Charts of the Week

Current economic trends from 11 June to 15 July 2022: value of fiscally verified invoices, activity in construction, production volume in manufacturing and other charts

At the end of June and beginning of July, the value of fiscally verified invoices was nominally well above the same period last year, given the high price growth, but the effect of last year’s low base has begun to fade. Construction activity picked up in May after two months of decline and was well above the previous year’s level, with particularly high growth in the construction of buildings. Manufacturing production increased slightly in May, with high-technology industries recording the highest year-on-year growth this year. The 12-month surplus on the current account has fallen to just over a tenth of what it was a year ago, mainly due to the impact of rising prices for energy and other commodities. In June, electricity consumption in the distribution network was lower than in the same periods of 2021 and 2019, which we associate with the impact of unstable supply chains and material shortages in manufacturing, as well as higher electricity prices.

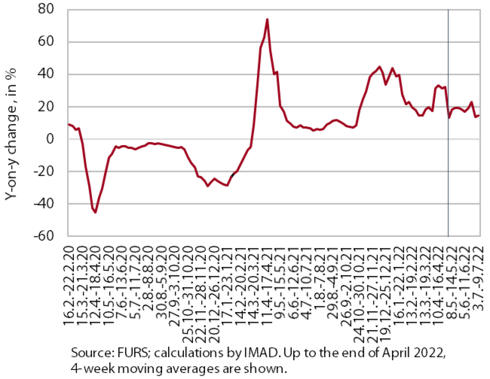

Value of fiscally verified invoices, in nominal terms, 26 June–9 July 2022

Amid high price growth, the value of fiscally verified invoices between 26 June and 9 July 2022 was 14% higher year-on-year in nominal terms and 10% higher than in the same period of 2019. Year-on-year growth was significantly lower than in the previous two weeks, partly because the effect of last year’s low base has begun to fade. Growth in trade was lower (both in retail and wholesale trade, while turnover in the sale of motor vehicles was lower year-on-year). Growth also declined slightly in accommodation and food service activities, certain personal services and arts, entertainment and recreation, with further easing of restrictions on businesses last June.

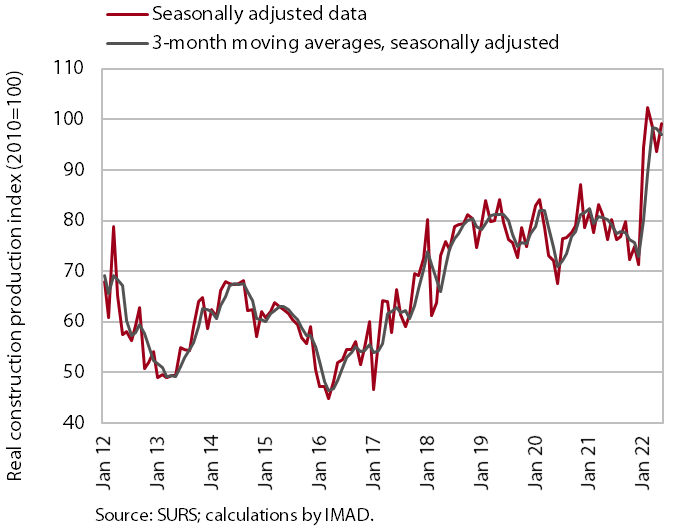

Activity in construction, May 2022

According to figures on the value of construction put in place, construction activity increased in May and was significantly higher year-on-year. After a strong pick-up at the beginning of this year, the value of construction put in place declined on a monthly basis in March and April before rising again in May. In the first five months, the value of construction put in place was 22.2% higher than in the same period of 2021. Construction of buildings stands out in terms of growth in activity. Activity also increased in civil engineering, while activity was lower in specialised construction work (installation works, building completion, etc.).

The data based on VAT forms show that the year-on-year increase of construction activity was about 17 p.p. lower this year than can be assumed from the data on the value of construction put in place.

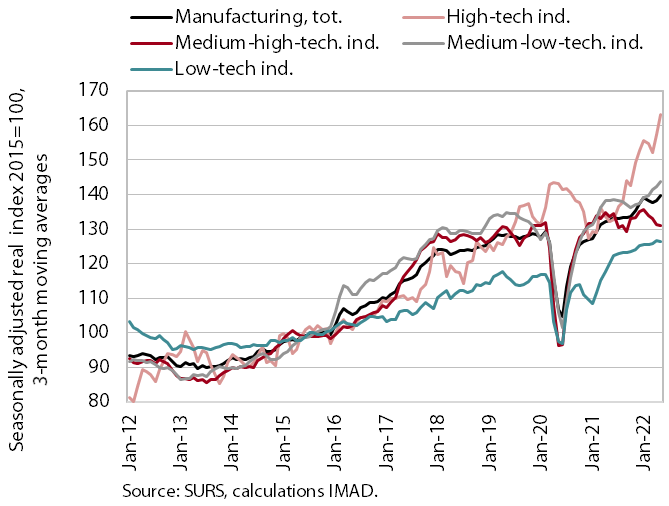

Production volume in manufacturing, May 2022

Manufacturing production continued to rise slightly in May. Growth continued in the high-technology and medium-low-technology industries, while production in the other two groups declined again. In the first five months, production was 5.1% higher than a year ago, with the strongest growth in the high-technology industries. Most other industries were also at or above last year’s levels, while the manufacture of motor vehicles, trailers and semi-trailers in particular was lower and was also the only industry that has not yet reached pre-epidemic levels due to various factors (supply chain disruptions, lower demand, restructuring towards a greater supply of electric vehicles).

