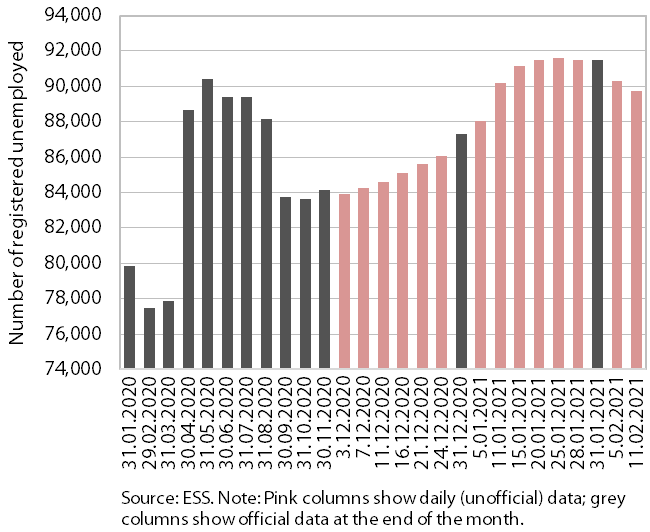

Registered unemployment, February 2021

After a seasonal increase in December and January, the number of registered unemployed persons recorded a slight seasonal decline in the first half of February. The adoption of intervention measures to preserve jobs during the first wave and the subsequent easing of restrictions on businesses stemmed the high growth of unemployment seen in March and April. This was followed by a gradual decline from July to September. Until the end of November, the number of unemployed persons remained roughly unchanged, before rising moderately in December and January. With intervention measures still in place, this growth did not deviate significantly from seasonal increases at the end and the beginning of previous years and came to a halt towards the end of January. In February, a seasonal fall in unemployment can already be seen. According to ESS unofficial (daily) data, 89,761 persons were unemployed on 11 February, which is 1.9% less than at the end of January and around 16% more than a year earlier.