Charts of the Week

Current economic trends from 19 to 23 April 2021: fiscal verification of invoices, registered unemployment, economic sentiment, traffic of electronically tolled vehicles and other charts

The renewed easing of containment measures in mid-April had a favourable impact on economic activity and confidence. Data on fiscal verification of invoices show an increase in turnover, which was only 3% lower in the third week of April than in the comparable week of the pre-crisis year 2019. With the relaxation of containment measures, confidence in trade and service activities improved slightly. Confidence in manufacturing remained high while confidence in construction improved further. In both it was higher than before the epidemic. Favourable developments in industry are also indicated by electricity consumption and freight traffic on Slovenian motorways – in the third week of April, they were similar to or higher than in the comparable week of the pre-crisis year. Unemployment also continued to fall after a slight increase in mid-April due to seasonal factors.

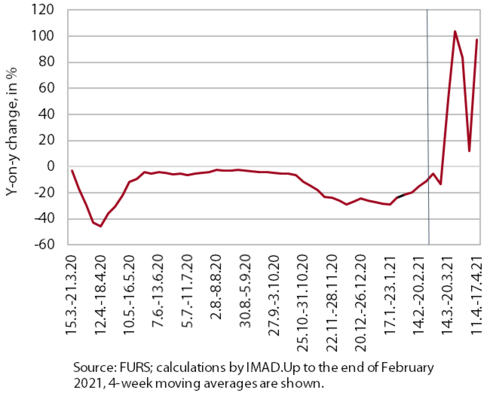

Fiscal verification of invoices, April 2021

After a downswing due to the temporary lockdown, turnover almost doubled year on year in mid-April according to data on fiscally verified invoices, and was around 3% lower than in the same period of 2019. The fall in year-on-year growth in the second week of April was mainly a consequence of the re-closure of some non-essential shops and services. To some extent, it was also attributable to the different distribution of Easter holidays and increased sales in the week before the closure of shops. With the re-opening of shops and some services, turnover growth rose strongly again in the third week of April due to the low base and was only 3% lower than in the comparable week of 2019. Strong year-on-year growth was recorded by all main trade segments (the strongest by the sale of motor vehicles) and accommodation and food service activities.

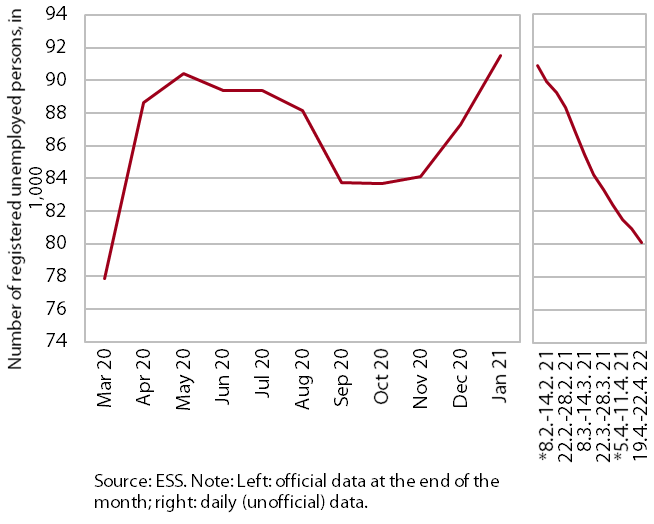

Registered unemployment, April 2021

In April, the number of registered unemployed continued to decline. Following the increases in the number of unemployed in December and January, which, due to the retention of intervention measures, did not differ much from seasonal increases in the same period of previous years, the number of unemployed dropped seasonally adjusted from February to April. On 22 April, 79,835 persons were unemployed according to ESS unofficial (daily) data, which is 3.4% less than at the end of March and around 10% less than in the same period last year.

