Charts of the Week

Current economic trends from 24 to 28 February 2020: GDP, active and inactive population, prices and others

Economic growth slowed down last year, particularly growth in investment and exports being lower year on year. Amid still relatively favourable labour market conditions, household consumption increased further last year. Most sectors recorded more modest growth in activity year on year. In the service sector, activity growth slowed more visibly at the end of the year.

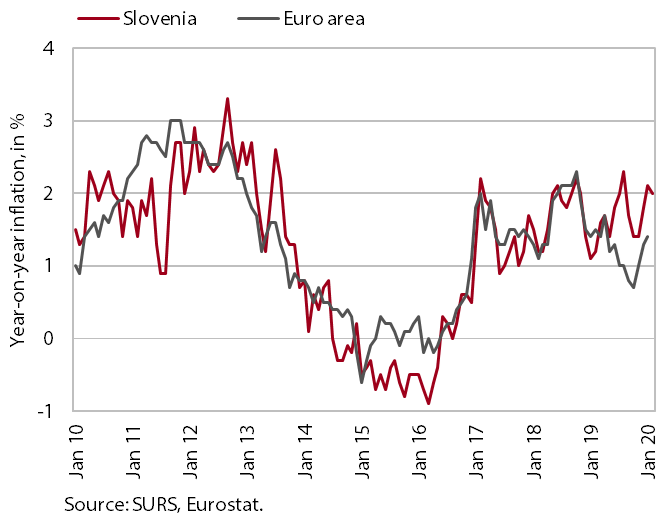

Consumer price growth was hovering around 2% in the first months of this year; growth in prices of services remains higher.

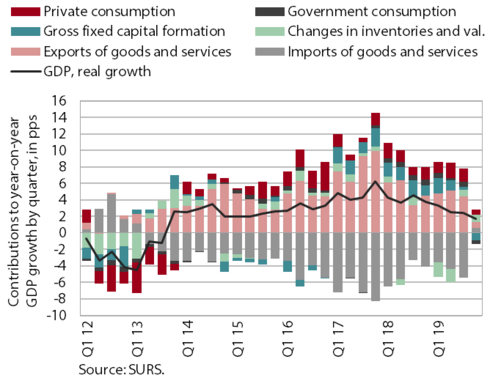

GDP, Q4 2019 and the entire 2019

Real GDP growth eased year on year to 1.7% in the last quarter of 2019, totalling 2.4% for the year as a whole, which is considerably less than in 2018 (4.1%). Growth in exports and, in particular, investment slowed noticeably. In the last quarter their volume dropped further relative to the previous quarter, which was, in addition to lower economic growth in trading partners, to a great extent due to uncertainty in the international environment. The slowdown in export growth and growth in industrial production started to spill over into the service sector more visibly towards the end of the year. Household consumption remained strong, supported by relatively high growth in employment and growth in wages and social transfers. As these developments were also reflected in slower growth in imports, net exports made a positive contribution to GDP growth last year (0.5 pps).

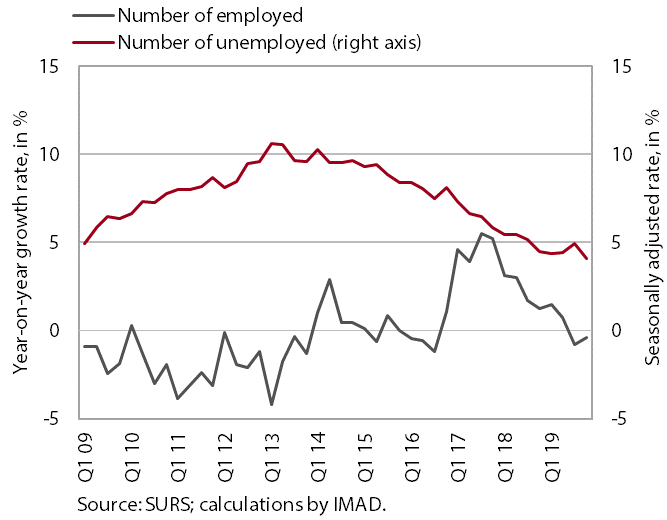

Active and inactive population, Q4 2019

According to the Labour Force Survey data, employment remained high in the last quarter of 2019, while unemployment was the lowest thus far. The number of employed persons increased further (mainly as a result of the hiring of foreigners), while the number of self-employed persons and unpaid family workers declined slightly again. ILO unemployment was the lowest thus far, in terms of both number and rate (4%).

