Charts of the Week

Current economic trends from 6 to 9 April 2021: fiscal verification of invoices, traffic of electronically tolled vehicles, electricity consumption, registered unemployment and other charts

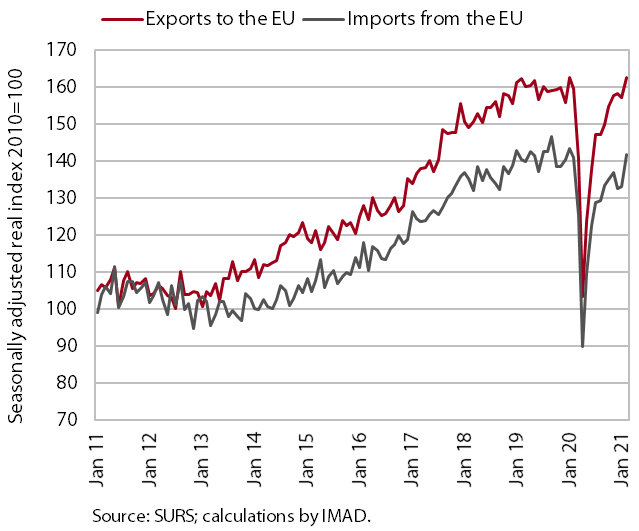

The relatively favourable developments in the export-oriented part of the economy, which had reached pre-crisis levels at the end of last year, continued at the beginning of the year. After the increase in January, manufacturing output remained at a similar level in February; goods exports to EU countries rose.

According to data on fiscal verification of invoices, turnover was significantly higher year on year at the end of March and the beginning of April, mainly due to the base effect, as in the same period of last year all non-essential shops had been closed. Compared with the same period of the pre-crisis year 2019, it was around 3% higher, which is also related to increased sales before the re-closure of some shops and the distribution of Easter holidays. Freight traffic on Slovenian motorways and electricity consumption were also significantly higher year on year at the beginning of April due to the base effect, but lower than in the same period of the pre-crisis year. The lag in traffic was also a consequence of the distribution of Easter holidays, while the decline in electricity consumption reflected the stringent containment measures. The decline in the number of unemployed continued at the beginning of April.

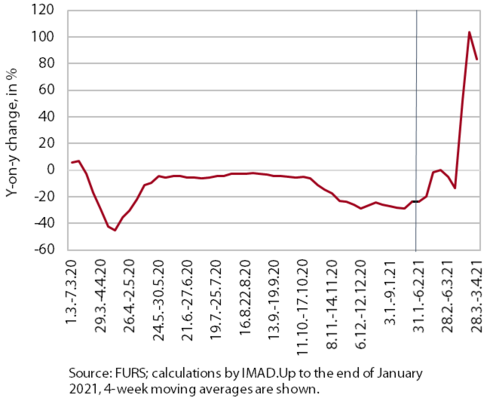

Fiscal verification of invoices, April 2021

According to data on fiscal verification of invoices, turnover at the end of March and the beginning of April was significantly higher year on year due to the base effect; compared with the same period of 2019, it was around 3% higher. Year-on-year growth in turnover strengthened further in the fourth week of March. At the transition to April, it fell due to the new lockdown, but remained high. Strong year-on-year growth in sales in the days until the end of March was mainly a consequence of high growth in turnover in trade, as last year all non-essential shops had been closed in this period. Growth was also partly related to increased sales before the re-closure of some shops and the distribution of Easter holidays, because of which turnover in trade also remained relatively high compared with the same period of the pre-crisis year 2019. With bar terraces and gardens also opening in the Primorsko-notranjska region, year-on-year turnover growth in food and beverage serving activities rose further in the fourth week of March before falling due to the re-closure at the turn of the month.

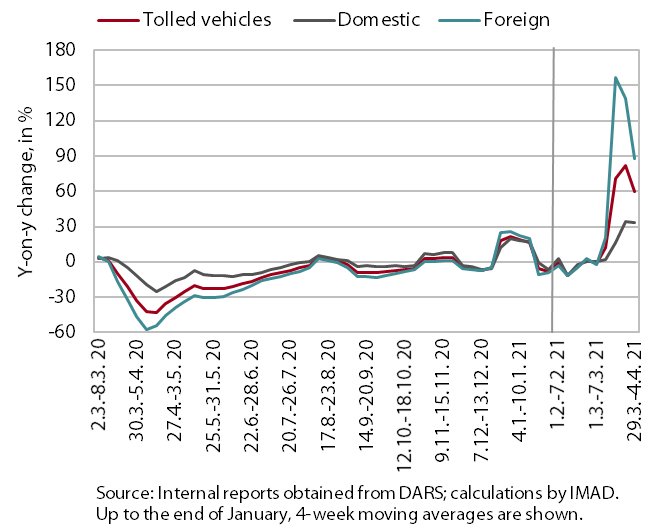

Traffic of electronically tolled vehicles on Slovenian motorways, April 2021

Freight traffic on Slovenian motorways in the first week of April was 60% higher than in the same period of last year but 8% lower than in the same period of 2019. Between 29 March and 4 April, domestic vehicle traffic was 34% higher and foreign vehicle traffic 88% higher year on year. This strong growth was mainly a consequence of the base effect, given that in the same period of last year, traffic had been highly limited due to the stringent containment measures during the first wave of the epidemic. In the first week of April, the volume of freight traffic was also not particularly high due to Easter holidays and restrictions on traffic during this period. Amid a different distribution of holidays, it lagged behind that in the same period of the pre-crisis year 2019 (in domestic vehicles, it was 2% higher, in foreign vehicles 14% lower).

