Charts of the Week

Current economic trends from 17 to 21 May 2021: labour market, wages, fiscal verification of invoices, traffic of electronically tolled vehicles and other charts

Labour market conditions have improved slightly in recent months but remain remain tight. Unemployment declined somewhat between February and mid-May due to seasonal factors and the easing of containment measures but remained higher than before the epidemic. In March, the number of employed persons was similar to that in the previous few months. Year-on-year wage growth in the first quarter was high, mainly owing to the payment of crisis bonuses in the public sector. Current data on economic activity show higher freight traffic on Slovenian motorways in the first half of May than in the same period before the epidemic, while electricity consumption was still slightly lower. According to data on fiscally verified invoices for this period, turnover in trade was also higher than before the epidemic, while turnover in services where strict restrictions on activity still apply remained significantly lower. Slovenian industrial producer prices are rising, driven particularly by higher prices of intermediate goods.

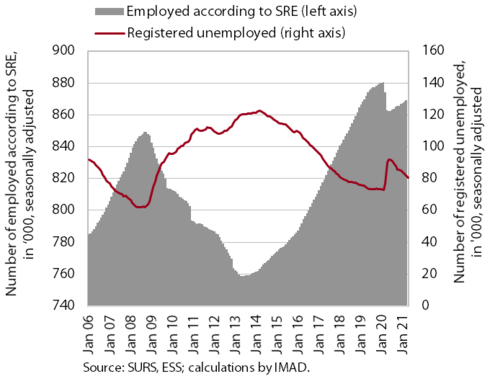

Labour market, May 2021

In May, the number of registered unemployed continued to decline. In addition to seasonal impacts, which did not deviate significantly from those in the period before the epidemic, the decline is also related to the gradual relaxation of containment measures. On 20 May, 76,074 persons were unemployed according to ESS unofficial (daily) data, which is 4% less than at the end of April and around 16% less than in the same period of last year. Compared with May 2019, the number was, however, around 6% higher. The number of employed persons was 0.5% lower year on year in March, which is less than in previous months, mainly due to the base effect (a sharp fall in March 2020 due to the outbreak of the epidemic. The year-on-year decline was again largest in accommodation and food service activities and administrative and support service activities, i.e. activities that were hit hardest by containment measures, while the largest increase was in health and social work.

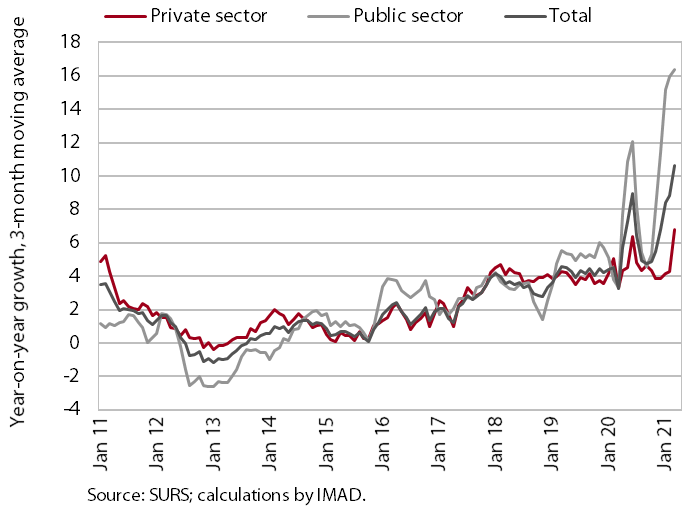

Wages, March 2021

In the first quarter of this year, wages rose year on year, which was mainly related to the payment of crisis bonuses in the public sector. With the renewed payment of allowances (the extraordinary payment of allowances for hazardous working conditions and additional workload and the payment of the bonus for work in crisis conditions in accordance with the collective agreement), year-on-year wage growth in the public sector increased again towards the end of last year and in the first quarter of this year, by far the most in social work and health (in March, it was 31.3%; in the entire public sector, 16%). Year-on-year wage growth in the private sector was lower in the second wave of the epidemic than in the first mainly owing to the payment of allowances in the first wave. The strong year-on-year increase in March of this year was a consequence of the base effect (a decline in wages in March 2020, when a state of epidemic was declared).

