Charts of the Week

Current account from 14 June to 18 June: traffic of electronically tolled vehicles, electricity consumption, wages, labour market and other charts

Current indicators of economic activity show that in the second week of June, the volume of freight traffic on Slovenian motorways was very high, slightly exceeding the pre-crisis level of 2019. Electricity consumption was also slightly up year-on-year. However, it was slightly below the pre-crisis level, probably mainly due to reduced tourism activities. According to data on the fiscal verification of invoices, total turnover in the first half of June was already slightly above pre-crisis levels, while turnover in the services sector, where restrictions remained relatively high, continued to lag behind pre-crisis levels by more than half. The number of registered unemployed continued to fall sharply in June, and by mid June it was almost a fifth lower year-on-year, but still slightly higher than in June 2019. After strengthening in the second half of last year, activity in the construction sector fell again, but remained higher than a year ago.

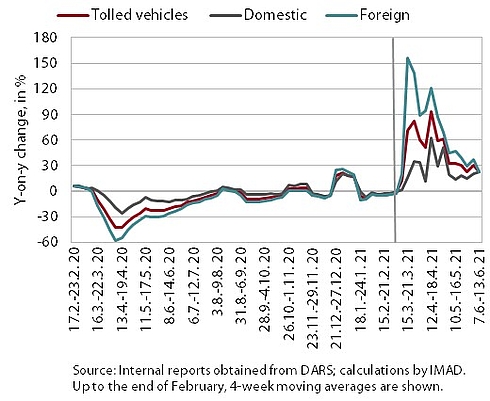

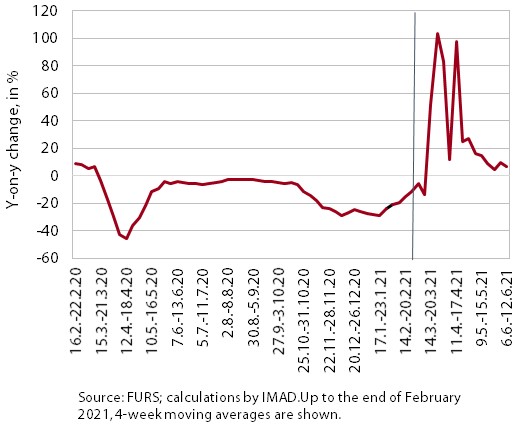

Traffic of electronically tolled vehicles on Slovenian motorways, June 2021

Freight traffic on Slovenian motorways in the second week of June was 23% higher than in the same period of last year and 3% higher than in the same period of 2019. The volume of freight traffic again exceeded 22 million kilometres driven, reaching the third highest weekly measured value this year (last year it did not reach such a volume due to the epidemic). Year-on-year, the volume of domestic and foreign vehicle traffic increased by almost a quarter, but this was still mainly due to the lower volume of traffic in the same period last year during the first wave of the epidemic. Compared to the same week of the pre-crisis year 2019, it was 6% higher for domestic vehicles and 1% higher for foreign vehicles.

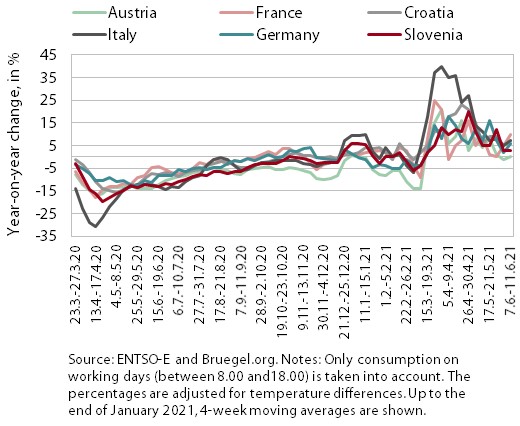

Electricity consumption, June 2021

In the week between 7 and 11 June, electricity consumption was 3% higher than the same week in 2020, but 10% lower than the same week of the pre-crisis year 2019. The reason for the higher year-on-year consumption was in particular the low base of last year. However, despite the easing of a number of containment measures, consumption remained lower than before the crisis. Mainly due to the base effect, year-on-year higher consumption was also recorded in most of Slovenia’s main trading partners (around 7% in Italy, Germany and Croatia and 10% in France), except in Austria, where it remained the same as in the same period last year. Compared to the same week of 2019, consumption was down in Austria (4%), Italy (3%) and Germany (2%), while it was up in France (6%) and remained more or less unchanged in Croatia.

