Charts of the Week

Current economic trends from 14 to 18 October 2019: labour market, wages, construction and current account of the balance of payments

Further employment growth is mainly a consequence of the hiring of foreigners amid a slower decline in the number of unemployed persons. Year-on-year wage growth remains higher than one year ago. Activity in construction has decreased in recent months, but the indicators of expectations indicate a renewed strengthening in the coming months.

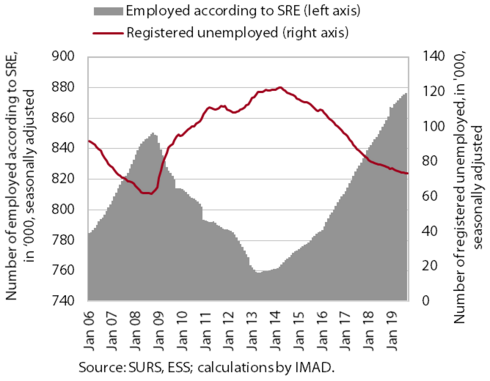

Labour market, August–September 2019

Employment growth remains fairly high mainly due to the hiring of foreigners. In the first eight months, the number of employed persons was up 2.8% year on year, somewhat less than in the same period of 2018 (3.2%), which reflects lower growth in economic activity, low unemployment and a greater shortage of (appropriate) workforce. The strongest growth in this period was recorded in construction and transportation and storage, the sectors with the largest shares of foreign labour. The fall in the number of registered unemployed persons also slowed in the middle of the year. In total, 68,834 persons were registered as unemployed at the end of September, which is 5.3% less than one year before.

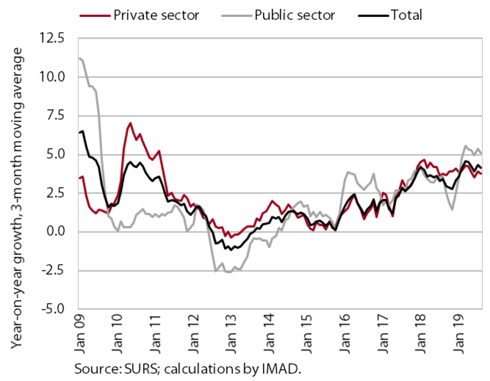

Wages, August 2019

Year-on-year wage growth in the first eight months (4.3%) was higher than in the same period of last year (3.6%). Wages increased the most in the general government sector, reflecting the agreed wage rises at the end of last year, promotions and, to a lesser extent, the increase in the minimum wage. The increase in the minimum wage at the beginning of the year, amid the still strong GDP growth and labour shortages, was also reflected in wage growth in the private sector. Wages rose the most in administrative and support service activities, accommodation and food service activities, and trade, i.e. sectors marked with the greatest labour shortages and a large share of minimum wage recipients.

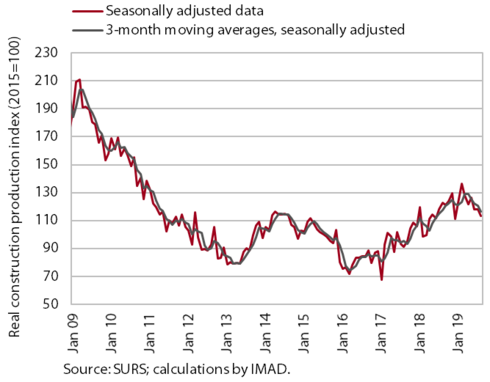

Construction, August 2019

In August the value of construction output fell for the third consecutive month. Activity was 7.5% lower year on year, which is also related to last year’s strong base. After strong growth early in the year, which was also partly due to favourable weather conditions, the value of construction output fell in the middle of the year. The largest decline was recorded in non-residential buildings, which is related to deteriorated expectations of the business sector and its investment activity. The slowdown in the construction of civil-engineering works was more moderate, while activity in the construction of residential buildings increased, however, with significant monthly fluctuations. The indicators of the stock of contracts and new contracts in construction had fallen towards the end of last year, but in the middle of the year their values were higher than in the same period of last year. Similarly, the indicators of business trends in construction have stabilised this year, after dropping in 2018. These data indicate that construction activity is set to strengthen again.

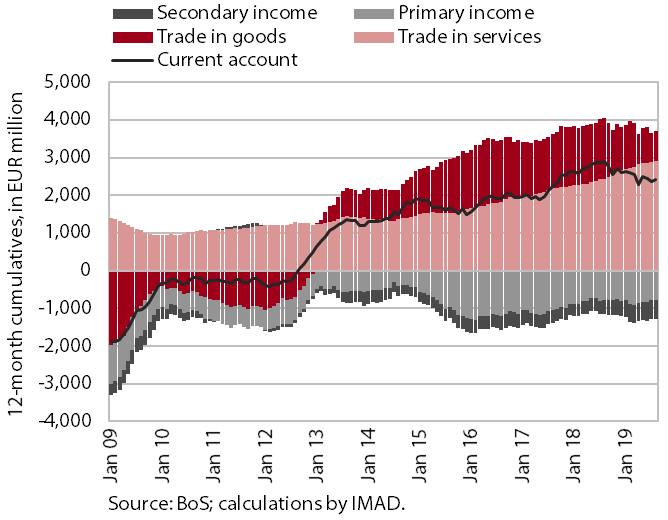

Current account of the balance of payments, August 2019

The current account surplus totalled EUR 2.4 billion (5.0% of estimated GDP) in the 12 months to August and was lower year on year. The main reason for the year-on-year decline was the lower surplus in trade in goods, which was largely due to volume factors. Real growth of imports was faster than that of exports. The terms of trade deteriorated as well. The deficit in secondary income was also up year on year, primarily on account of higher VAT- and GNI-based contributions to the EU budget. On the other hand, the surplus in services trade was significantly higher than last year. The net outflows of primary income were lower, largely owing to lower costs of external debt servicing.