Charts of the Week

Current economic trends from 19 to 23 July 2021: economic sentiment, traffic of electronically tolled vehicles, electricity consumption, Slovenian industrial producer prices and oter charts

Freight traffic volumes on Slovenian motorways remained at a relatively high level in mid-July, close to those of the same period in 2019. With the gradual strengthening of activity in the tourism sector, electricity consumption approached the level of the same period in 2019. The value of the sentiment indicator deteriorated slightly in July, but remained well above last year's average and close to the 2019 level in all indicators, mainly due to the release of containment measures in recent months. The growth in Slovenian industrial producer prices continued to rise sharply in June, reaching its highest level in the last decade mainly due to higher commodity prices. In May, average wage growth was again relatively high, in particular due to high growth in the public sector.

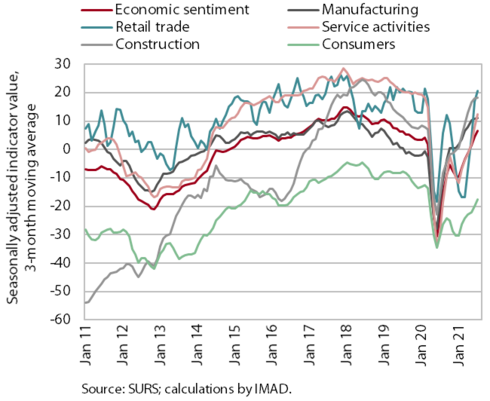

Economic sentiment, June 2021

In July, the value of the sentiment indicator deteriorated slightly. On a monthly basis, confidence in trade and services fell to May’s levels after rising June due to the release of measures. Confidence in construction, manufacturing and among consumers also fell slightly. After rising to last March's level in May, consumer confidence has remained unchanged for the past three months. Consumers are particularly concerned about the future economic situation. However, across all indicators, it was well above last year's average and around 2019 levels due to the gradual release of containment measures in May and June.

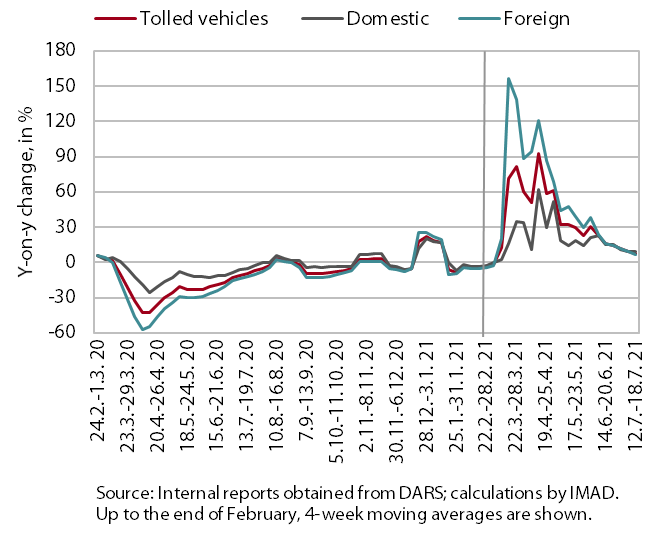

Traffic of electronically tolled vehicles on Slovenian motorways, July 2021

Freight traffic on Slovenian motorways in the third week of July was 8% higher than in the same period last year and the same as in the same period of 2019. The significant year-on-year increase is still mainly due to the low base, namely lower traffic volume in the same period last year after the first wave of the epidemic. The volume of freight traffic was relatively high in the third week of July, as it was in the previous two weeks of July, and as high as it was in the same week in 2019 (with a slightly higher share of domestic vehicles).

