Charts of the Week

Current economic trends from 4 to 8 October 2021: fiscal verification of invoices, traffic of electronically tolled vehicles on Slovenian motorways, electricity consumption, registered unemployment and other

In September, high-frequency short-term indicators for several activities pointed to continued growth, although uncertainty remains high. According to data on fiscal verification of invoices, total turnover in the second half of September was higher than in the same period before the epidemic. Uncertainty related to the future development of the COVID-19 epidemic and the introduction of the recovered/vaccinated/tested rule led to a moderation in year-on-year growth. In September, the volume of freight traffic on Slovenian motorways remained comparable to the same period before the epidemic, while the growth of electricity consumption has slowed down in recent months. This is mainly due to the fact that industrial consumption remains below pre-epidemic levels due to material supply and production disruptions. In September, the number of unemployed continued to fall in the face of strong demand for labour. At the end of the month, 21.1% fewer people were unemployed than a year ago and 5.3% fewer than in the same period of 2019. Despite significant fluctuations in recent months, mainly due to disruptions in the vehicle exports due to disrupted supply of raw materials, trade with EU Member States remains high and well above pre-epidemic levels.

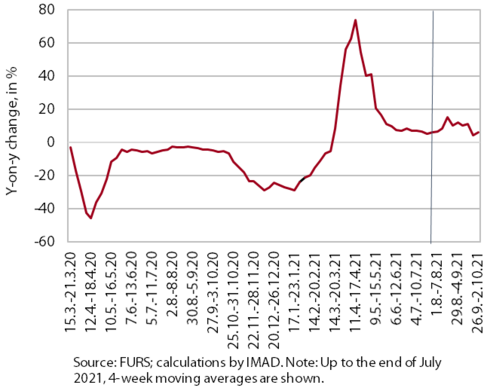

Fiscal verification of invoices, September 2021

According to data on fiscal verification of invoices, total turnover between 19 September and 2 October was 6% higher year-on-year and similar to that in the same period of 2019. Year-on-year growth has slowed sharply (from 11% and 6% respectively) compared to the growth in the previous two weeks, likely due in part to the introduction of the recovered/vaccinated/tested rule for users of most services and activities. Year-on-year growth in trade more than halved (to 4%), mainly due to a decline in retail trade, which accounts for almost half of total turnover. The introduction of the recovered/vaccinated/tested rule also contributed to lower turnover in some other activities such as accommodation, food and beverage service activities and sports activities, resulting in a significant decline in growth compared to the same period in 2019. Nevertheless, year-on-year turnover growth in these services remained high (around 20%), due to the increased number of foreign and domestic tourists and same-day visitors (also as a result of the low turnover or base last year) and the continued redemption of vouchers.

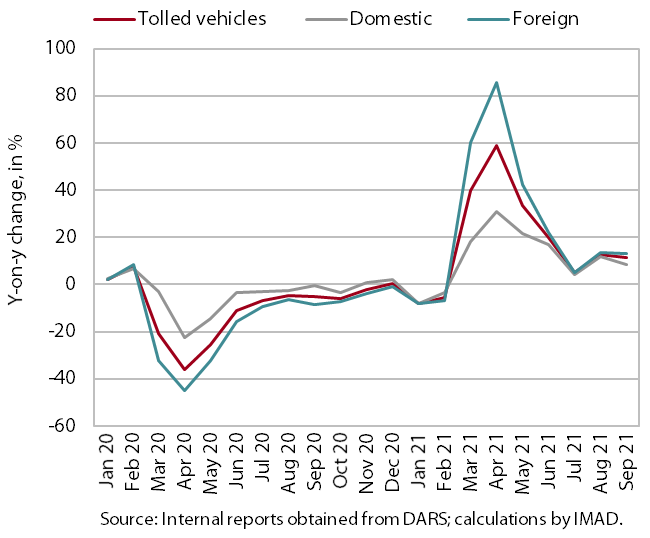

Traffic of electronically tolled vehicles on Slovenian motorways, September 2021

Freight traffic on Slovenian motorways in September was up 11% year-on-year; after adjusting the data for working days, it was almost the same as in September before the epidemic. With the number of working days being the same, the high year-on-year increase in traffic in September is still the result of a low base, i.e. lower traffic volumes during the two epidemic waves last year. Compared to September 2019, freight traffic has increased by almost 6%. This is mainly due to one more working day. After adjusting the data for the different number of working days, freight traffic in September was around 1% higher than before the epidemic. The ratio of domestic to foreign vehicles has also not changed significantly and remains at 40:60.

