Charts of the Week

Current economic trends from 29 March to 2 April 2021: electricity consumption, traffic of electronically tolled vehicles, registered unemployment, consumer prices and other charts

In the last year, companies have tried to adapt to the changed situation to the greatest extent possible. In comparison with the first wave of the epidemic, particularly those sectors whose operations are hampered due to the very nature of activity are still the most affected. For example, turnover in accommodation and food service activities fell further year on year in January due to the continued closure of most hotels and restaurants. Despite the re-closure of most non-essential stores and hence lower sales of non-food products, turnover in trade maintained its December level in January due to an improvement in motor vehicle sales. It strengthened more markedly in February, according to preliminary data, due to the renewed opening. March data on foreign freight traffic on Slovenian motorways and electricity consumption indicate a further strengthening of industrial production, which already reached pre-crisis levels at the beginning of the year. Consumer prices were up year on year in March for the first time since last July. Their growth was mainly driven by electricity prices, which were almost 40% higher than a year earlier due to the considerable fall at the beginning of the first wave of the epidemic. The number of registered unemployed persons fell more sharply in March than in the previous month, especially due to a sharp decline in the first half of the month.

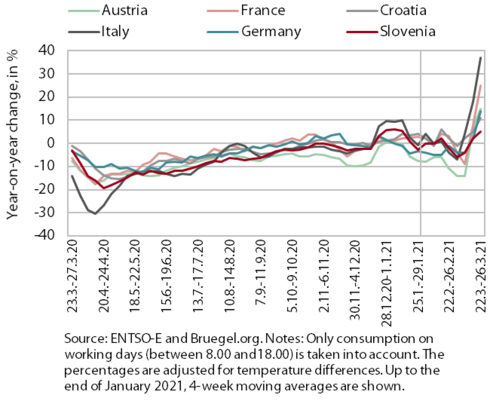

Electricity consumption, March 2021

Electricity consumption in the fourth week of March was 5% higher than in same week of 2020 but unchanged compared with the same week of the pre-crisis year 2019. This can be attributed particularly to the base effect, the renewed easing of measures in the Obalno-kraška region and the opening of restaurant terraces and gardens also in the Primorsko-notranjska region. Particularly do to the base effect, year-on-year higher consumption was also recorded in our main trading partners, from 11% in Croatia to 37% in Italy. Relative to the comparable week of 2019, consumption was down 3% and 5% in Italy and Austria, roughly the same in France, and 2% and 9% higher in Germany and Croatia.

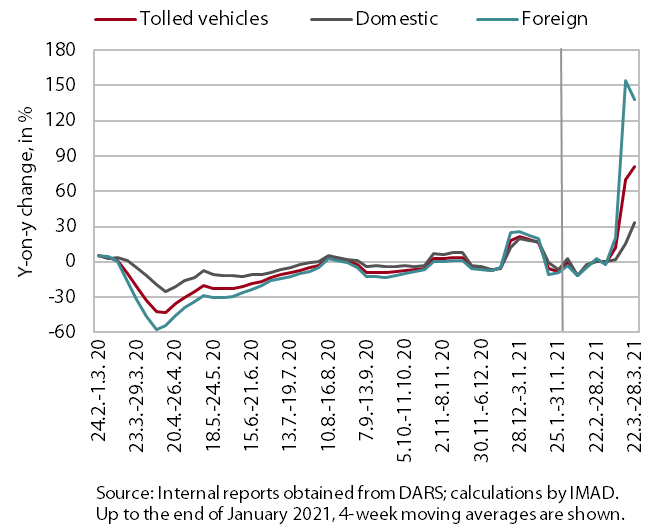

Traffic of electronically tolled vehicles on Slovenian motorways, March 2021

Freight traffic on Slovenian motorways in the fourth week of March was up 81% year on year and up 5% compared with the same period of 2019. Between 22 and 28 March, domestic vehicle traffic was 34% higher and foreign vehicle traffic 138% higher year on year. Although at the end of March the volume of freight traffic was very high, this strong growth is mainly a consequence of the base effect, given that in the same period of last year, traffic was highly limited due to the stringent containment measures. Relative to the comparable week in 2019, freight traffic was somewhat higher (in domestic vehicles by 8% and in foreign vehicles by 3%).

