Charts of the Week

Current economic trends from 28 June to 2 July 2021: consumer prices, traffic of electronically tolled vehicles on Slovenian motorways, electricity consumption, trade and other charts

According to data on the fiscal verification of invoices, total turnover in the second half of June was higher than in the same period of 2019, while turnover in services where certain restrictions on activity were still in place, continued to lag significantly behind this level. Inflation fell slightly in June and the year-on-year price growth was mainly driven by higher energy prices. Freight traffic volumes on Slovenian motorways and electricity consumption remained at high levels in the fourth week of June, close to comparable 2019 levels.

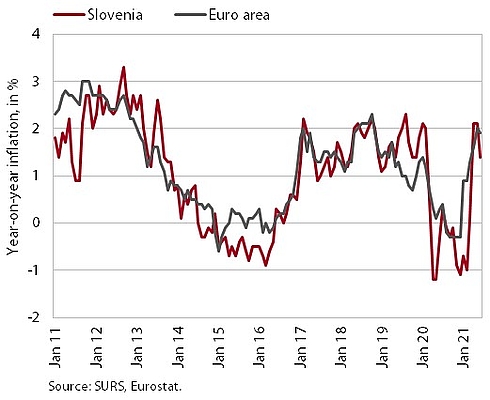

Consumer prices, June 2021

Consumer price growth slowed slightly in June to 1.4%. The contribution from energy prices, which, with a high year-on-year increase in the prices of petroleum products (by almost a quarter), contribute the most to current inflation (1 pp), decreased significantly in June. This is due to the increase in electricity prices last June (base effect), when the measure of temporary exemption from the payment of contributions for households, introduced during the first wave of the epidemic, expired. The year-on-year increase in prices for semi-durable goods remained broadly unchanged in June (1.7%), while the month-on-month growth in durable consumer prices almost halved (0.9% year-on-year). The prices of food and services remain lower year-on-year, but are gradually approaching last year's levels.

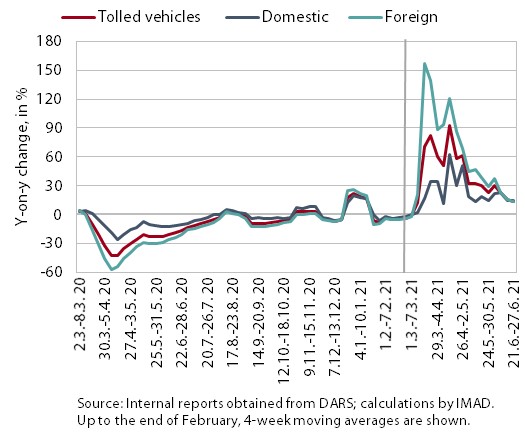

Traffic of electronically tolled vehicles on Slovenian motorways, June 2021

Freight traffic on Slovenian motorways in the fourth week of June was 14% higher than in the same period of last year and slightly lower as in the same week of 2019. The volume of freight traffic was one tenth lower than in the previous very busy week due to the Statehood Day on Friday. The significant year-on-year higher levels are still mainly due to the lower traffic volume in the same period last year after the first wave of the epidemic. Compared to the same week in 2019, the volume of domestic vehicle traffic was 5% higher and the volume of foreign vehicle traffic was 4% lower, but the share of foreign vehicle traffic was about the same as the average share in the pre-crisis year, at just over 60%.

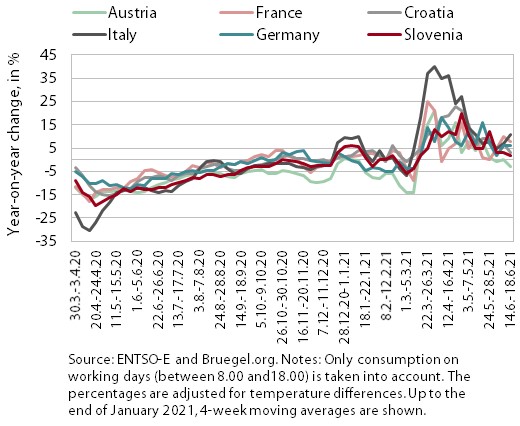

Electricity consumption, June 2021

In the week between 21 and 25 June, electricity consumption was 14% higher than the same week in 2020 and 1% higher than the same week of the pre-crisis year 2019. We estimate that the reason for a slightly higher spending than before the crisis is primarily the timing of the Statehood Day in 2019, and the reason for the higher year-on-year spending is the combination of the holiday timing and the low base in 2020. Particularly due to the base effect, year-on-year higher consumption was also recorded in the majority of Slovenia’s main trading partners (from 1% in Austria to 14% in Italy), except in France, where it was 2% lower. Compared to the same week of 2019, all partner countries recorded lower consumption, Austria by 2%, France and Croatia by 6%, Italy by 4% and Germany by 1%.

