Charts of the Week

Current economic trends from 12 to 15 January 2021: registered unemployment, electricity consumption, electricity consumption by consumption group, traffic of electronically tolled vehicles and other charts

The containment measures implemented during the second wave of the epidemic have a negative impact particularly on service activities, but, unlike during the first wave, they have no major impact on activity in industry and construction. According to data on the fiscal verification of invoices, turnover in service activities fell strongly year on year in the last quarter of 2020, albeit less than in the spring. The smaller impact on industry is also indicated by electricity consumption, which was similar year on year in December, as was freight traffic on Slovenian motorways. Construction activity in November was even considerably higher than a year earlier. After December’s growth, which was not significantly different from seasonal increases of previous years, the number of unemployed increased further in the first half of January. As a result of the payment of allowances, the year-on-year growth of the average gross wage strengthened in November.

Registered unemployment, January 2021

The number of registered unemployed persons increased further by mid-January. Following a pronounced increase during the first wave of the epidemic, the number of registered unemployed persons has been gradually falling since mid-year after the adoption of intervention job retention measures and the lifting of restrictions. Between September and November, it remained roughly unchanged, before starting to rise moderately in December. Growth also continued at the beginning of this year – on 14 January, 91,000 persons were unemployed according to ESS unofficial (daily) data, which is 4.3% more than at the end of December and around 14% more than in the same period last year. Amid the retention of intervention measures, the December increase in the number of unemployed was not much different from increases at the end of previous years, which had mostly been a consequence of seasonal factors. In the first half of January, the number of unemployed persons rose further.

Electricity consumption, January 2021

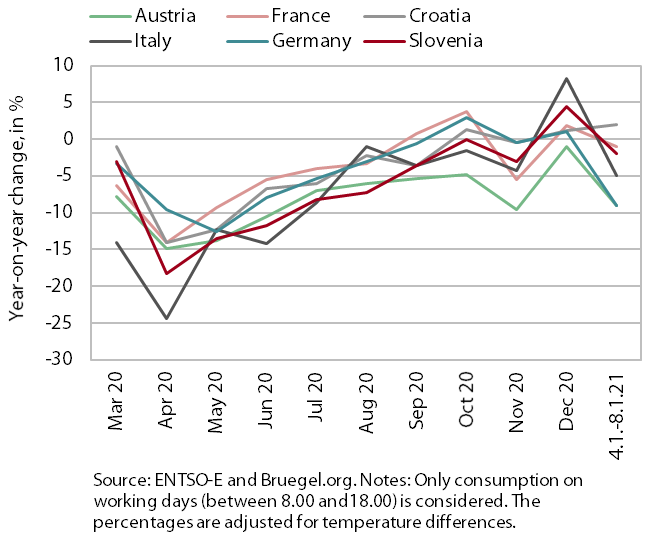

At the beginning of January, electricity consumption was only slightly lower than in the same period last year. Between 4 and 8 January, electricity consumption was 2% lower than a year earlier. Among Slovenia’s main trading partners, the year-on-year decline in consumption was largest in Austria and Germany (around 9%), due to the strict containment measures in both countries. In Italy, the decline was somewhat smaller (5%). Electricity consumption in France was roughly the same as last year, while in Croatia it was 2% higher.

