Charts of the Week

Current economic trends from 11 to 15 November 2019: current account of the balance of payments, wages and construction

The current account surplus declined in the last twelve-month period amid moderating growth in the international environment. The growth of wages is higher than last year, mainly owing to higher wage growth in the general government sector, but also as a consequence of favourable economic conditions, labour shortages and, to a lesser extent, increase in the minimum wage at the beginning of the year. Activity in construction decreased further, while indicators of expectations for the next few months improved again.

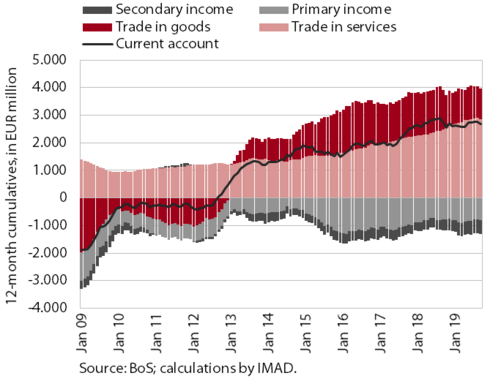

Current account of the balance of payments, September 2019

The current account surplus narrowed in September; it was down year on year in the last twelve-month period (at 5.5% of estimated GDP). The lower surplus compared with the previous twelve months was largely due to a lower surplus in trade in goods, which is attributable mainly to the easing of growth in the international environment. The lower current account surplus year on year was also a consequence of a higher net outflow of secondary income, which is mainly related to higher VAT- and GNI-based payments into the EU budget. Net outfows of primary income remained similar to those recorded one year earlier. The surplus of trade in services was higher, mainly on account of a higher trade surplus in transport and construction services and higher net revenues from travel.

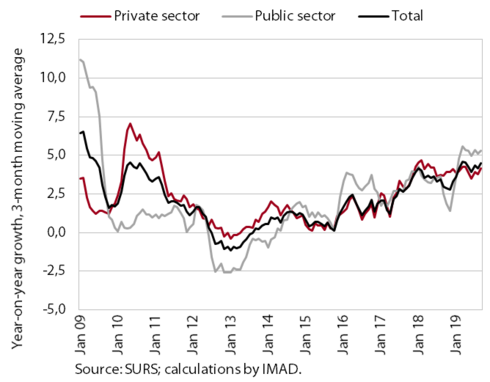

Wages, September 2019

Wage growth this year is higher than last year. In the first nine months it was 4.3%, compared with 3.4% in the same period last year. Higher wage growth mainly reflected higher growth in the general government sector resulting from higher valuation of most positions (agreed at the end of last year), promotions and, to a lesser extent, increase in the minimum wage. With relatively strong growth in economic activity and a shortage of appropriately skilled workers, further wage growth was also recorded in the private sector. Wage growth in the private sector was also affected by the increase in the minimum wage early in the year. Wages thus increased the most in activities with the greatest labour shortages and a large share of minimum wage recipients (administrative and support service activities).

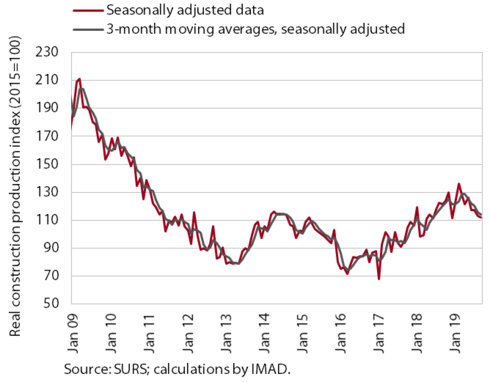

Construction, September 2019

The value of construction output dropped further in September. Activity was 8.1% lower year on year. After the strong growth early in the year, which was also due to favourable weather conditions, the value of construction output fell in the middle of the year. The decline was the most pronounced in the construction of non-residential buildings, which is related to deteriorated expectations of the business sector and its investment activity. The slowdown in civil-engineering works was more moderate, while activity in the construction of residential buildings increased further amid significant monthly fluctuations. The indicators of the stock of contracts and new contracts in construction, which fell towards the end of last year, have been strengthening again this year and are already higher than last year. They improved the most in the construction of residential and non-residential buildings, while they maintained similar levels as recorded at the beginning of the year in civil-engineering works.