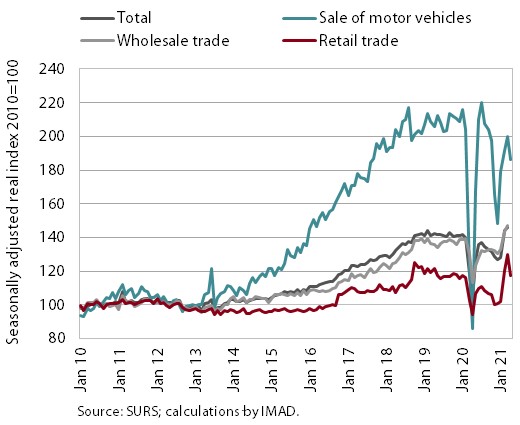

Trade, April 2021

Turnover in trade declined in April and strengthened in May according to preliminary data. After high growth in March, turnover declined in April, due in part to the partial closure of certain stores and services at the beginning of the month and the limited movement between regions in the first three weeks of the month. Turnover fell in all three main sectors, most markedly in the retail sector, where non-food sales dropped particularly strongly. According to preliminary data, turnover in retail trade picked up again in May.

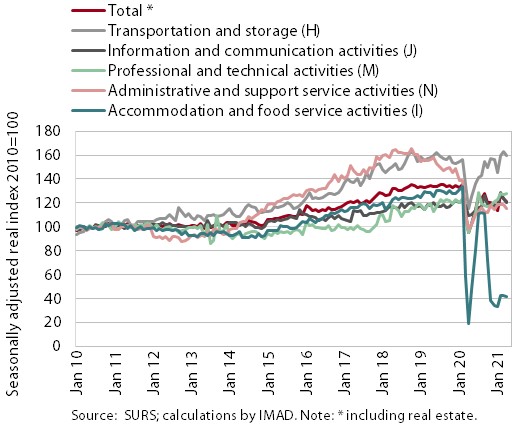

Market services, April 2021

In most market services, turnover declined in April. Compared with the previous month, real turnover fell by 2.4% but was still higher than a year earlier (by 27.2%), mainly because of the low base. With severe restrictions on business and movement between regions, the decline in revenue in the hospitality and tourism-related activities (travel agencies) has deepened. Turnover declined also in information and communications activities, although computer services contributed to increased sales in foreign markets. Turnover in transport also fell in most activities. It increased slightly only in professional and technical activities. In April, the year-on-year turnover trend was positive in all market services due to last year's low base.

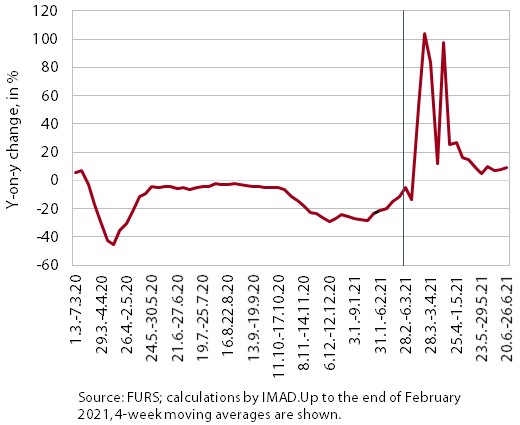

Fiscal verification of invoices, May 2021

According to data on the fiscal verification of invoices, turnover between 13 and 26 June was 8% higher year-on-year and 4% higher than in the same period of 2019. Favourable trends continued in the retail trade, where sales increased by 6% year-on-year and compared to 2019 due to growth in the wholesale and retail trade. In most, mainly tourism-related sectors (accommodation, gambling and betting, travel agencies), as well as cultural, recreational, sports and personal services, turnover growth was even higher year-on-year, but around 40% lower than in the same period of 2019, due to the ongoing constraints on certain business activities.

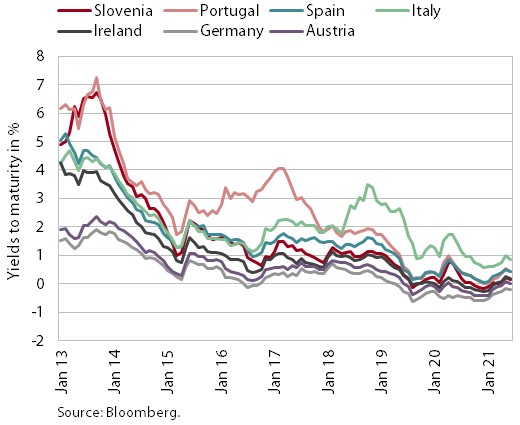

Bond, Q2 2021

The situation on euro area bond markets remained favourable in the second quarter. ECB had a significant impact on this, as it significantly increased its purchases of securities under the PEPP programme at the end of the first quarter in light of the rise in required government bond yields in the euro area. The yield to maturity of the Slovenian bond was thus 0.14%, while the spread to the German bond declined slightly, to 36 basis points.