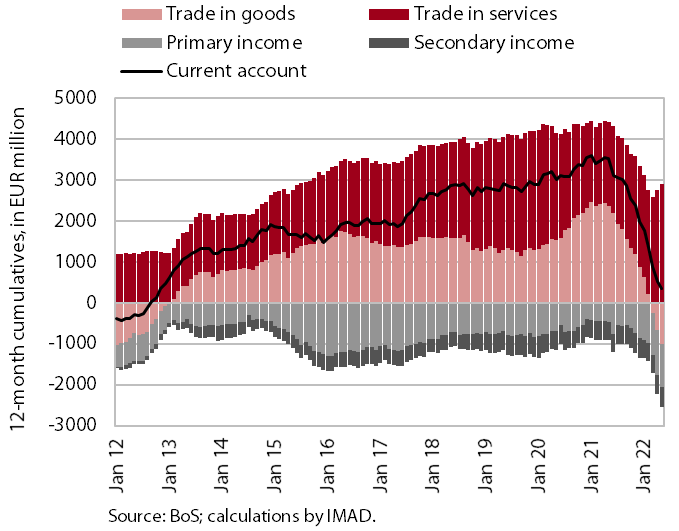

Current account of the balance of payments, May 2022

The 12-month surplus of the current account of the balance of payments fell to just over a tenth of what it was a year ago. It amounted to EUR 363.7 million (0.6% of estimated GDP), compared to EUR 3.5 billion or 6.8% of GDP in 2021. With imports growing faster than exports, this was mainly due to goods trade balance, which turned from a surplus to a deficit at the end of last year. This is mainly related to rising prices for energy and other primary commodities, which have a negative effect on the balance of payments due to a relatively rigid demand. Net outflows of primary and secondary incomes were also higher year-on-year in May. The primary income deficit was higher mainly due to higher payments of dividends and profits to foreign investors, which is related to high economic activity in Slovenia. In addition, payments from traditional own resources to the EU budget were also higher. The higher secondary income deficit was characterised by higher pension transfers to pensioners abroad. The services surplus continues to grow, especially in trade in travel (easing of COVID-19 restrictions) and in trade in telecommunication, computer and information services.

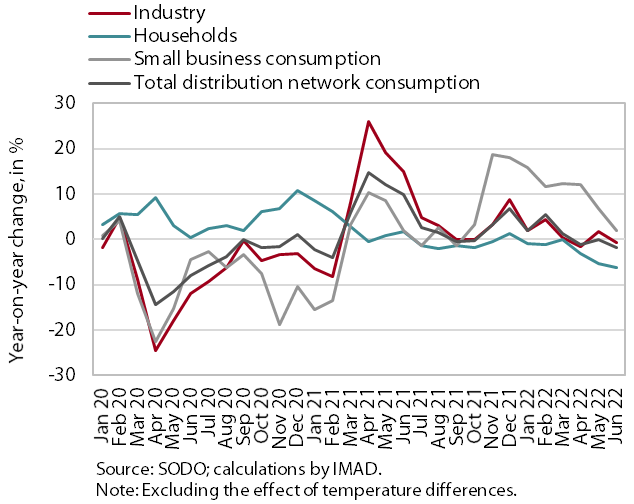

Electricity consumption by consumption group, June 2022

In June, electricity consumption in the distribution network was lower than in the same periods of 2021 and 2019. With one more working day, industrial electricity consumption in June was 0.6% lower year-on-year, while small business electricity consumption was 2.0% higher. The latter may have been partly influenced by last year’s low base due to restrictions in trade and services. Household consumption in June was 6.2% lower than a year ago and 4.3% lower than in the same period of 2019, which could already be due to higher electricity prices for households. Industrial electricity consumption and small business electricity consumption in June were about the same as in June 2019, with three more working days this June. This development is related to the impact of unstable situation regarding supply chains and material shortages in manufacturing and higher electricity prices.

Road and rail freight transport, Q1 2022

The volume of road and rail freight transport increased in the first quarter of 2022. The volume of road transport performed by Slovenian vehicles increased significantly quarter-on-quarter and was 13% higher than in the same quarter of 2019 (cross-trade increased by 7% and other road transport by 19%). Amid strong growth of economic activity, the high quarter-on-quarter growth was mainly due to further increase in road transport performed at least partially on Slovenian territory (exports, imports and national transport combined), while the volume of cross-trade decreased again. Thus, the share of cross-trade transport performed by Slovenian vehicles in total transport is still much lower than before the epidemic, while the share of transport performed by foreign vehicles on Slovenian motorways (according to DARS data) has returned to its previous level. Rail freight transport, which had been declining also before the epidemic, was a tenth lower than in the same quarter of 2019.