Charts of the Week

Current economic trends from 20 to 24 December 2021: economic sentiment, Slovenian industrial producer prices, wages and other

Economic sentiment and consumer confidence improved slightly at the end of the year, but remain lower than in the previous quarter. Slovenian industrial producer prices continue to rise rapidly, and the year-on-year increase is mainly due to higher prices of intermediate goods. Growth in average gross wages in the private sector remains high year-on-year. This is mainly due to the increase in the minimum wage at the beginning of the year, but also to the return to employment of workers who had participated in job retention measures and labour shortages in some sectors. Year-on-year public sector wage growth slowed significantly in the second half of the year (cessation of epidemic-related bonus payments). With relatively high turnover in the real estate market, average dwelling price growth accelerated in the third quarter.

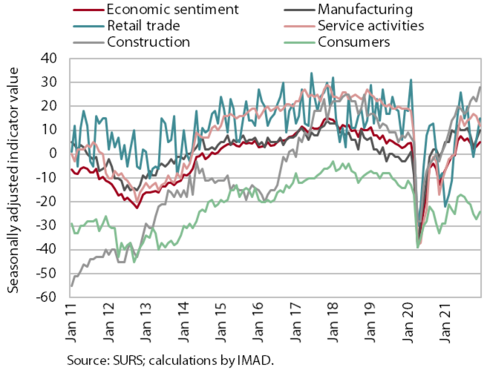

Economic sentiment, December 2021

The Economic Sentiment Indicator improved in December, but the average value for the last three months points to a slowdown in economic activity in the last quarter. At the monthly level, confidence improved in most activities and among consumers. Confidence thus remained significantly higher in December than in the same period last year, and was also higher in manufacturing and construction than in the same period in 2019. Despite the improvement in the last two months, confidence in most activities deteriorated compared to the previous quarter. The deterioration in manufacturing is the result of current situation in the international environment (supply bottlenecks, rising non-energy commodity and energy prices), while the deterioration in the retail trade and among consumers was caused by uncertainty about the epidemic situation and measures. On the positive side, confidence in construction stands out, which increased significantly in the last quarter and is well above the long-term average.

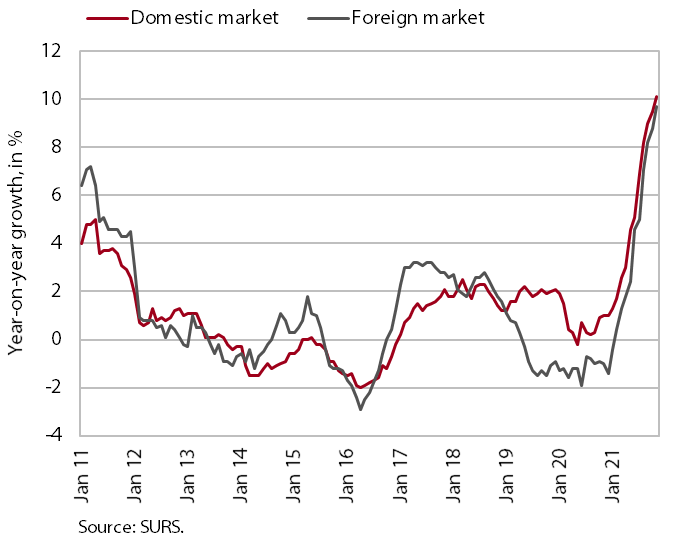

Slovenian industrial producer prices, November 2021

Slovenian industrial producer prices continue to rise. They increased by almost a tenth year-on-year in November. Prices are rising across all industrial groups, both in the domestic and foreign markets. Overall growth continues to be driven mainly by prices in the intermediate goods group, which rose by around 15% year-on-year. The increase in prices for capital goods has stabilised at around 8.5% over the past three months. Energy prices have also risen and despite the increase in the last two months, their year-on-year growth in the domestic market remains relatively low (3.7%). In the face of production bottlenecks and higher non-energy commodity (intermediate goods) and energy prices, prices for consumer goods, which rose by 3% year-on-year, increased more in November than in previous months. Prices in the durable goods group rose somewhat more strongly, by about 4%, while prices for non-durable consumer goods increased by about 3% year-on-year.

