Charts of the Week

Current economic trends from 18 to 22 October 2021: turnover based on fiscal verification of invoices, economic sentiment, Slovenian industrial producer prices, wages and other

Uncertainty in the international environment and regarding the future development of the COVID-19 epidemic most likely contributed to the deterioration of the economic sentiment indicator in October as well. Nevertheless, most confidence indicators remain higher than a year ago. Turnover growth picked up slightly in the first half of October and was higher than in the same period before the epidemic. Year-on-year growth in the average wage was lower in August, reflecting a slower public sector wage growth. Employment in August was still comparable to previous months, but the number of employed persons was higher than in the same period last year. The year-on-year growth of Slovenian industrial producer prices continues to increase rapidly, with prices of intermediate goods and capital goods having the greatest impact on growth.

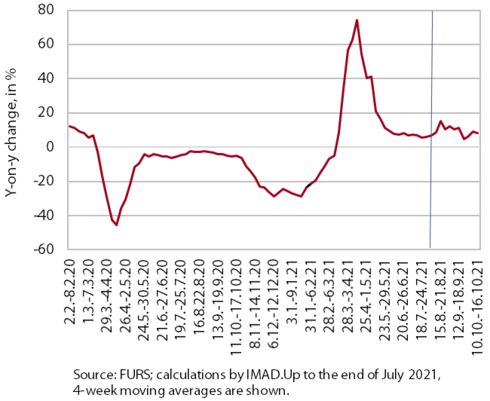

Turnover based on fiscal verification of invoices, October 2021

According to data on the fiscal verification of invoices, total turnover between 3 and 16 October was 9% higher year-on-year and 3% higher than in the same period of 2019. Growth has picked up somewhat in most activities after slowing down in the past two weeks since the introduction of the recovered/vaccinated/tested rule. The higher growth could be related to consumers adjusting to the new conditions. In trade, which represents the largest share of total turnover, it increased significantly and exceeded the 2019 level by 4%. Year-on-year growth also increased in accommodation, food and beverage service activities, travel agencies and arts, entertainment and recreation. This is due to a greater number of foreign and domestic tourists and day visitors (also due to the low turnover/low base last year) and continued redemption of vouchers. Despite the year-on-year growth, turnover in most activities with the exception of trade is still significantly below the 2019 level.

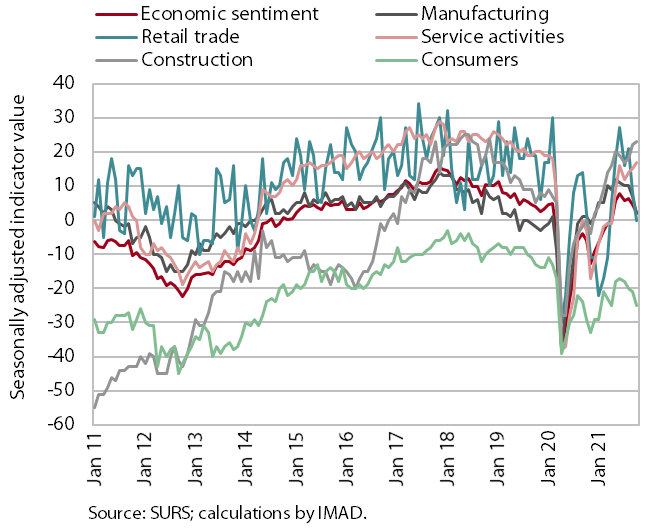

Economic sentiment, October 2021

In October, the value of the sentiment indicator deteriorated for the second month in a row. On a month-on-month basis, confidence fell in retail trade, manufacturing and among consumers. This is probably due to the still high level of uncertainty about the course of the epidemic as well as some current developments in the international environment related to supply bottlenecks and rising prices of intermediate goods and energy. The value of the confidence indicator is higher than in October last year, mainly due to significantly higher confidence in services and construction. Compared to the same period in 2019, the sentiment indicator fell slightly. It is significantly lower in the retail trade and among consumers, probably due to uncertainty about the epidemiological situation and containment measures.

