Charts of the Week

Current economic trends from 6 to 10 December 2021: registered unemployment, electricity consumption by consumption group, traffic of electronically tolled vehicles on Slovenian motorways and other data

Activities related to international trade were already affected by supply chain disruptions in the third quarter, with growth slowing slightly year-on-year in October as well. These problems, particularly the semiconductor shortage, have a particular impact on the decline in activities related to the automotive industry. Labour market conditions remain favourable. In November, the number of unemployed was 1.9% lower than in the previous month and about a fifth lower year-on-year and almost a tenth lower than in November 2019. Given the high demand for labour, which is also reflected in the high vacancy rate, the proportion of unemployed people aged over 50 with low employment prospects is rising this year.

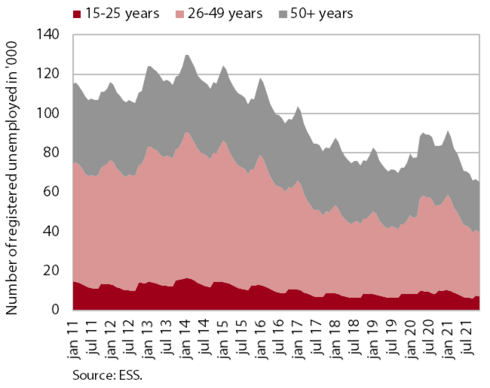

Registered unemployment, November 2021

According to the seasonally adjusted data, the decline in registered unemployment in November was higher than in the previous months, namely 2.4%. According to original data, 65,379 people were unemployed at the end of November, 1.9% fewer than at the end of October and 22.3% fewer than a year earlier. The number of unemployed persons was also lower (by 9.7%) than at the end of November 2019. In the first eleven months of this year, the inflow into unemployment was lower than in the same period of 2019. The outflow from unemployment has fallen in recent months, but remains higher than the inflow, so that the number of unemployed continues to fall. Given the high demand for labour, which is also reflected in the high vacancy rate, the proportion of unemployed people aged over 50 with low employment prospects is rising this year. In November, their share was 38.8%.

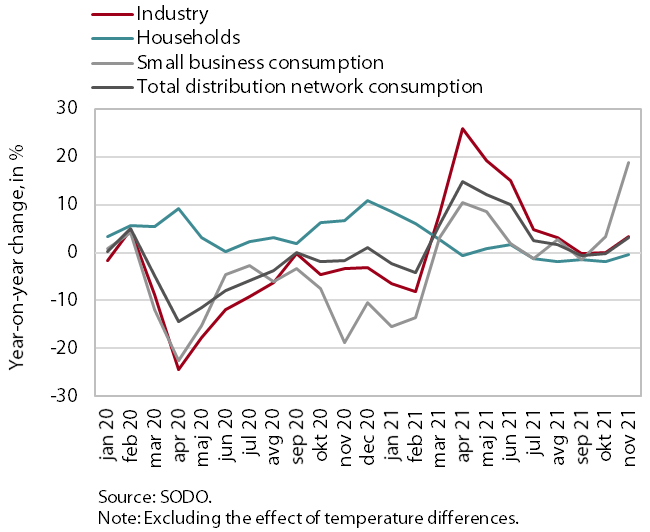

Electricity consumption by consumption group, November 2021

Year-on-year, industrial and small business electricity consumption were higher in November, while compared to the same period of 2019, industrial consumption remained about the same and small business consumption was lower. Compared to November last year, industrial electricity consumption increased by 3.4% and small business electricity consumption by 18.7%. The main reason for the high year-on-year growth in small business consumption was last year's low base, as containment measures were introduced last November during the second wave of the epidemic, restricting mainly trade and services activities. Household consumption in November was similar to the same period last year (lower by 0.5%), as household members spent more time at home - similar as last year - due to various epidemic-related reasons (illness, remote working, etc.). Compared to November 2019, industrial consumption remained about the same, while small business consumption, which has lagged behind comparable periods in 2019 since the start of the epidemic, was lower (by 2.6%). Compared to November 2019, household consumption increased by 6.2%.

