Charts of the Week

Current economic trends from 24 to 28 May 2021: economic sentiment, traffic of electronically tolled vehicles, electricity consumption, registered unemployment and other charts

The easing of containment measures had a favourable impact on economic activity and confidence in May. Confidence in most sectors, particularly trade and service activities, improved further. Activity in the majority of these sectors had already increased in the first quarter, while the sectors related to tourism and accommodation and food services, where activity declined further, remained strongly affected. Developments in industry remained relatively favourable, which is indicated by the indicators of confidence and freight traffic on Slovenian motorways. Freight traffic in the third week of May was higher than in the same week of the pre-crisis year, while electricity consumption remained somewhat lower. The decline in the number of unemployed continued, even accelerating slightly in the second half of May.

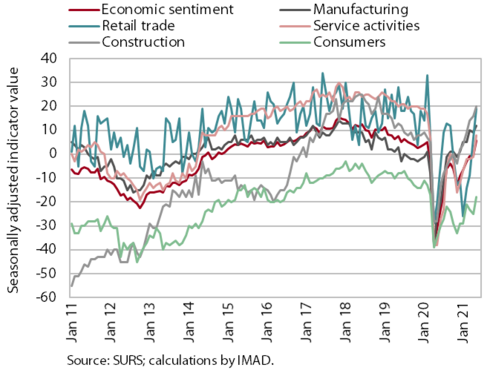

Economic sentiment, May 2021

In May, economic sentiment has improved in most sectors. With the gradual relaxation of some containment measures in May, and particularly with the opening of accommodation and food service establishments, confidence has improved the most in trade and service activities. Confidence in the export-oriented part of the economy and construction has improved as well, being higher than before the beginning of the epidemic. Consumer confidence has remained low but it is improving gradually. Compared with the period before the epidemic, consumers are more pessimistic particularly about future economic conditions and, hence, their future financial situation.

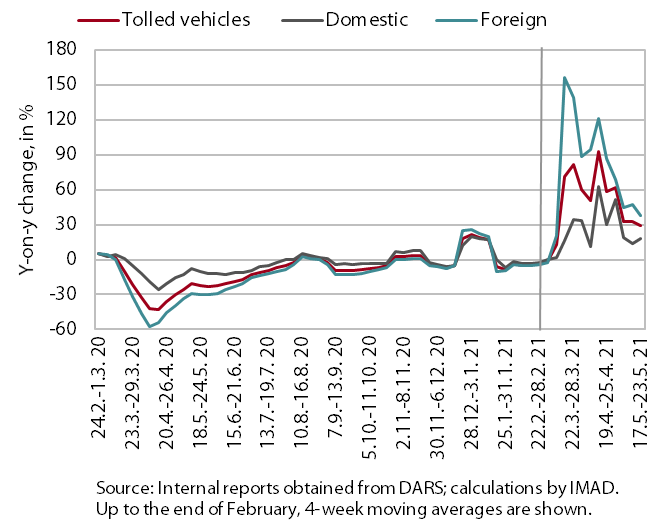

Traffic of electronically tolled vehicles on Slovenian motorways, May 2021

Freight traffic on Slovenian motorways in the third week of May was 29% higher than in the same period of last year and 1% higher than in the same period of 2019. The volume of freight traffic was, as in the previous week, very high and somewhat higher than in the same week of the pre-crisis year 2019 (equally in domestic and foreign vehicles). Between 17 and 23 May, domestic vehicle traffic was 18% higher and foreign vehicle traffic 38% higher year on year. This strong year-on-year growth was still mainly a consequence of lower traffic in the same period of last year due to the first wave of the epidemic (when freight traffic of foreign vehicles declined more).

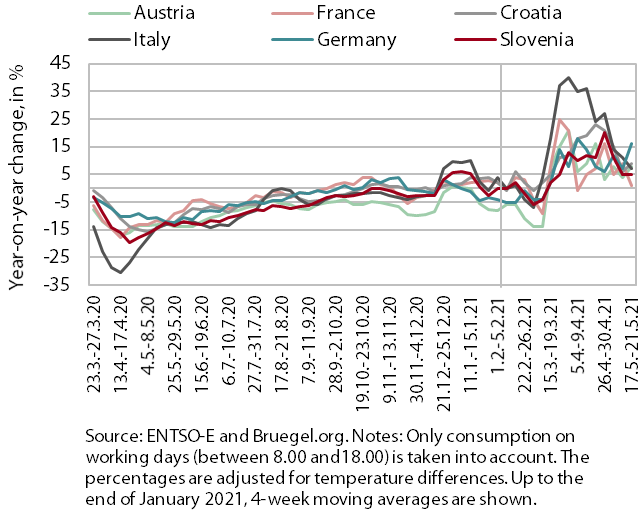

Electricity consumption, May 2021

Electricity consumption in the third week of May was 5% higher compared with the same week of 2020 but 5% lower compared with the same week of the pre-crisis year 2019. The reason for the year-on-year higher consumption between 17 and 21 May was last year’s low base. Despite the relaxation of a number of containment measures, consumption did not yet reach pre-crisis levels. As a result of the base effect, higher consumption year on year was also recorded in our main trading partners, from 1% in France to 16% in Germany. Relative to the same week of 2019, consumption was down in most trading partners (in France by 9%, in Austria by 7%, in Italy and Germany by around 3%, and in Croatia by 1%).