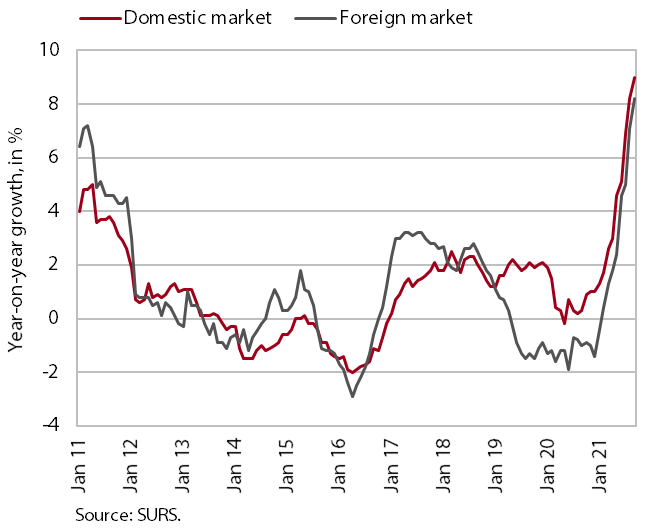

Slovenian industrial producer prices, September 2021

Slovenian industrial producer prices continue to rise rapidly year-on-year, reaching 8.6% in September. Prices in domestic and foreign markets are rising rapidly. Further growth in the prices of intermediate goods, which were 13.1% higher year-on-year, and capital goods, which were 8.2% higher, continue to contribute the most to overall growth. The year-on-year increase in energy prices remained at 8.5% but their contribution to overall growth was relatively modest due to their small share. Higher intermediate goods prices and production bottlenecks are also affecting consumer price growth, which, while still relatively moderate (1.8%), is gradually strengthening. Prices of durable and non-durable goods rose in September (by 1.6% and 1.8% respectively).

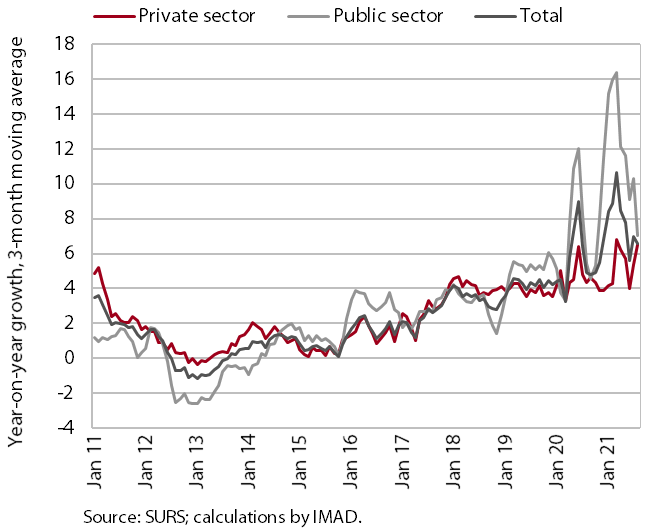

Wages, August 2021

Year-on-year wage growth in August was lower than in previous months (4.8%), especially in the public sector. Here it was 3.4% and thus significantly lower than in the previous months, when it was still influenced by the epidemic-related bonus payments. In the first eight months, wages in the private sector were 11.2% higher than in the same period last year. In the private sector, the average wage increased by 5.6% year-on-year in the first eight months due to various factors, in particular the increase in the minimum wage at the beginning of the year and, according to our estimates, also labour shortages; a new wage calculation method related to job retention intervention measures also plays a role.

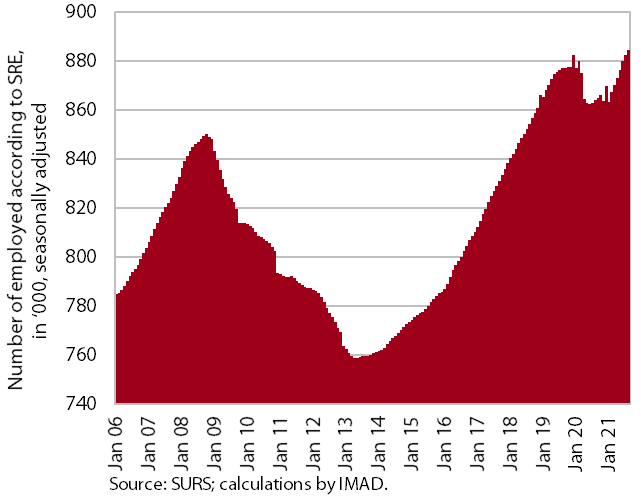

Labour market, August 2021

Employment remained at a similar level in August as in the previous two months. The number of employed persons increased by 0.7% year-on-year in the first eight months. Employment growth was higher for the self-employed (1.3%) than for employees (0.6%), although the decline in the number of self-employed last year was much smaller than for employees. In August, the highest year-on-year increases were again recorded in construction and health and social work. Employment growth was also high in the accommodation and food service activities, reflecting a relatively quick recovery after last year’s sharp decline, while the number of employed persons remained below the August 2019 level. The containment measures also had a strong impact on arts, entertainment and recreation where the number of employed people remained lower in this August than a year ago.