Charts of the Week

Current economic trends from 28 February to 7 March 2022: gross domestic product, active and inactive population, registered unemployment and other data

Real GDP rose 10.4% year-on-year in the final quarter of last year and 8.1% in 2021 as a whole. The growth exceeded expectations and mainly reflects the continued successful adjustment of the economy and the population to the changed situation. The growth in private consumption was particularly surprising, as turnover in trade and market services recorded a rapid growth despite the containment measures (see also Komentar BDP) Although growth in manufacturing slowed due to supply chain disruptions, the growth of trade in goods accelerated. Labour market conditions remained favourable at the beginning of 2022. The number of unemployed in February was a quarter lower than a year ago and also much lower than before the epidemic in February 2020. Inflation picked up significantly again in February (6.9% year-on-year), mainly due to higher prices of energy, food and non-energy industrial goods and, to a somewhat lesser extent, prices of services.

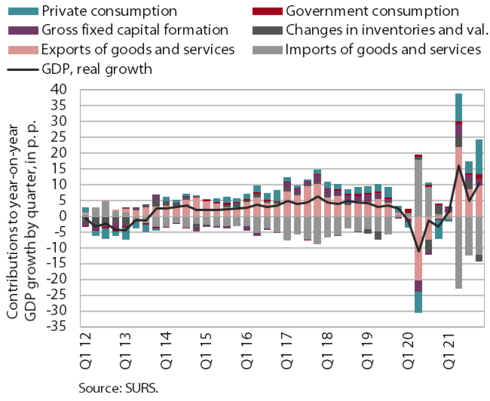

Gross domestic product, Q4 2021

In the last quarter of last year, real gross domestic product (GDP) rose by as much as 5.4% quarter-on-quarter and by 10.4% year-on-year. In the year as a whole, GDP grew by 8.1%. GDP exceeded pre-crisis levels from the last quarter of 2019 in the third quarter, while most activities exceeded them during the year, with the exception of tourism-related activities and high-contact activities. GDP growth in 2021 exceeded IMAD’s expectations from its Autumn Forecast and also IMAD's December 2021 estimate, largely reflecting the continued successful adjustment of the economy and the population to the changed situation. Household spending accelerated and, somewhat surprisingly, growth of trade in goods picked up significantly in the last quarter, despite ongoing problems related to supply chain disruptions. Investment activity last year was driven mainly by investment in equipment and machinery, while the less favourable development in the construction sector was characterised by rising prices and problems with the supply of materials. Final government consumption also increased last year, mainly due to expenditure to contain the epidemic.

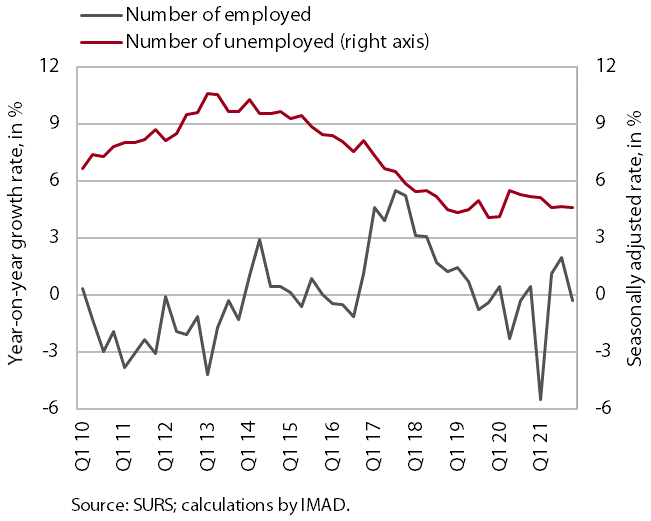

Active and inactive population, Q4 2021

According to the survey data, labour market conditions remained favourable in the last quarter of 2021. The number of employed persons (according to the original data) decreased by 0.3% year-on-year, and increased by 0.1% compared to the final quarter of 2019. The volume of student work increased by 53% year-on-year, which, in addition to the strong base effect, indicates a strong increase in demand for various types of work due to labour shortages. At the end of last year, the number of unemployed decreased by 11.3% year-on-year and the survey unemployment rate decreased by 0.6 p.p. to 4.5%.