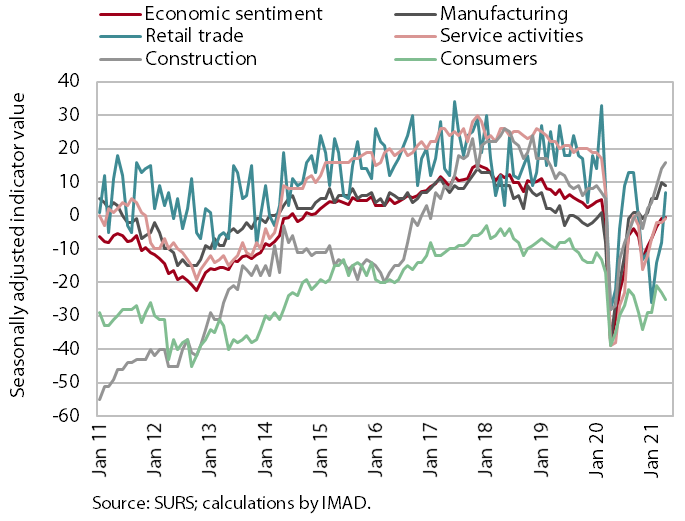

Economic sentiment, April 2021

Economic sentiment improved somewhat further in April. With the announced relaxation of some containment measures and the re-opening of public life in the middle of the month, confidence improved particularly in trade and, partly, service activities. Confidence in construction has also been rising for several months, reaching the highest level in the last two years. Confidence in the export-part of the economy did not change much in April and remained higher than before the epidemic. Consumer confidence deteriorated further and remained very low.

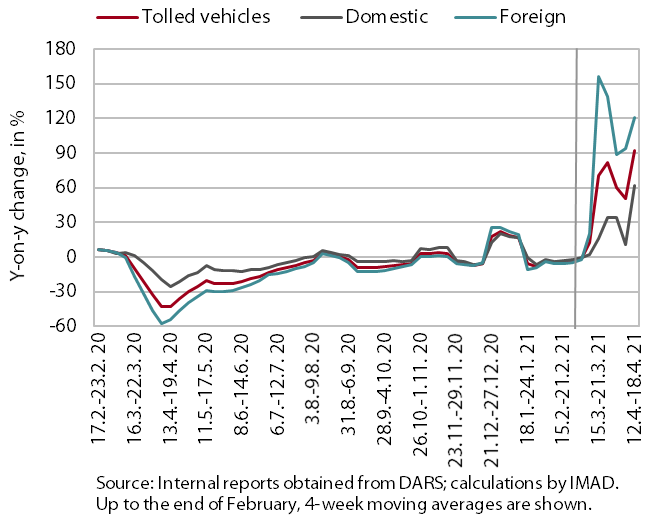

Traffic of electronically tolled vehicles on Slovenian motorways, April 2021

Freight traffic on Slovenian motorways in the third week of April was 93% higher than in the same period of last year and 9% higher than in the same period of 2019. Between 12 and 18 April, domestic vehicle traffic was 62% higher and foreign vehicle traffic 121% higher year on year. This strong year-on-year growth was mainly a consequence of the base effect, as in the same period of 2020 traffic had declined significantly due to the stringent containment measures in the first wave of the epidemic (and additionally due to one working day less due to Easter holidays). After two modest weeks due to holidays and weather conditions, freight traffic was again significantly higher in the third week of April, much higher than in the same period of the pre-crisis year 2019 (in domestic vehicles by 7%; in foreign vehicles by 11%).

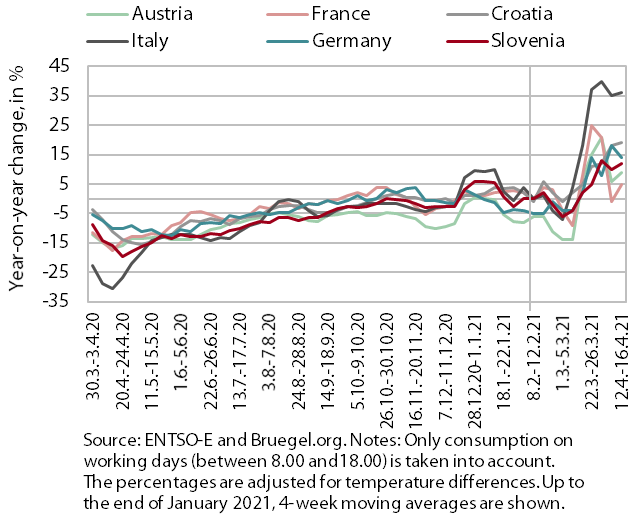

Electricity consumption, April 2021

In the week between 12 and 16 April, electricity consumption was 12% higher than in same week of 2020 and only 1% lower than in the same week of the pre-crisis year 2019. The reason for the smaller lag behind the pre-crisis level than in the previous two weeks (by around 8% on average) lies in the easing of measures after their tightening in early April, while the year-on-year increase was due to the base effect. Particularly due to the base effect, year-on-year higher consumption was also recorded in our main trading partners, from 5% in France to 36% in Italy. Compared with the same week of 2019, the largest decline in consumption was recorded in France (17%). In Austria, it was 4% and in Italy 2%. Consumption in Croatia and Germany was 3% and 5% higher respectively.