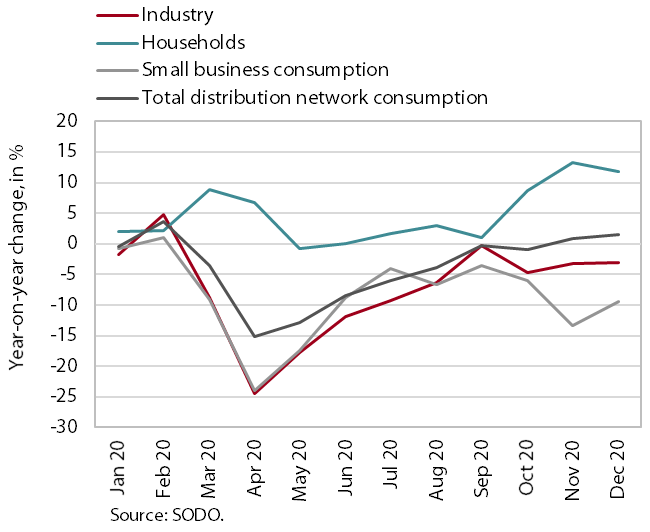

Electricity consumption by consumption group, December 2020

Electricity consumption in December was similar to the same period last year, as, unlike during the first wave of the epidemic, the containment measures had no visible impact on consumption by industry, the largest consumer. Industrial electricity consumption in December was, as in the previous two months, 3.1% lower year on year (in contrast to 18% in the second quarter). After increasing in November, the year-on-year decline in electricity consumption by small business consumers, which also include trade and services, decreased somewhat in December (9.4%). The same decline was recorded for the last quarter as a whole (in the second quarter, 16.8%). On the other hand, household electricity consumption was 11.7% higher year on year in December, as people spent more time at home more due to the epidemic.

Traffic of electronically tolled vehicles on Slovenian motorways, January 2021

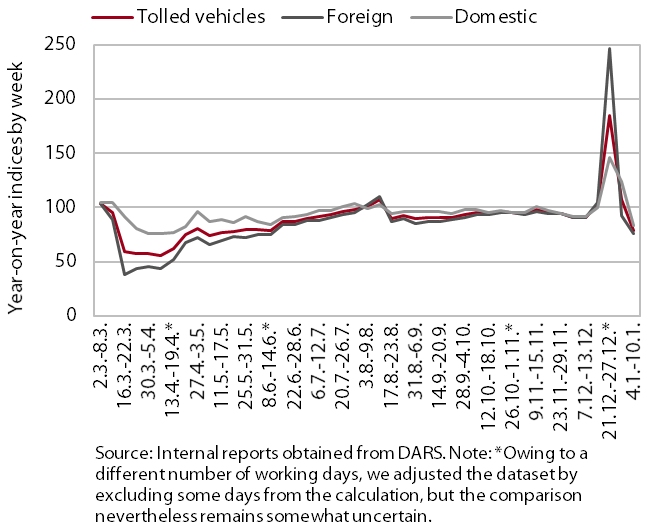

Freight traffic on Slovenian motorways at the beginning of 2021 was lower year on year. Between 4 and 10 January, freight traffic was 22% lower year on year – domestic vehicle traffic by 17% and foreign vehicle traffic by 25%. The lower volume of traffic than in the equivalent week of 2020 is mainly related to a less favourable distribution of public holidays in neighbouring countries and the abundance of snow in some parts in Italy and Austria this year.