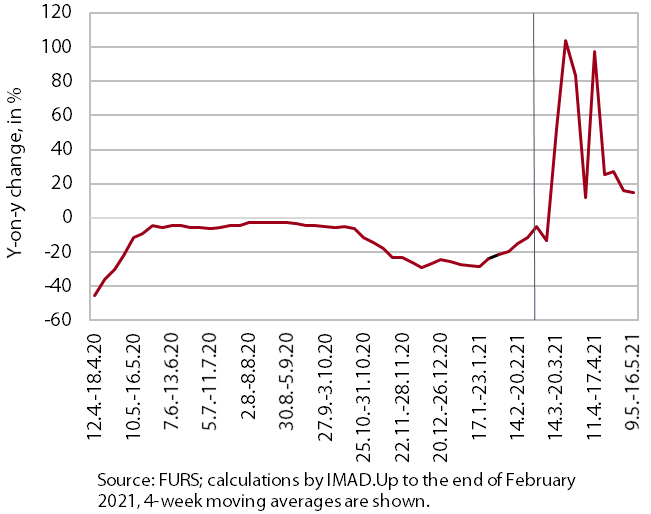

Fiscal verification of invoices, May 2021

According to data on fiscally verified invoices, in the first half of May turnover was 16% higher year on year and 9% higher than in the same period of 2019. Year-on-year growth in turnover moderated in those sectors where last year containment measures were already considerably relaxed in the first half of May (e.g. most shops and establishments serving food and beverages), or turnover even fell year on year in those which saw a significant increase in sales with the renewed opening last year (for example some personal services). In others, for example accommodation and travel agency activities, which were allowed to partially reopen, turnover more than tripled this year. Total turnover in the first half of May was 9% higher than in the same period of 2019, which was mainly a consequence of high growth in all three trade segments. Turnover in services where strict restrictions on activity are still in place (cultural, recreational, sports, personal and food service activities and travel agencies), however, was significantly smaller.

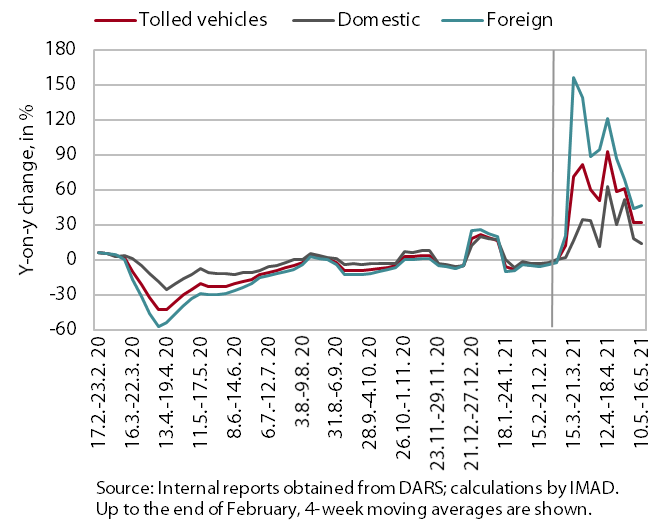

Traffic of electronically tolled vehicles on Slovenian motorways, May 2021

Freight traffic on Slovenian motorways in the second week of May was 32% higher than in the same period of last year and 1% higher than in the same period of 2019. The volume of freight traffic in the second week of May was again relatively high and somewhat higher than in the same week of the pre-crisis year 2019 (in domestic vehicles the same and in foreign vehicles 2% higher). Between 10 and 16 May, domestic vehicle traffic was 13% higher and foreign vehicle traffic 47% higher year on year. This strong year-on-year growth is still mainly a consequence of lower traffic in the same period of last year in the first wave of the epidemic (when freight traffic of foreign vehicles declined more).

