Charts of the Week

Current economic trends from 14 to 18 March 2022: labour market, current account and electricity consumption by consumption group

Labour market conditions continued to be favourable in January, with employment growth increasing slightly year-on-year. It was strongest in accommodation and food service activities and in construction. Due to the shortage of domestic labour, the employment of foreign workers is increasing, with the highest numbers in January in construction and transportation and storage. The current account surplus fell again in January. This is mainly due to a decline in the surplus in goods trade related to the rising prices of energy and other primary commodities. Industrial electricity consumption and small business electricity consumption were higher year-on-year in February and lower than in February 2020, most likely due to supply chain problems and shortages of raw materials, which put a constraint on business operations.

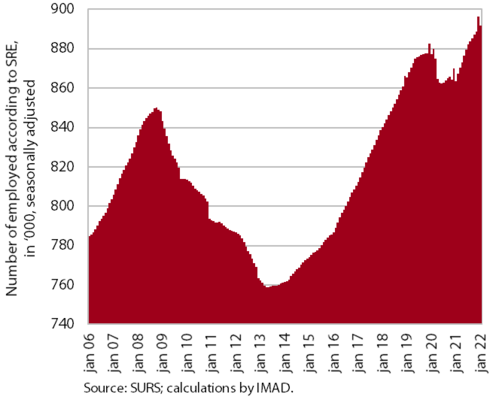

Labour market, January 2022

Employment fell slightly in January compared to the previous month (-0.7%), mainly due to seasonal trends; year-on-year growth strengthened slightly (3.3%). It was strongest in accommodation and food service activities and in construction. Employment in the latter was significantly higher than before the epidemic, while employment in the former remained slightly below the level of two years ago. Amid strong economic recovery, employment growth still depended largely on the hiring of foreign workers, whose contribution to overall growth in January was almost 50% year-on-year. The high share of foreign workers is also related to the shortage of domestic labour, which is the most pronounced in construction and administrative and support service activities (both having a high job vacancy rate). The economic sectors with the highest share of employed foreign workers in January were construction (45%), transportation and storage (31%), and administrative and support service activities (24%).

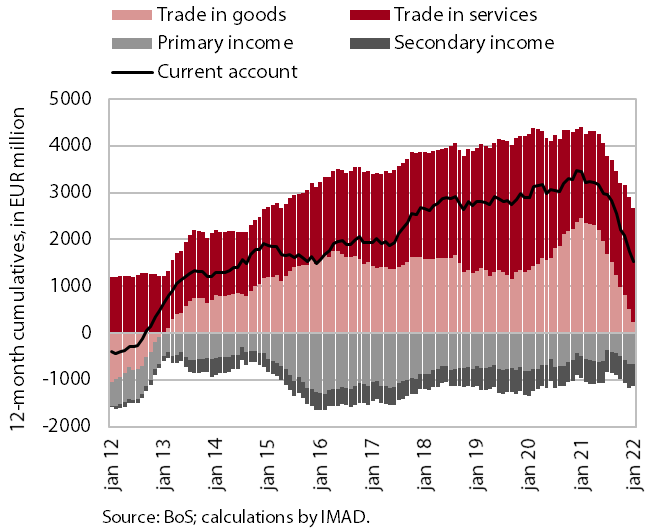

Current account, January 2022

The current account surplus fell again in January, mainly due to a decline in the surplus in goods trade. Over the past 12 months, the current account surplus totalled EUR 1.5 billion (2.7% of estimated GDP). The lower year-on-year surplus was mainly a result of a lower surplus in trade in goods, which is related to the rising prices of energy and other primary commodities, which have the largest impact on the price increase of imported products. The deficits in primary and secondary income were up year-on-year. Net outflows of primary income were higher year-on-year, mainly due to higher payments of dividends and profits to foreign investors, while net outflows of secondary income were higher mainly due to higher VAT- and GNI-based contributions to the EU budget. The surplus in services trade continued to increase, especially in trade in travel and other business services.

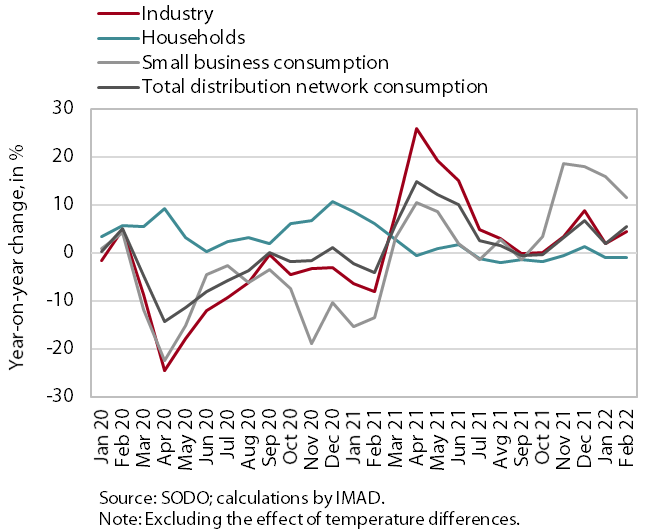

Electricity consumption by consumption group, February 2022

Industrial electricity consumption and small business electricity consumption were higher year-on-year in February, while the gap with the same period of 2020 was similar as in January. Industrial electricity consumption was 4.4% higher year-on-year in February and small business electricity consumption was 11.6% higher due to the low base last year. Household consumption was slightly lower year-on-year in February (-1.1%). Compared to February 2020, small business consumption was 3.4% lower and industrial consumption was 4.1% lower. This could be related to supply problems and a shortage of raw materials, which, according to the survey data, remains one of main factors limiting business activity. Household consumption was also higher in February than in the same period of 2020 (4.8%), but the surplus was lower than in the previous month (7.4%) due to the improved epidemiological situation.