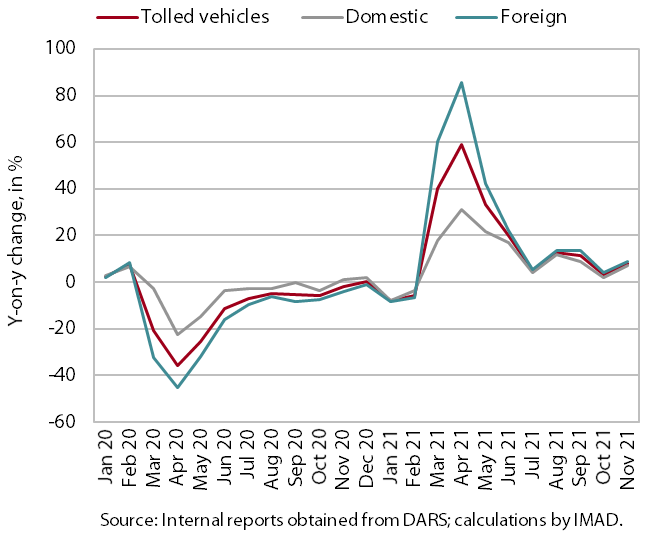

Traffic of electronically tolled vehicles on Slovenian motorways, November 2021

Freight traffic on Slovenian motorways increased by 8% year-on-year in November. The high year-on-year increase was due to lower traffic volumes in the second wave of the epidemic last year. Compared to November 2019, the volume of freight traffic was also significantly higher due to one more working day, but after adjusting the data for working days, it was only one percent higher. The share of foreign vehicle traffic on Slovenian motorways, which had fallen slightly year-on-year in November 2020, returned to its pre-epidemic level of 61% this year.

Trade in goods, October 2021

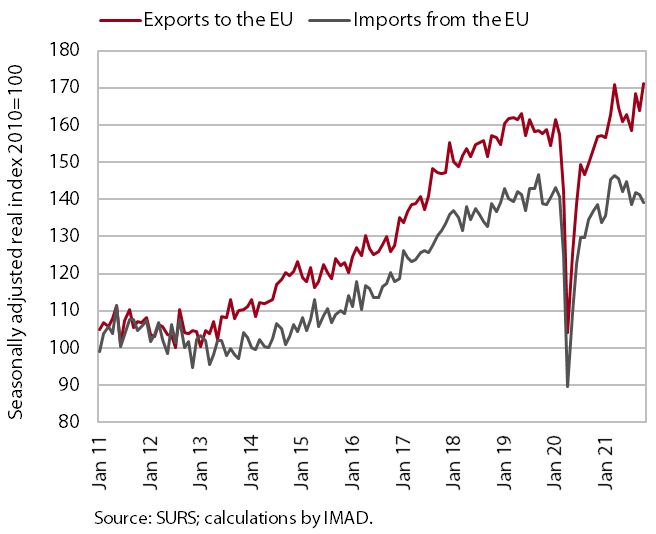

The increased uncertainty in the international environment in recent months has had an impact on export and import activity in Slovenia. Uncertainty related to high commodity prices and supply chain disruptions particularly affected the automotive and related industries in Slovenia and among its main trading partners. At the same time, there have been more marked monthly fluctuations in trade with other EU Member States in recent months, with exports rising slightly and imports falling. In our opinion, the fluctuations in exports are mainly related to the vehicles group, which is also the only one of the main product groups to lag behind the level of the same period in 2019. The stronger monthly fluctuations in imports have been largely related to the import of capital goods and some consumer goods (passenger cars, non-durable goods excluding medical and pharmaceutical products). Compared to the same period in 2019, trade in goods, especially with EU Member States, was slightly higher in October (higher exports, lower imports). Export expectations and new orders rose in November, well above the long-term average, and their fluctuations in recent months indicate increased uncertainty.

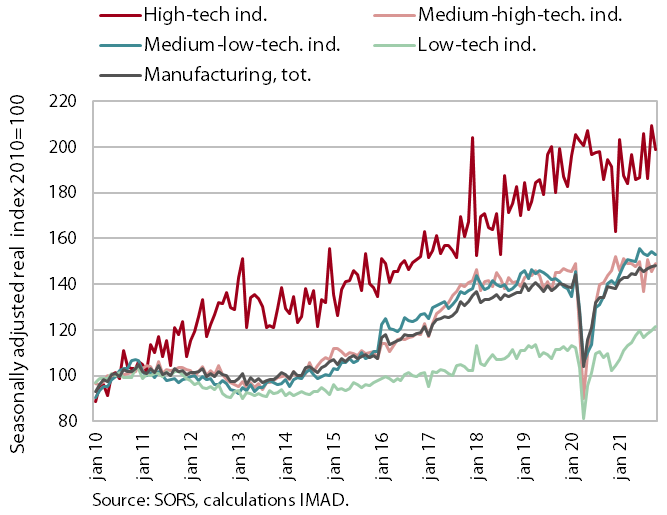

Production volume in manufacturing, October 2021

Manufacturing activities were already affected by supply chain disruptions in the third quarter, with growth slowing slightly year-on-year in October as well. Medium-low and low technology industries recorded relatively high year-on-year growth, but at a lower rate than in the previous month. Medium-high technology industries recorded modest year-on-year growth, while high-technology industries recorded a decline. The decline was even slightly higher than in the same period of 2019. Production in medium-technology industries was limited by supply disruptions, especially in the automotive industry, but also in the rubber and plastics industry and in the manufacture of electrical appliances. In high-technology industries, the year-on-year decline was mitigated by the production of electronic and optical products.