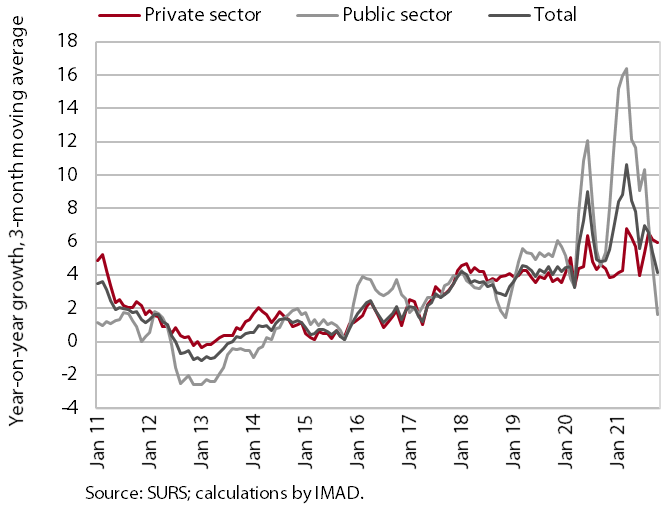

Wages, October 2021

Year-on-year wage growth in the public sector was low in October (0.5%), while it remained relatively high in the private sector (5.7%). Year-on-year public sector wage growth slowed significantly in the second half of the year due to the cessation of epidemic-related bonus payments. In the first ten months, public sector wages were 9.1% higher than in the same period last year. In the private sector, average wages increased by 5.7% year-on-year in the first ten months, mainly due to the impact of the minimum wage increase at the beginning of the year, but also to the return to employment of workers who had participated in job retention measures. According to our estimates, wage growth in some private sector activities (administrative and support service activities, construction and accommodation and food service activities) may already be affected by labour shortages.

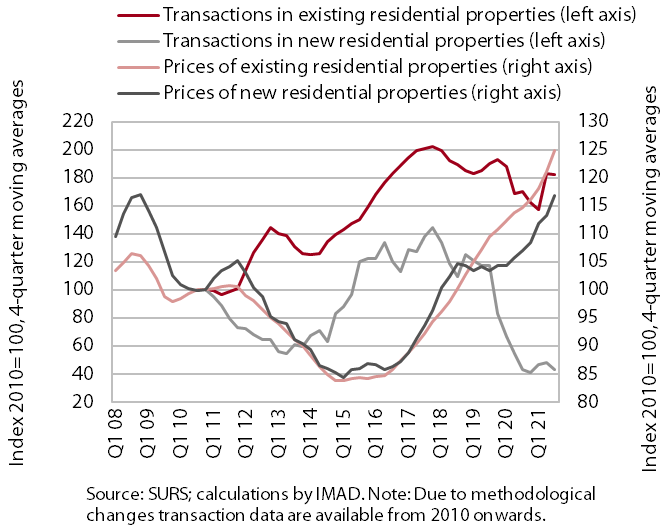

Real estate, Q3 2021

Given the relatively high number of transactions, average dwelling price growth accelerated in the third quarter. Prices were up 12.9% year-on-year and 10.1% overall in the first nine months, which is a strong acceleration from the average growth of 4.6% in 2020. In the third quarter, year-on-year price increase was similar (by about 13%) for both existing and newly built dwellings (the latter account for only 1% of all transactions). According to our estimates, the growth of prices this year is influenced by several factors. On the supply side, the main factors affecting prices for several years are the low supply of newly built dwellings and, more significantly this year, higher prices for construction raw materials. On the other hand, the price increase is influenced by increased household demand stimulated by the rise in total savings during the epidemic, the maintenance of relatively high disposable income and the persistence of favourable credit conditions (new housing loans rose by more than a third year-on-year in the year to October).