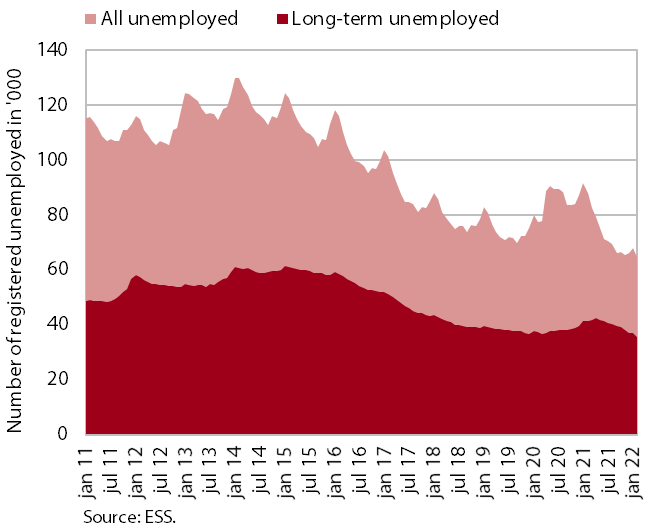

Registered unemployment, February 2022

According to seasonally adjusted data, the decline in the number of registered unemployed was slightly lower in February than in previous months (-2.3%). According to original data, 64,783 people were unemployed at the end of February, 4.5% fewer than at the end of January and 26.4% fewer than a year earlier. The number of unemployed was also lower (by 16.4%) than at the end of February 2020. Among the unemployed, the number of long-term unemployed increased in the first four months of last year but then decreased again by the end of the year, given the high demand for labour, which is also reflected in the high rate of job vacancies. The number of long-term unemployed continued to fall in the first two months of 2022 – in February their number fell by 13.5% compared to February last year and by 4.3% compared to the pre-epidemic period two years ago. Of the long-term unemployed, more than half have been unemployed for more than two years.

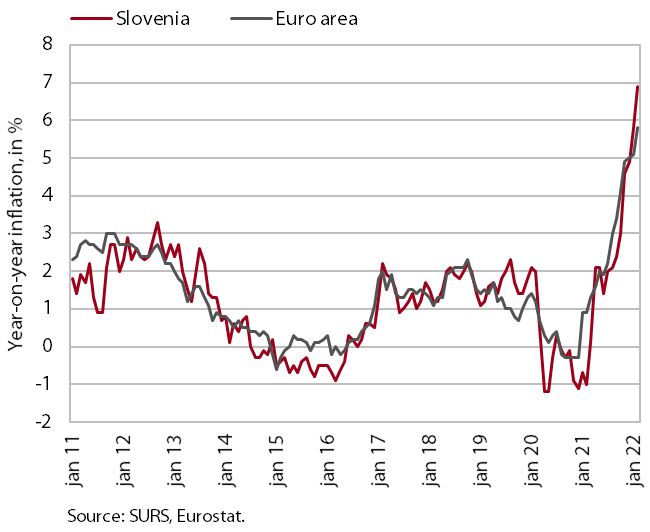

Inflation, February 2022

Inflation picked up sharply again in February (6.9% year-on-year), driven largely by very broad increase in goods prices. The increase resulted mainly from higher prices of energy, food and non-energy industrial goods and, to a somewhat lesser extent, services prices. After the prices for petroleum products and heating fuels rose significantly last year, the prices for other energy sources (gas, electricity and, to some extent, solid fuels) are also rising rapidly this year. As a result of the increase in the prices of energy and inputs, food price growth has also increased significantly, amounting to 6.4% year-on-year. Growth in the prices of durable (vehicles and furniture) and semi-durable goods continues to strengthen. Prices for the latter still fluctuate widely due to different seasonal developments in the clothing and footwear group. However, higher demand with less stringent containment measures led to stronger growth in holiday package prices, which in turn led to stronger growth in services prices.