Prices, February 2020

In February consumer prices were 2% higher year on year. Growth in food prices strengthened again amid further growth in prices of meat and fruit. The contribution of energy dropped due to a monthly decline in prices of oil products. Price growth in services remained just above 2.5%. The high growth of insurance prices and prices of housing-related goods and services continued. Prices of package holidays were also somewhat higher than last year. Growth in prices of semi-durable goods strengthened slightly in February (to 1.1%), while prices of durable goods remained down year on year.

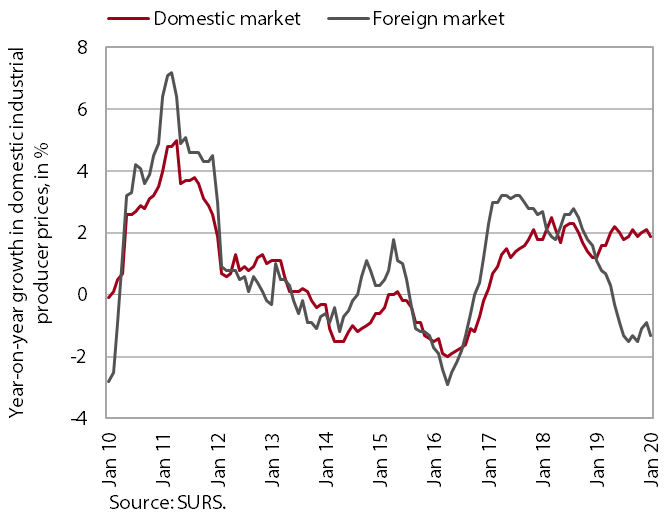

Slovenian industrial producer prices, January 2020

Total year-on-year growth in Slovenian industrial producer prices moderated further in January. The decline in prices on foreign markets (especially in the euro area) deepened. Particularly prices of investment goods declined in January. The year-on-year decline in raw material prices also made a significant contribution to the somewhat lower price growth on the domestic market. This otherwise remains at around 2%, one of the main reasons being high (around 15%) price growth in electricity, gas and steam supply. Growth in household consumption and rises in meat prices are reflected in a strengthening of consumer price growth on the domestic market, which was the highest since 2007, at 2.7%.

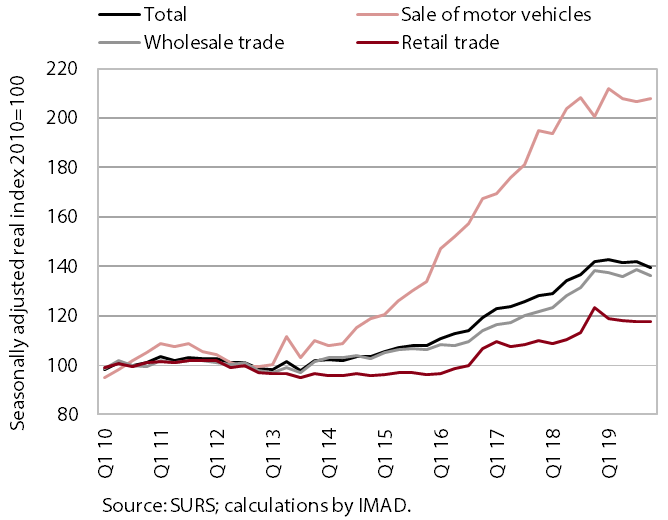

Trade, December 2019

Following first-quarter growth, turnover in trade remained at a similar level until the end of last year. After increasing at the beginning of the year, turnover in wholesale trade remained practically unchanged, which was also due to less favourable developments in some trade-related activities (transportation, construction and manufacturing). Since the beginning of 2019, turnover has also remained more or less unchanged in retail trade, within which the sale of automotive fuels was declining throughout the year, while the sale of non-durable goods was rising amid increased household consumption. Following a decline in the middle of the year, turnover in trade of motor vehicles improved somewhat at the end of last year under the impact of higher passenger car sales to natural persons and December’s high growth of sales to legal persons.