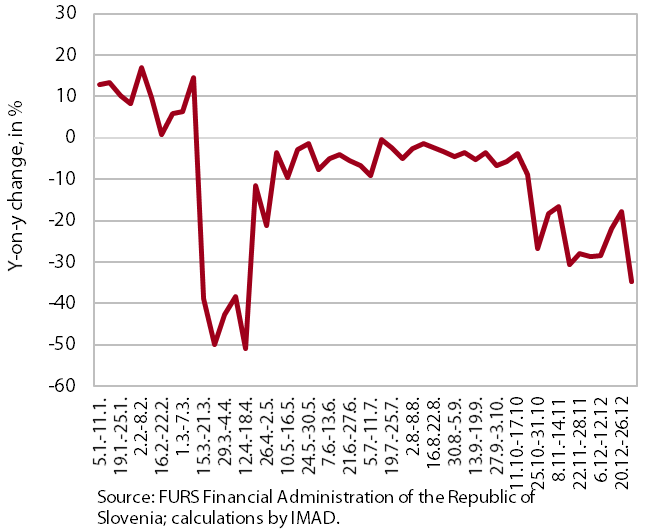

Fiscal verification of invoices, December 2020

According to data on the fiscal verification of invoices, the decline in turnover decreased in the middle of December, before increasing again towards the end of the year. In the second half of November and at the beginning of December, turnover was around 30% lower than in the same period of 2019. Before Christmas, the fall was smaller due to the opening of some shops and activities, only to increase again in the last week of December. The fall seen at the end of the year was thus the largest in the whole period of the second wave of the epidemic, albeit markedly smaller than the largest decline during the first wave. The deepening of the fall towards the end of the year was significantly impacted by a decline in turnover in the sale and repair of motor vehicles. The structural effect of accommodation activities was also significant. With a roughly the same year-on-year decline as in previous weeks, these made a larger contribution to the the overall decline in turnover towards the end of the year, as in previous years the season was at its peak during this period.

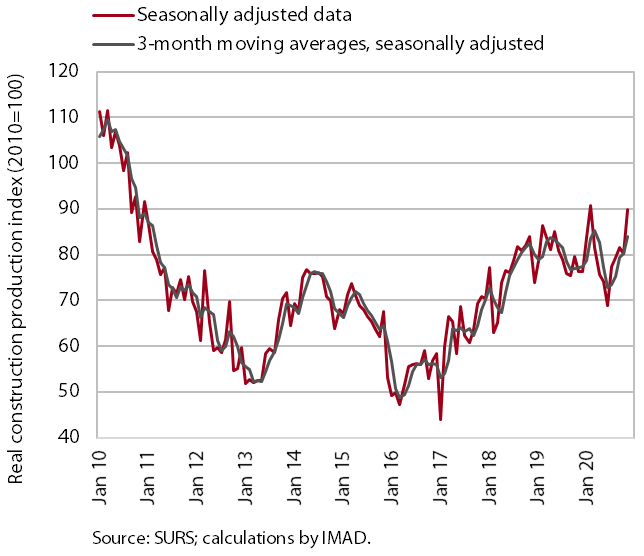

The value of construction put in place, November 2020

Construction activity strengthened significantly in November. The value of construction output increased by 12.2% and was 18.4% higher than a year before. Compared with 2018 and 2019, in the last few months of last year, construction activity was significantly lower in non-residential buildings, slightly higher in civil-engineering works and considerably higher in residential buildings (where data for the last months are less reliable).

Short-term prospects remain favourable for civil-engineering works and residential buildings, while they look worse for the construction of non-residential buildings. The stock of contracts in the construction of civil-engineering works increased by 15% year on year, while in the construction of non-residential buildings, it declined by 28%. The number of issued permits for the construction of new flats, which had declined in the first half of 2020, increased again in the summer and autumn.