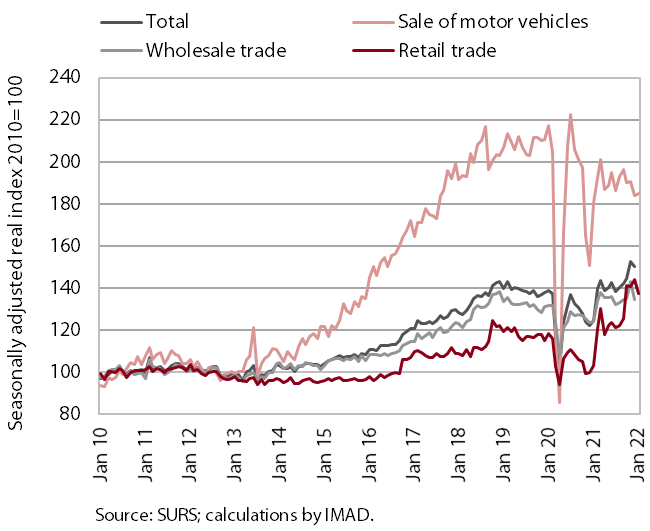

Turnover in trade, December 2021–January 2022

Turnover in trade increased in the last quarter of 2021, outpacing 2019 turnover by 4% in 2021 as a whole. Turnover, which was high in November, fell slightly in December but was significantly higher on average in the last quarter than in the third quarter. The only quarter-on-quarter decline in turnover was recorded in the sale of motor vehicles, which was the only main segment still below pre-epidemic levels. In the last quarter, total turnover in trade increased by a fifth year-on-year, which was also influenced by the low base due to restrictions on business and movement in the last quarter of 2020. In 2021 as a whole, it was 12% higher in real terms than in 2020 and 4% higher than in 2019.

According to preliminary data, turnover in the sale of motor vehicles and in the retail sale of food increased in January this year, while it decreased in the retail sale of automotive fuel and non-food products.

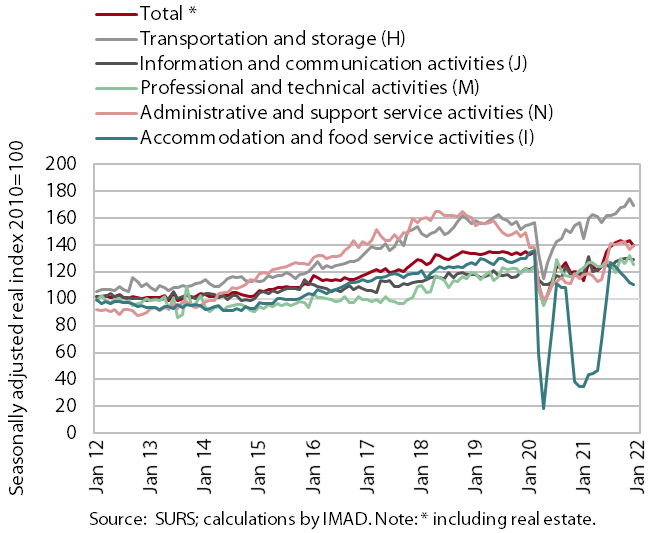

Turnover in market services, December 2021

Real turnover in market services remained unchanged in the last quarter of 2021 but was significantly higher year-on-year. The highest quarter-on-quarter increase was recorded in transportation and storage, particularly in warehousing. Turnover also increased in information and communication activities, reflecting higher turnover in computer services in the domestic and foreign markets. After a slight decline in the previous quarter, turnover increased in all professional and technical activities . After high growth in the third quarter, turnover decreased in accommodation and food service activities and in administrative and support service activities, in the latter mainly due to a further decline in turnover in employment agencies. Year-on-year, turnover increased by 18.3% in the final quarter of 2021 and by 12.6% overall in 2021. Compared to the same quarter in 2021, it was higher in all market services and compared to the same quarter in 2019, it was significantly lower in travel agencies (by 47%) and in food and beverage service activities, publishing activities and employment agencies (by 19% on average).