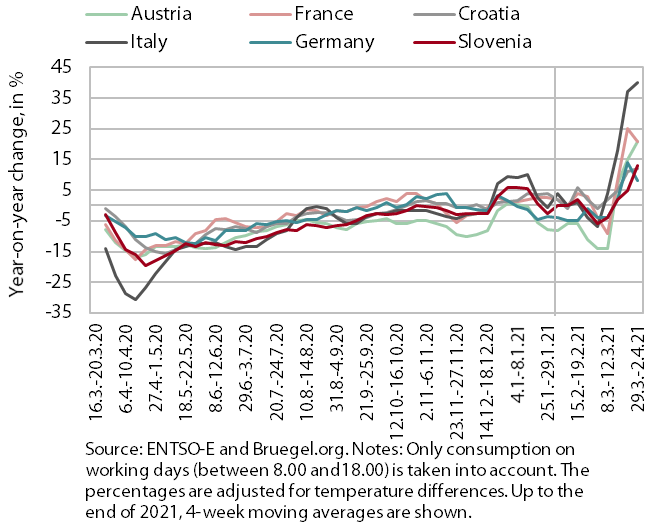

Electricity consumption, April 2021

In the week between 29 March and 2 April, electricity consumption was 13% higher than in same week of 2020 but 6% lower compared with the same week of the pre-crisis year 2019. The main reason for the significant year-on-year rise in consumption was the base effect and for the lower consumption than in the the same week of 2019 the new lockdown, which started on 1 April. Particularly due to the base effect, year-on-year higher consumption was also recorded in our main trading partners, from 12% in Croatia to 40% in Italy. Relative to the comparable week of 2019, consumption in Italy and Germany was 6% lower, in Austria and France roughly the same, and in Croatia 2% higher.

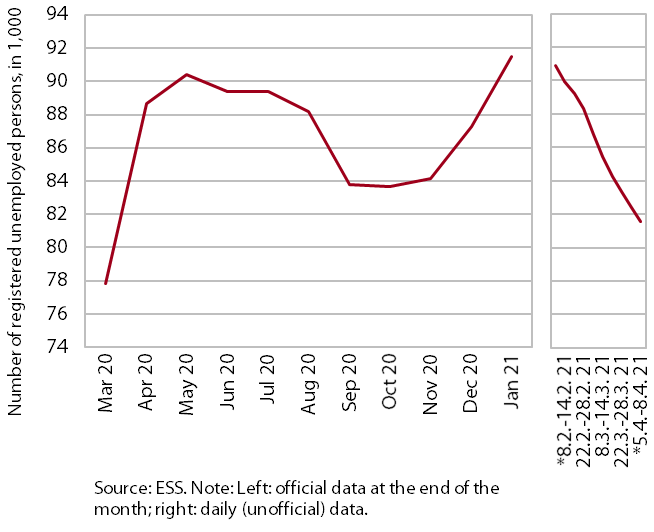

Registered unemployment, April 2021

The number of registered unemployed persons fell further at the beginning of April. Following the increases in the number of unemployed in December and January, which, due to the retention of intervention measures, did not differ much from seasonal increases in the same period of previous years, the number of unemployed dropped seasonally adjusted in February. As a result of seasonal factors and the easing of containment measures, the decline in the number of unemployed strengthened somewhat further in March and also continued at the beginning of April. On 8 April, 81,424 persons were unemployed according to ESS unofficial (daily) data, which is 1.5% less than at the end of March and around 8% less than in the same period last year.

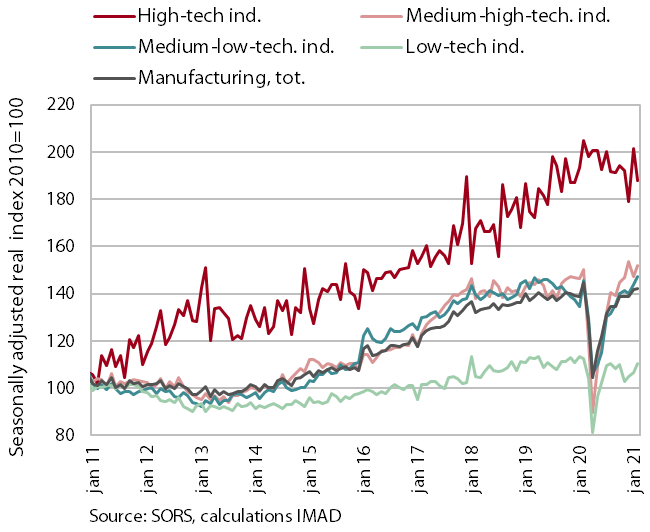

Production volume in manufacturing, February 2021

In February, manufacturing production remained similar month on month. Production in medium-high-technology industries strengthened after a fall in January. Medium-low- and low-technology industries recorded further growth, while production in high-technology industries declined. As in the previous month, manufacturing production was down year on year. Amid last year's high base, this was largely a consequence of a fall in high- and low-technology industries. The worse performance in high-technology industries was a consequence of a year-on-year decline in pharmaceutical production; in low-technology industries the fall was more broad-based. Production in medium-low- and medium-high-technology industries stagnated year on year. Among the latter, the largest negative contribution was made by the car industry.

Goods trade, February 2021

After the recovery of goods trade came to a halt at the turn of the year, February saw more favourable developments. Real goods exports to EU countries rose and exceeded pre-crisis levels. Exports recovered in in the majority of main activities; particularly the movements of exports of intermediate goods and some high-technology consumer goods remained favourable. In March, export expectations improved noticeably, companies being more optimistic regarding future foreign demand than before the beginning of the epidemic. Goods imports recovered too, underpinned mainly by imports of intermediate goods and activity of industrial sectors and, to a lesser extent, the movements of private consumption due to the relaxation of some containment measures.