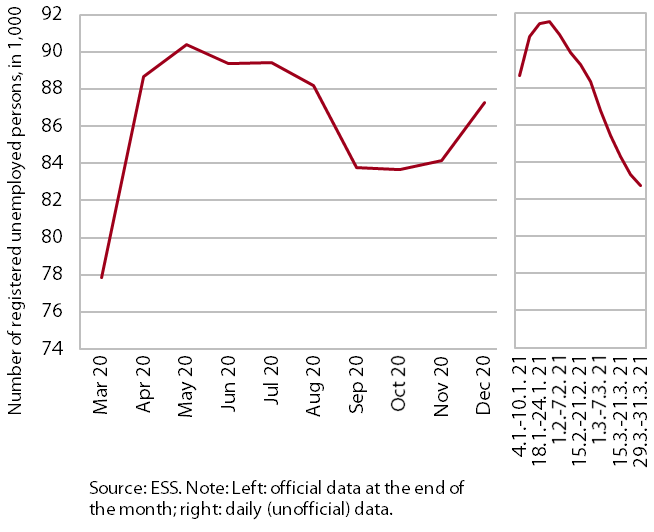

Registered unemployment, March 2021

The decline in the number of registered unemployed persons again strengthened somewhat in March. After the increase in the number of unemployed in December and January, which did not deviate significantly from seasonal increases in the same period of previous years, the number of unemployed dropped seasonally adjusted in February. In March, its decline strengthened slightly, which, in addition to seasonal factors, is also attributable to the easing of measures. At the end of March, 82,638 persons were unemployed, 6.1% less than at the end of February and 6.1% more than a year earlier.

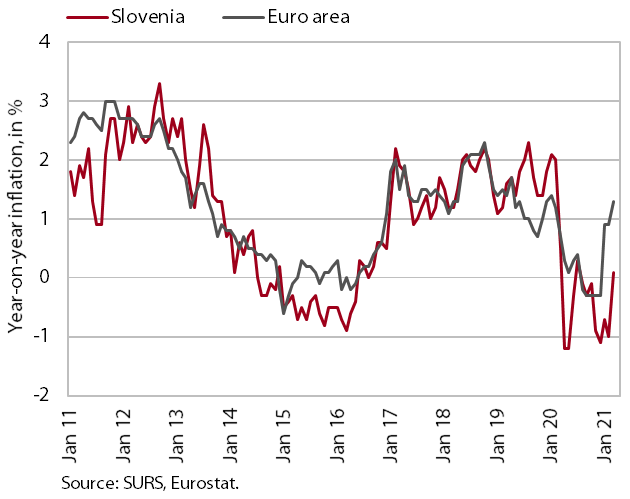

Consumer prices, March 2021

Consumer prices were up year on year in March for the first time since July last year. The increase was mainly due to higher energy prices. Electricity prices were almost 40% higher than a year earlier, which was a consequence of the substantial price fall at the start of the first wave of the epidemic, when the government temporarily exempted households and specific small business consumers from paying contributions. The year-on-year fall in oil product prices also slowed significantly, reflecting the current increase in oil prices and a lower base. The decline in prices of semi-durables strengthened further year on year in March (-5.8%) and was the most pronounced since 2006. This was again mainly due to a markedly different seasonal movement in prices of clothing and footwear than in previous years, reflecting lower demand as a result of containment measures. Also, retailers are making even greater use of discounts and other sales channels (online sales) to promote sales. Prices of durable goods were also somewhat lower, by 0.3%. The year-on-year fall in prices of services remained at roughly the same level as in the previous month (-0.4%).