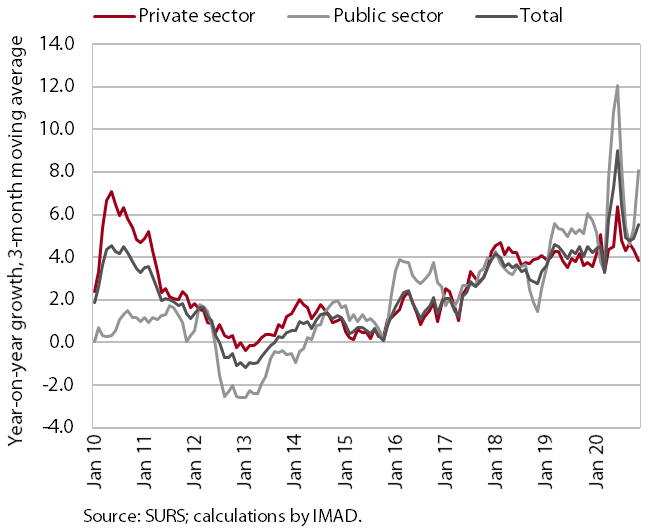

Wages, November 2020

Since the spring months, the year-on-year growth of the average gross wage (6.9% in November) has been significantly affected by the payment of crisis allowances and the inclusion of employed persons into intervention job retention schemes. In the private sector, growth has slowed considerably since April, when it increased significantly due to the impact of the methodology for the collection of earning statistics, which reflected the placement of a large number of people on temporary layoff. In the public sector, wage growth slowed in the middle of the year after the discontinuation of allowances (the extraordinary payment of allowances for hazardous working conditions and additional workloads and the payment of the bonus for work in crisis conditions in accordance with the collective agreement). Since mid-October, when the second wave of the epidemic was declared, it has strengthened somewhat due to the renewed payment of allowances in November, albeit somewhat less than during the first wave. The increase of wages in social work and health stood out in particular (the payment of allowances). The payments of Christmas bonuses in the private sector, which have a significant impact on November’s increase in the average wage, were similar to November 2019.

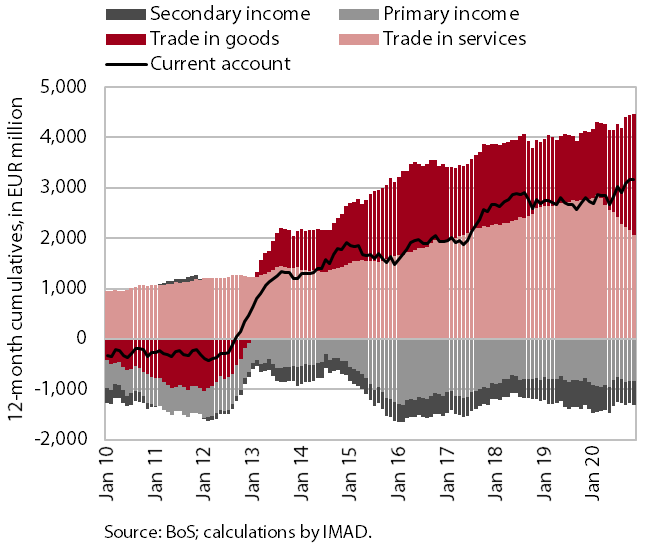

The balance of payments, November 2020

The current account surplus remained high; it mostly reflected the movements in trade in goods and services. The year-on-year higher surplus, which amounted to EUR 3.2 billion in the last twelve months to November (6.9% of estimated GDP), was, amid the improved terms of trade, mainly due to a higher surplus in trade in goods. The surplus in services trade declined further, mostly due to a fall in the surplus in travel and transport services. The surplus in services with higher value added (telecommunications, computer and information services) and, amid rising re-exports of medicinal and pharmaceutical products, the surplus in processing services (packaging, assembly and labelling) increased. The current account surplus also strengthened year on year as a result of net outflows of secondary income, which declined mainly due to lower payments of taxes and contributions abroad and lower VAT- and GNI-based contributions to the EU budget. Net outflows of primary income were higher year on year due to a higher net outflow of income on equity and debt. In addition, the net inflow of labour income was lower, as income of daily migrants working abroad declined more than income of foreign workers in Slovenia.

Road and rail freight transport – Q3 2020

The volume of road freight transport increased significantly in the third quarter of 2020 after the removal of containment measures; fluctuations in rail transport, which has been declining for quite a while, were insignificant. Slovenian hauliers carry out a large part of their journeys abroad. Road transport abroad declined significantly in the first half of last year as a result of strict containment measures in the majority of EU countries. With the relaxation of measures, it rose again and was 5% smaller in the third quarter than a year earlier. The volume of road transport at least partially connected to the Slovenian territory (exports, imports and national transport combined) decreased less during the first wave of the epidemic, but it also recovered more slowly than transport abroad and was 8% smaller in the third quarter than in the same period of 2019. The containment measures had a smaller impact on freight transport by rail, but this had already been declining for several quarters before the epidemic (in the third quarter, it was 13% lower year on year).