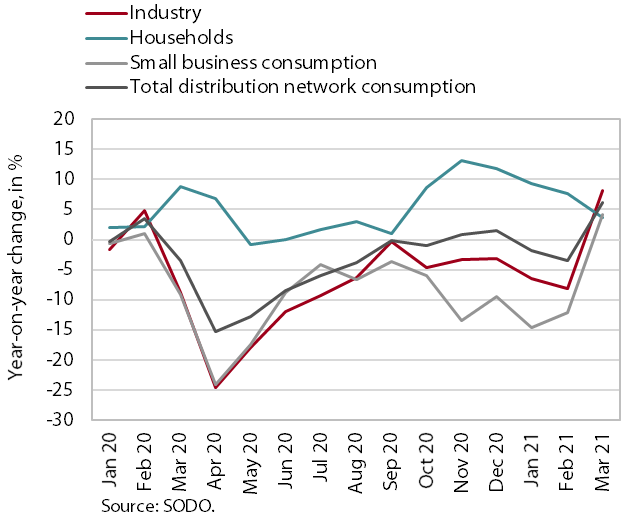

Electricity consumption by consumption group, March 2021

In March, industrial electricity consumption and small business electricity consumption were higher than in the same period of last year and not much lower than in the same period of 2019. In March, industrial electricity consumption was 8.1% and small business electricity consumption 4.1% higher year on year. The main reason was the base effect, as last year in the middle of March electricity consumption dropped notably as a result of the adoption of stringent containment measures at the beginning of the epidemic. Household electricity consumption was 3.6% higher year on year, as people spent more time at home due to the epidemic. Compared with March 2019, industrial consumption and business consumption were 1.4% and 5.3% lower, while household consumption was 12.8% higher.

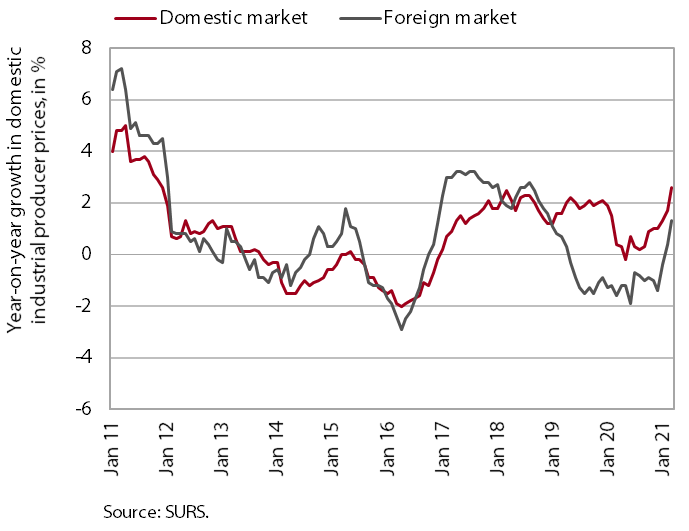

Slovenian industrial producer prices, March 2021

With stronger price rises on the domestic and foreign markets, year-on-year growth in Slovenian industrial producer prices strengthened again in March, reaching 2%. Price growth on the domestic market continues to be fuelled by price rises in the group of intermediate and capital goods. In March, energy price growth also strengthened notably. The latter is largely a consequence of the lower base, as the government temporarily exempted households and certain small business electricity consumers from paying electricity contributions during the first wave of the epidemic. The growth of consumer goods prices remains low amid more modest household consumption. Price growth on foreign markets continues to be driven particularly by higher capital goods prices. In addition, prices of intermediate goods were also up year on year in March (after almost two years of decline).