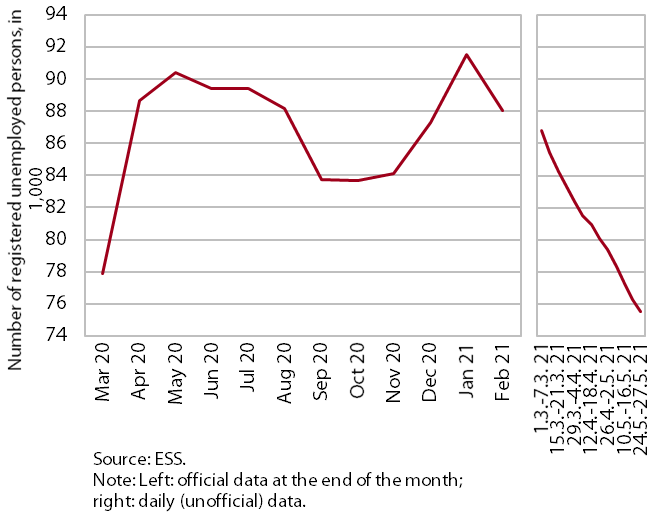

Registered unemployment, May 2021

The number of registered unemployed persons fell further at the end of May. Amid seasonal impacts, which did not deviate significantly from those in the period before the epidemic, the decline was also related to the gradual relaxation of containment measures. On 27 May, 75,269 persons were unemployed according to ESS unofficial (daily) data, which is 5.1% less than at the end of April and around 17% less than one year earlier. Compared with May 2019, the number was, however, around 5% higher.

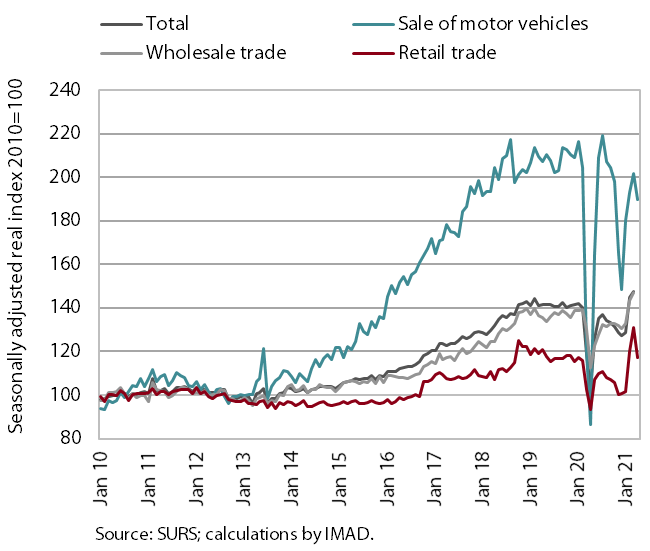

Trade, March 2021

Turnover in trade strengthened in the first quarter and was higher year on year; due to the renewed partial closure of shops, it fell again in April according to preliminary data. After February’s strong growth related to the re-opening of shops and the lifting of the ban on movement between municipalities, turnover also strengthened further in March. In the first quarter as a whole, it was up 4.2% year on year, reflecting strong year-on-year growth in March, which, in addition to the low base, was also a consequence of increased sales before the re-closure of some shops and of the distribution of Easter holidays. Year on year, turnover was up in the first quarter in all three main segments, the most, by 8.9%, in the sale of motor vehicles, where high sales of new passenger cars to natural persons stood out in particular. In April, turnover fell according to preliminary data under the impact of increased sales at the end of March and the partial closure of shops at the beginning of the month.

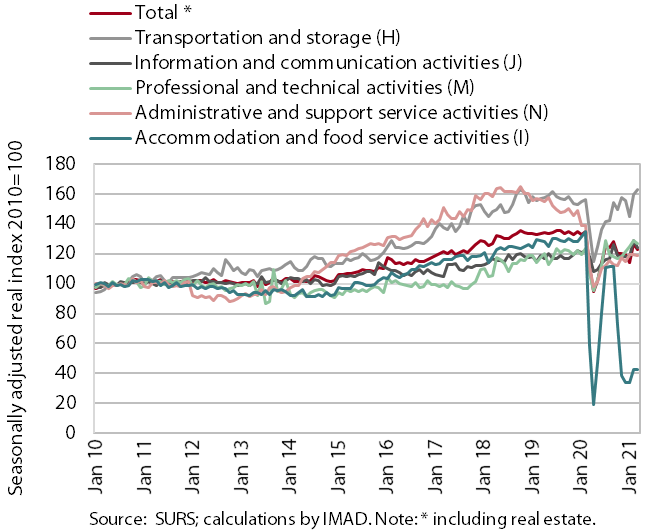

Market services, March 2021

Total turnover in market services again increased slightly in the first quarter; it fell only in accommodation and food service activities. Real turnover rose by 1.3% relative to the last quarter of 2020, while at the year-on-year level, it was 3.4% lower. With restrictions on activity still in place, turnover dropped further in accommodation and food service activities. It strengthened the most in professional and technical activities, reflecting accelerated growth in architectural and engineering services and consultancy activities. It was also up in information and communication activities, particularly on account of higher turnover in computer services on the domestic market. In administrative and support service activities, turnover growth increased somewhat further mainly as a consequence of renewed growth in employment services. Meanwhile, the strong turnover growth in transport decelerated. Turnover in travel agencies and accommodation and food service activities remained significantly below last year’s levels (by more than 80% and 60% respectively). However, in professional and technical activities, transport, and information and communication activities, last year’s turnover levels were already exceeded in this period.