Charts of the Week

Current economic trends from 13 to 17 December 2021: turnover based on fiscal verification of invoices, construction, labour market and other data

Turnover based on fiscal verification of invoices was up 41% year-on-year in early December, mainly due to growth in activities that were almost completely shut down during the same period last year. The high growth in trade also continued. Total turnover was similar to the same period in 2019. Activity in construction, which has fluctuated widely across segments in recent months, declined significantly in October. Price growth in construction remained high, mainly due to rising commodity prices and labour shortages. Employment, which had reached historically high levels, increased further in October. The highest year-on-year increases were recorded in accommodation and food service activities and in construction, which, given the low unemployment rate, is mainly due to the hiring of foreigners. The current account surplus remains quite high, but has narrowed in recent months, mainly due to the sharp increase in import prices for goods and the recovery of domestic demand.

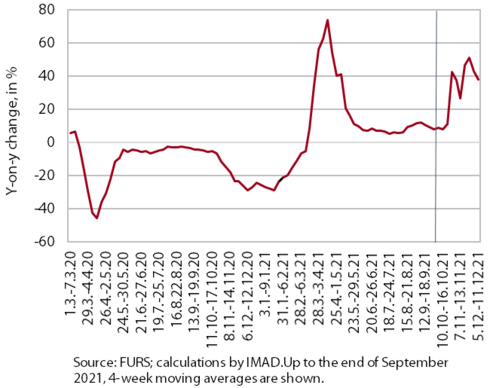

Turnover based on fiscal verification of invoices, December 2021

According to data on fiscal verification of invoices, total turnover between 28 November and 11 December was 41% higher year-on-year and similar to that in the same period of 2019. Year-on-year growth in most activities was slightly lower than in the previous two weeks, but still high, mainly due to last year's low turnover. Very strong growth was recorded mainly in activities that were almost completely shut down in the same period last year, and turnover in trade was also one third higher. After exceeding the 2019 level in recent weeks, overall turnover was similar to the same period in 2019, mainly due to lower growth in trade, which is related to the timing of "Black Friday". Due to the poor epidemic situation and the introduction of stricter business restrictions as well as the announced extension of the deadlines for the redemption of vouchers, decline in turnover in the accommodation and food service activities, arts, entertainment and recreation, travel agency activities, and gambling and betting activities deepened compared to 2019.

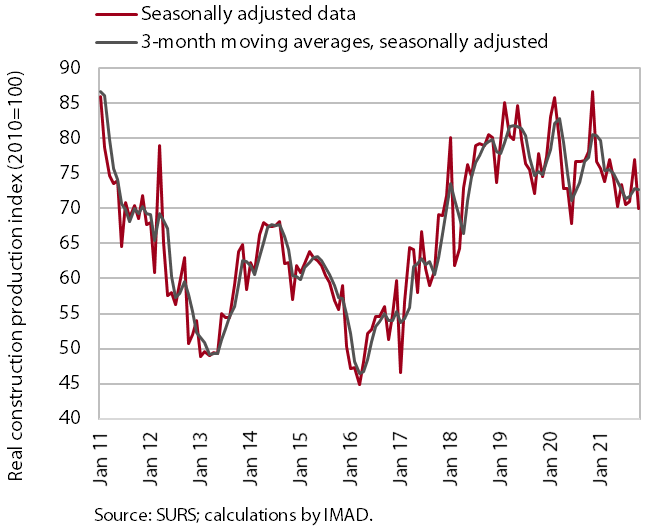

Construction, October 2021

Fluctuations in construction activity continued in October. After an increase in September, the value of construction output fell by 9.2% in October and was 10.7% lower than in October last year. At the monthly level, activity in the individual construction segments fluctuates strongly. Despite these fluctuations, civil engineering works and specialised construction remains at the levels reached at the beginning of the year. It is declining in residential construction and especially in non-residential construction. The stock of contracts also fluctuates similarly on a monthly basis. It peaked in July, but after a sharp decline in August, it has risen again slightly in the last two months.

Construction prices increased sharply in the last year under the pressure of rising commodity prices and shortage of labour. The implicit deflator of the value of completed construction works (used to measure prices in the construction sector) was 7.6% in October and over 10% in building construction.

