Charts of the Week

Current economic trends from 13 to 17 September 2021: electricity consumption by consumption group, construction, labour market and current account of the balance of payments

Some economic indicators point to a slowdown in growth during the summer months. Electricity consumption growth has slowed in recent months. This is mainly due to industrial consumption lagging behind pre-epidemic levels due to disruptions in material supply and lower production. Construction activity declined in July, with a particularly unfavourable trend in non-residential construction. Employment remained relatively high in July, with the largest year-on-year increases in health care and social work and in construction. The current account surplus also remains high.

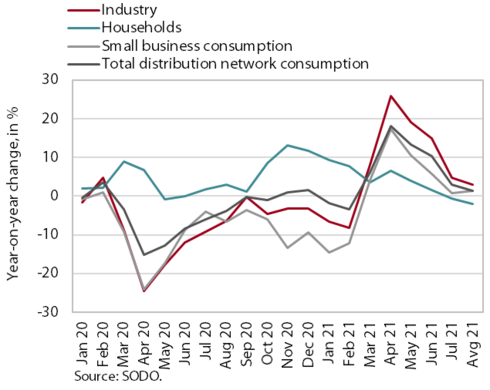

Electricity consumption by consumption group, August 2021

August was the second consecutive month in which industrial electricity consumption was lower than the same period in 2019, while small business electricity consumption has lagged behind 2019 levels since the epidemic began. Industrial consumption fell by 3.4% (by 4.9% in July), which we believe is related to supply constraints and high material prices, and consequently lower production. Small business electricity consumption was 5.3% lower (3.3% lower in July), while household consumption was 0.8% higher. Compared to August last year, industrial electricity consumption was 3.1% higher and small business electricity consumption was 1.4% higher. Household consumption was 2.1% lower, which may indicate that more households decided to go on holiday than last year.

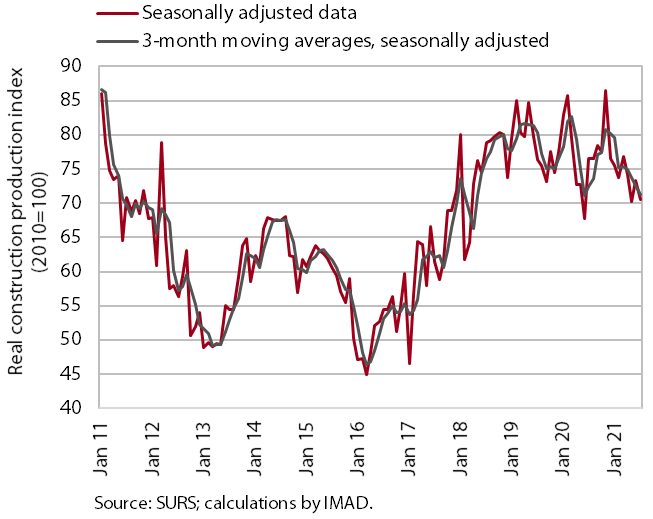

Construction, July 2021

Construction activity declined in July. The value of construction output fell by 3.9% and was 8.0% lower than a year earlier. At the monthly level, activity in individual construction segments is highly volatile. Amid these fluctuations, activity in residential buildings, civil engineering and specialised construction remains at the level reached at the beginning of the year, while it declined sharply in non-residential construction. Data on the number of contracts suggest that activity in non-residential construction will remain relatively low, while other segments, particularly civil-engineering and specialised construction activities, are expected to perform better.

Construction prices have risen significantly under the pressure of rising commodity prices (and labour shortages). The implicit deflator of the value of completed construction works (used to measure prices in the construction sector) was 7% in July, its highest level since 2005.

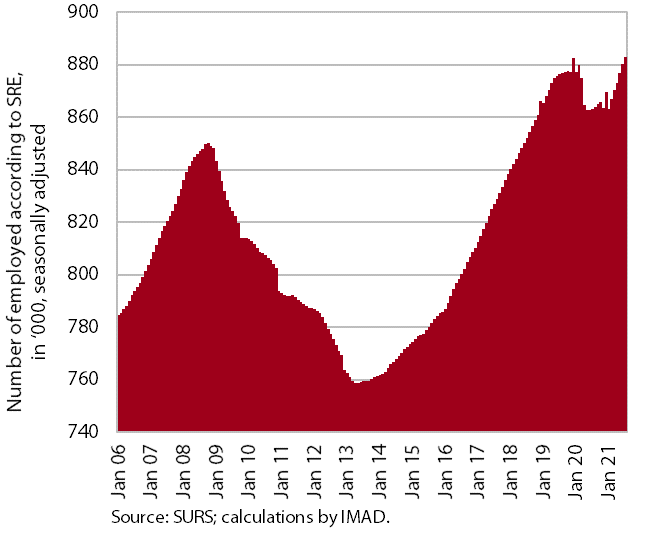

Labour market, July 2021

Employment remained at a similar level to the previous month, but year-on-year growth strengthened due to the base effect. The number of employed persons was up 2.3% year-on-year in July, mainly due to a sharp decline in the spring months of last year. Year-on-year growth was similar for both employees (2.2%) and the self-employed (2.1%), although the decline in the number of self-employed last year was much smaller than for employees. The highest year-on-year increases were observed in health and social work and in construction. For the first time since the outbreak of the epidemic, employment also rose year-on-year in the accommodation and food service activities in July. Year-on-year, employment was lower only in arts, entertainment and recreation, the sectors severely affected by the containment measures.

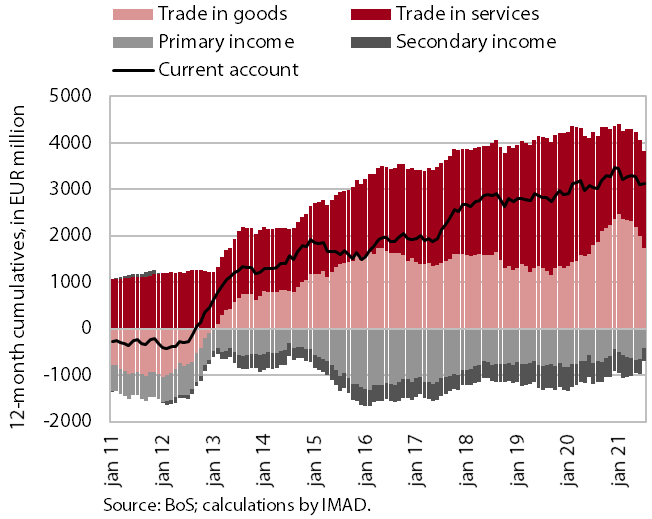

Current account of the balance of payments, July 2021

The current account surplus remained high in July. It totalled EUR 3.1 billion (6.5% of estimated GDP) in the last 12 months. In comparison with the same period a year before, the higher surplus arose mainly from lower primary income deficit, lower net payments of interest on external debt and lower net payments of income on equity. The deficit in secondary income was lower as the government received more funds from European Social Fund. Despite the recovery in trade in services, the surplus in trade in services is still lower year-on-year, mainly due to a lower surplus in travel. The current account surplus narrowed, due to higher prices of energy and other primary commodities, which have the largest impact on import price growth. Export prices rose by 0.9% year-on-year, and import prices rose by 2.0% and the terms of merchandise trade deteriorated by 1.1%.