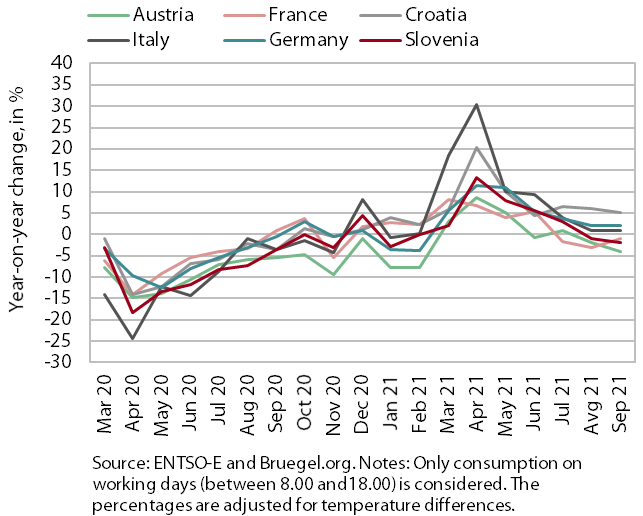

Electricity consumption, September 2021

Electricity consumption in September was 2% lower year-on-year and 4% lower than in September 2019. We estimate that the lag is related to lower industrial electricity consumption due to problems with the supply of input materials and consequently production disruptions. Among Slovenia’s main trading partners, consumption was significantly higher in Croatia (5%), which is related to a better tourist season than last year, and it was also higher in Italy (1%) and Germany (2%). In Austria and France, it was lower year-on-year, 4% and 1% respectively. Compared to September 2019, lower consumption was recorded in Austria and Italy (in both -3%), while consumption in other countries remained about the same.

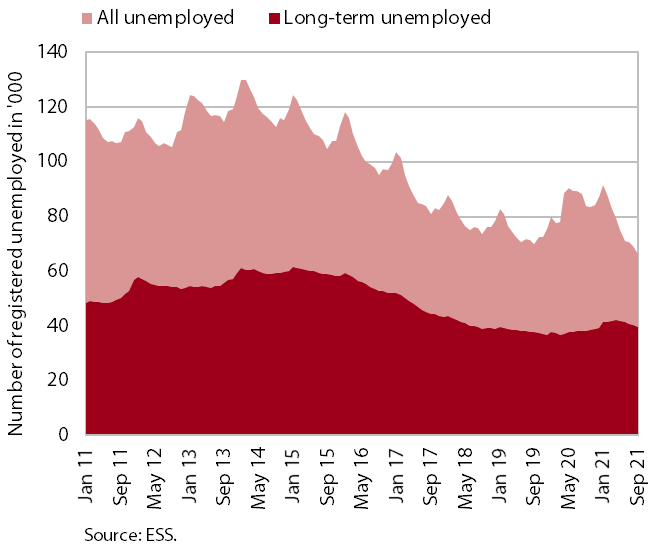

Registered unemployment, September 2021

The number of unemployed people continued to fall in September. At the end of September, 66,122 people were unemployed, 4.6% fewer than at the end of August and 21.1% fewer than a year earlier. The number of unemployed people decreased by 5.3% compared to the end of September 2019. In the first nine months, the inflow into unemployment was lower than in 2019. The outflow from unemployment has fallen in recent months, but remains higher than the inflow, which means that the number of unemployed continues to fall. Among the unemployed, the number of long-term unemployed increased in the first four months. In recent months, however, their number has fallen slightly again due to the high demand for labour. In the first nine months, an average of 41,206 people were long-term unemployed, which is 9.5% more than in the same period last year and 7.1% more than in 2019. Of the long-term unemployed, slightly more than half have been unemployed for more than two years.

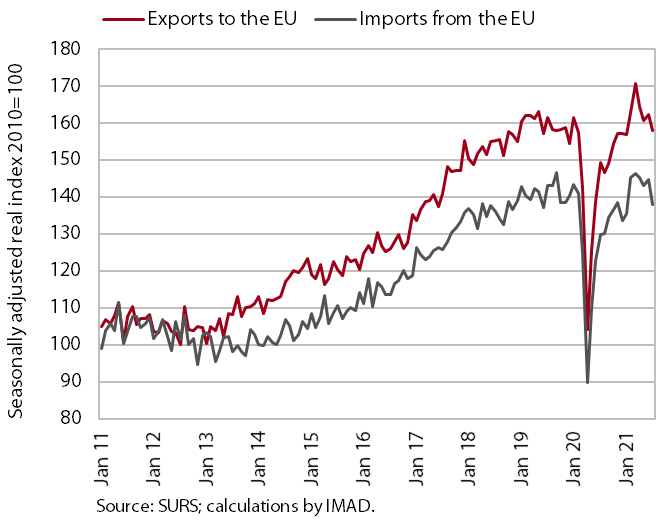

Trade in goods, August 2021

Trade in goods increased again in August, significantly exceeding pre-epidemic levels. At the same time, there have been more marked monthly fluctuations in trade with EU Member States in recent months, which we believe were mainly related to vehicle exports. Supply chain disruptions, and in particular shortages of electronic built-in components, have had a major impact on the automotive and related industries in Slovenia and its main partners in recent months. Nevertheless, in most of the main product groups (chemical products, machinery and equipment excluding vehicles, metals) the favourable development continues and the pre-epidemic levels are significantly exceeded. In recent months, exports of metals and metal products in particular have increased, which, in addition to higher exports, is also related to rising commodity prices on the world markets. Export expectations fell slightly in September, mainly due to disruptions in raw material supplies and longer delivery times, while new orders remain well above normal levels. On the import side, imports of intermediate goods remain high.