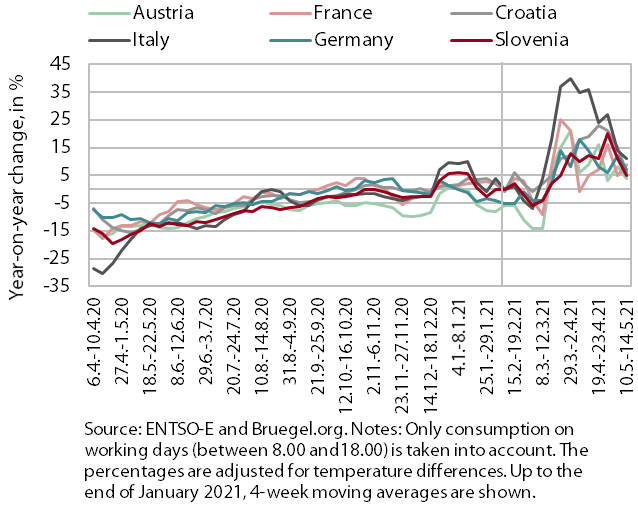

Electricity consumption, May 2021

Electricity consumption in the second week of May was 5% higher compared with the same week of 2020 but 5% lower compared with the same week of the pre-crisis year 2019. The reason for the year-on-year higher consumption in the week between 10 and 14 May was last year’s low base. However, consumption remained lower than before the crisis despite the relaxation of a number of containment measures. Particularly due to the base effect, year-on-year higher consumption was also recorded in Slovenia’s main trading partners, from 4% in Austria to 11% in Italy. Relative to the same week of 2019, consumption was down in most trading partners (in France by 10%, Croatia by 7%, and in Austria, Italy and Germany by around 3%).

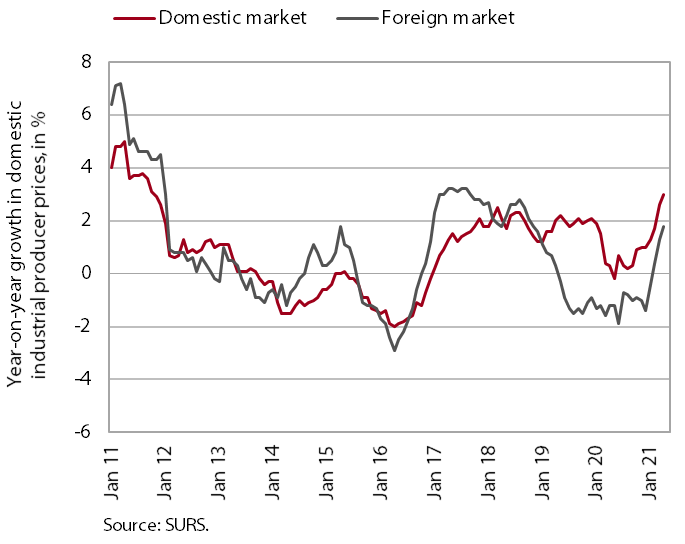

Slovenian industrial producer prices, April 2021

Year-in-year growth in Slovenian industrial producer prices rose to 2.4% in April. Price growth on the domestic market continues to be fuelled by price rises in the group of intermediate and capital goods and energy. Energy price growth is entirely a consequence of the lower base, as the government temporarily exempted households and certain small business consumers from paying electricity contributions in the first wave of the epidemic. Otherwise, energy prices even fell in the first four months of this year compared with December 2020. Year-on-year growth on foreign markets continues to be driven particularly by higher prices of capital and intermediate goods. Year-on-year growth in consumer goods prices on the domestic and foreign markets together remains modest (0.1%).