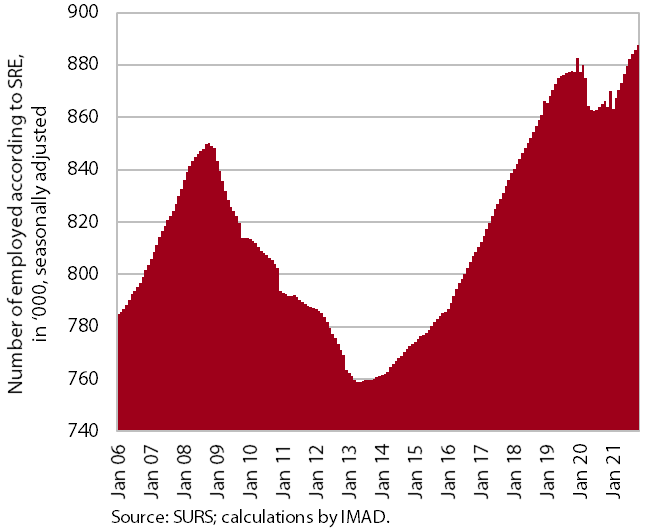

Labour market, October 2021

Employment rose further in October, reaching its highest level measured to date. The highest year-on-year increases were recorded in accommodation and food service activities and construction, with employment in the latter significantly higher than in October 2019, while employment in the former remained below the level of two years ago. The containment measures also had a strong impact on the arts, entertainment and recreation where the number of employed people also remained lower this October than in the same period of 2019. In the first ten months, the number of employed persons was 1.1% higher than last year and 0.4% higher than in the same period of 2019. In the midst of a rapid economic recovery, employment growth continues to be largely driven by the hiring of foreigners (their contribution to total employment growth exceeding 50% in October), as was the case before the outbreak of the COVID-19 epidemic. This is a consequence of demographic change and the related shortage of domestic labour. The economic sectors with the highest share of employed foreigners in the first ten months were construction (43%), transportation and storage (31%), administrative and support service activities (24%) and accommodation and food service activities (15%).

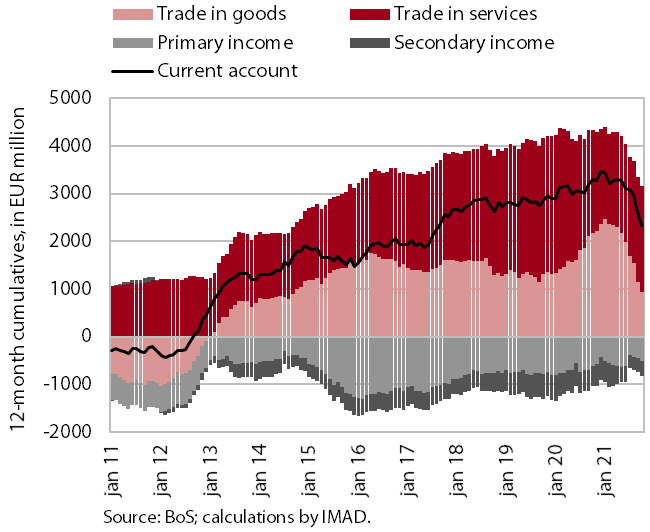

Current account of the balance of payments, October 2021

The current account surplus fell again in October. In the last twelve months, it amounted to EUR 2.3 billion (4.6 % of GDP), which was lower than in the previous year. The lower year-on-year surplus is entirely due to a lower trade surplus, as the real growth of imports was higher than that of exports. The terms of trade also deteriorated. As the increase in import prices (7.5%) was higher than that of export prices (3.1%), the operating costs of Slovenian exporters increased. The surplus in services trade continued to increase, especially in trade in construction services and trade in higher value-added services (research and development services and telecommunications, computer and information services). The primary income deficit decreased year-on-year, mainly due to higher subsidies from the EU budget for the agricultural and fisheries policies and lower costs of external debt servicing. The lower deficit in secondary income is mainly due to higher government sector receipts from the European Social Fund and ongoing international cooperation.