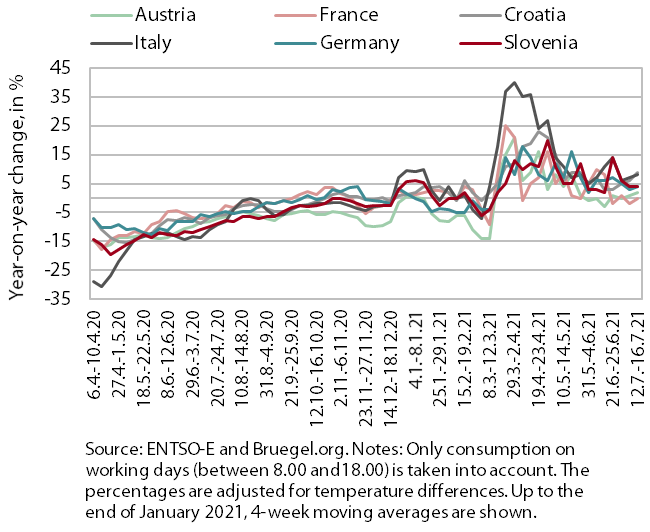

Electricity consumption, July 2021

In the week between 12 and 16 July, electricity consumption was 4% higher year-on-year, but 2 % lower than the same week in 2019. The reason for the higher year-on-year consumption is mainly due to the low base of last year, and the gap with the same week in 2019 narrowed further, mainly due to higher activity in the tourism sector. Particularly due to the base effect, higher year-on-year consumption was also recorded in most of Slovenia’s main trading partners (2% in Austria, 4% in Germany and around 9% in Italy and Croatia), except in France, where it remained the same. Also compared to the same week of 2019, most of partner countries recorded the same (Germany) or higher consumption (Austria and Italy by 2%, Croatia by 6%), with the exception of France (-6%).

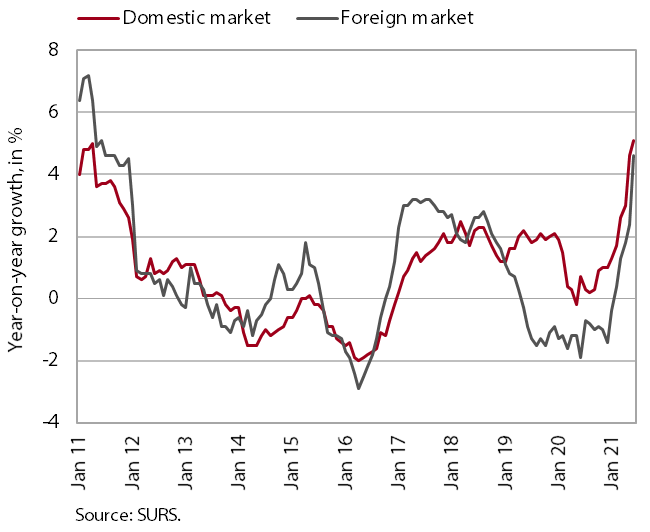

Slovenian industrial producer prices, May 2021

Year-on-year growth in Slovenian industrial producer prices continued to increase significantly in June, reaching 4.8%, the highest level in the last decade. Prices in the domestic market continued to rise faster year-on-year (5.1%), while price growth in foreign markets was only slightly lower (4.6%). Compared with May, it almost doubled and was largely the result of stronger price growth of Slovenian industrial producer prices in euro area markets, while price growth in non-euro area markets was moderate. The recovery of economic activity is driving price growth of commodities (7%), which remain the largest contributor to overall growth. Price growth of investment goods is also picking up (6%). Year-on-year growth in consumer goods prices on the domestic and foreign markets also strengthened in June, reaching 1.1%, the highest level since April last year.

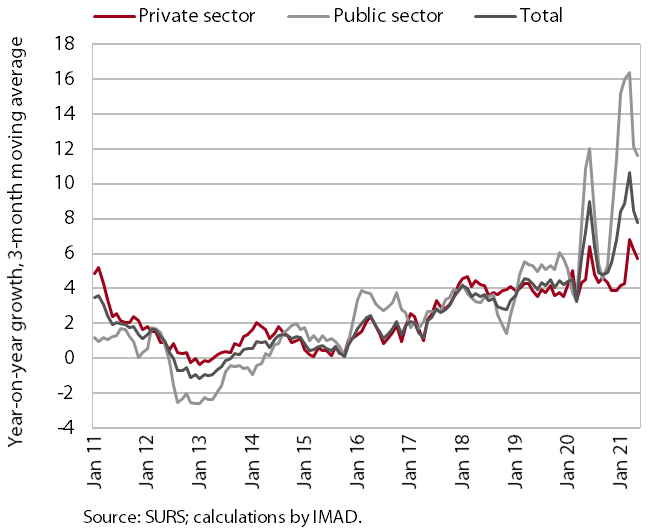

Wages, May 2021

After a moderate increase in April, year-on-year growth of average wages was relatively high again in May (6.1%), mainly in the public sector. Growth in the public sector reached 13.4% despite the already high base last year (payment of bonuses for hazardous working conditions and additional workload, as well as a bonus for work in crisis conditions in accordance with the collective agreement), due to the high level of bonuses paid in May and the resumption of payments for work performance in the middle of last year after their payment had been frozen for several years. In the private sector, average wage in May was 2.4% higher year-on-year. The relatively low year-on-year growth is related to the high growth in the same month of 2020 (base effect) caused by the payment of crisis bonuses and the methodology used to calculate wages.