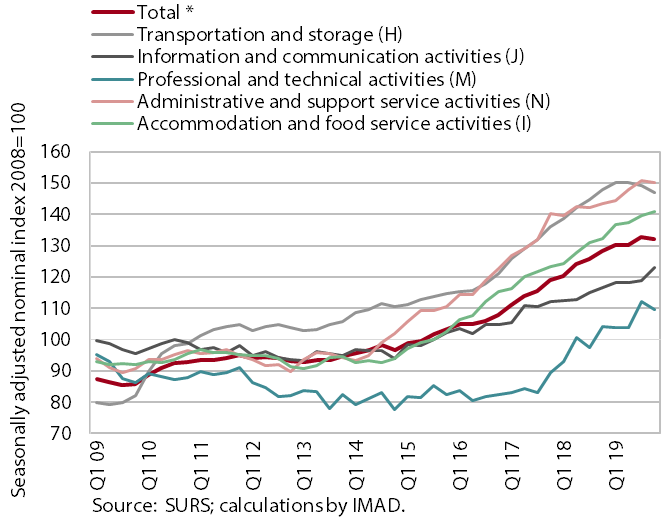

Market services, December 2019

Turnover in market services dropped slightly in the last quarter after strengthening in the first three. The decline in turnover was largest in professional and technical activities, mainly owing to a further fall in architectural and engineering services. Turnover also continued to decline in most activities of transportation, especially port traffic due to a lower volume of goods handled. Turnover in administrative and support service activities dropped somewhat, mainly as a consequence of declining turnover in employment services. Turnover growth in accommodation and food service activities eased somewhat, partly due to a lower number of foreign tourist visits than one year earlier. Turnover growth in information and communication activities accelerated due to growth in telecommunication services.

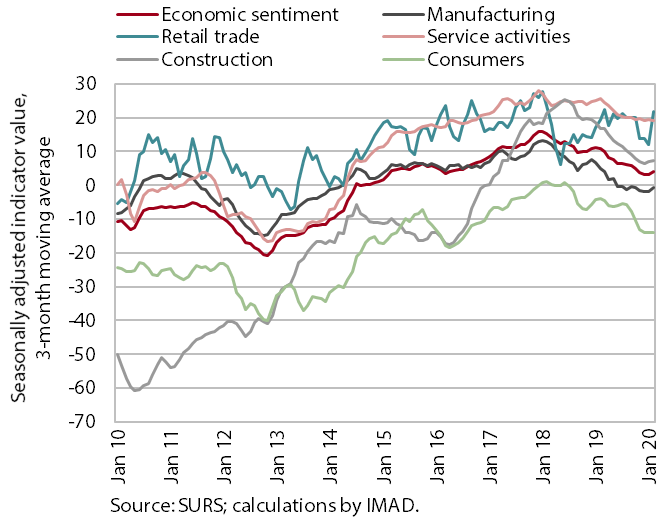

Economic sentiment, February 2020

Economic sentiment improved slightly at the beginning of this year; however, the survey was conducted before the outbreak of coronavirus in Italy. In addition to retail trade, confidence improved slightly in manufacturing and construction. Confidence in service activities remained fairly high, while confidence among consumers remained almost unchanged. Although improving in all activities and among consumers, confidence remains significantly lower than in the same period of last year. However, as the survey was conducted in the first half of February, economic sentiment indicators do not yet include the response of companies and consumers to the outbreak of coronavirus in Italy.