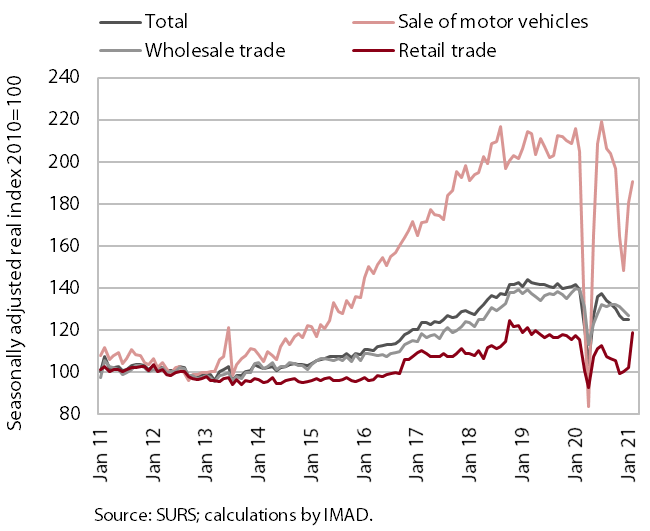

Trade, January 2021

In January, total turnover in trade was similar to that in the previous month, while in February it strengthened more markedly according to preliminary data due to the opening of all non-food stores. In January, turnover fell in wholesale trade, while strengthening in the sale of motor vehicles and retail trade. In the latter it increased due to stronger sales of food and automotive fuels, despite a significant fall in non-food sales due to the renewed closure of most non-food stores. With the opening of all shops and the removal of restrictions on movement between municipalities, turnover strengthened in all trade segments in February, according to preliminary data, the most, almost by a third, in the retail sale of non-food products.

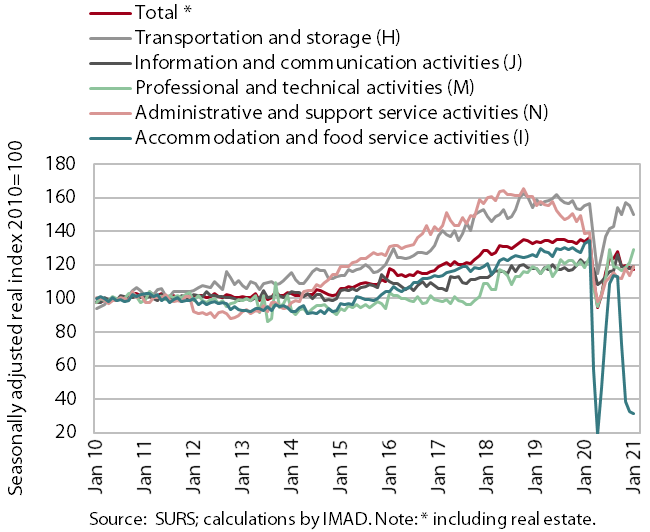

Market services, January 2021

Turnover in most market services rose in January. Real turnover growth in professional and technical activities accelerated further with renewed growth in architectural and engineering services. Strong growth was also recorded in administrative and support service activities, largely due to a halt in the decline in turnover in employment services. Turnover also increased in information and communication activities, where turnover in computer services rose on both the domestic and foreign markets. Turnover in transportation dropped due to a deterioration in road and port freight transport, and in accommodation and food service activities due to a further closure of most hotels and restaurants.

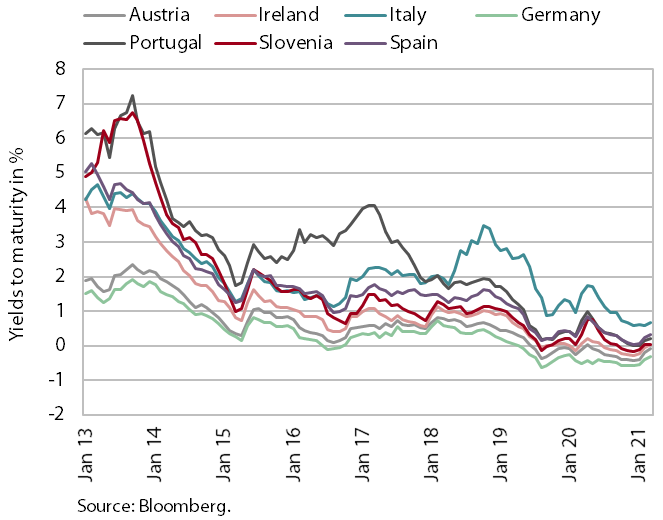

Bond, Q1 2020

The situation on euro area bond markets remained favourable in the first quarter. Amid rising consumer prices and the expected increase in public debt because of extensive support measures to mitigate the impact of the epidemic, the required yields on euro area government bond markets otherwise increased in the middle of the quarter. The situation then gradually eased following the ECB’s decision to significantly increase asset purchases under the existing emergency purchase programme (PEPP) in the second quarter. The yield to maturity of the Slovenian bond increased by around 10 basis points to -0.01% compared with the last quarter of 2020. The spread to the German bond fell to one of the lowest levels since 2007, to 40 basis points.