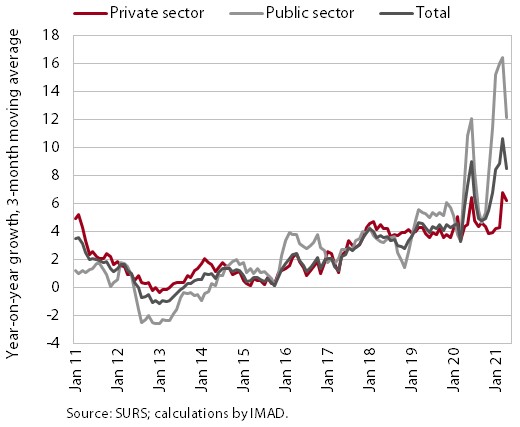

Wages, April 2021

After a strong year-on-year average wage growth in recent months, growth remained moderate in April (3%). In the private sector it was lower (2%), partly due to the high growth in the same month of the previous year (base effect) caused by the introduction of crisis bonuses and the wage calculation methodology. In the public sector, on the other hand, growth remained relatively high (5.6%) despite the already high base last year (introduction of bonuses for hazardous working conditions and additional workload, as well as a bonus for work in crisis conditions in accordance with the collective agreement), inter alia, due to the performance bonus introduced in the middle of last year.

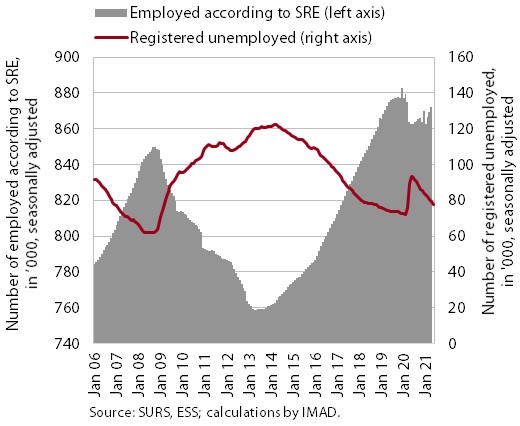

Labour market, April–June 2021

The number of registered unemployed persons continued to fall in the first half of June. The decline in the unemployment rate strengthened slightly in May and this trend continued in the first half of June. In addition to seasonal influences, which were not significantly different from those in the pre-epidemic period, the decline was also related to the gradual relaxation of containment measures and the economic recovery. As of June 15, 72,508 people were unemployed, down 3.5% from the end of May and down about 19% from a year ago, according to ESS unofficial (daily) data. However, compared to June 2019, the number was about 2% higher. The number of employed persons was 1% higher in April than in the same month a year earlier, mainly due to the base effect (a sharp fall in April 2020 due to the outbreak of the epidemic). The year-on-year decline in employment continued to be the strongest in accommodation and food service activities and administrative and support service activities, i.e. the sectors most affected by the containment measures, while the largest increase was recorded in health and social work.

Fiscal verification of invoices, June 2021

According to data on fiscal verification of invoices, turnover in the first two weeks of June was 8% higher year-on-year and 2% higher than in the same period of 2019. Year-on-year turnover growth slowed in most sectors. Turnover was actually lower in sectors that saw a large increase last June (such as motor vehicle sales). In some sectors, particularly those related to tourism (accommodation, gambling and betting, travel agencies), year-on-year growth remained high due to a further easing of containment measures. Total turnover in the first two weeks of June was 2% higher than in the same period of 2019, which was mainly a result of growth in wholesale and retail trade. Turnover in services where restrictions were still relatively high (cultural and entertainment services, accommodation, gambling and betting), remained more than half lower than in the same period of 2019.

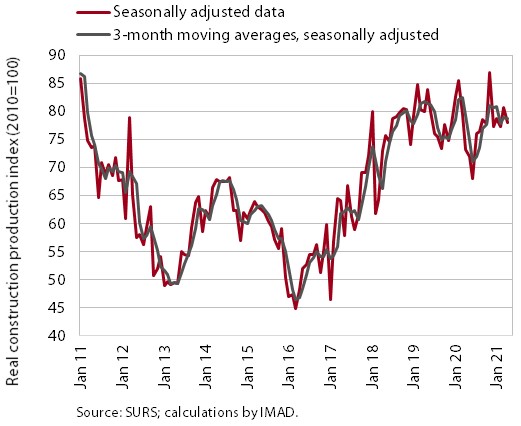

Construction, April 2021

Construction activity slowed somewhat in April. The value of construction output fell by 3.4%. However, it was 6.5% higher than a year earlier. Compared with the previous month, construction activity fell in all segments and strengthened only in non-residential construction, where it had fallen sharply in previous months. Activity in this construction sector is also significantly lower this year than last year's average. Year-on-year, the outlook is best for residential construction (nearly 30% higher activity). Activity in civil-engineering and specialized construction is also higher than last year. Data on the number of contracts suggest that activity in non-residential construction will remain relatively low, while other segments, particularly civil-engineering and specialised construction activities, are likely to perform better.

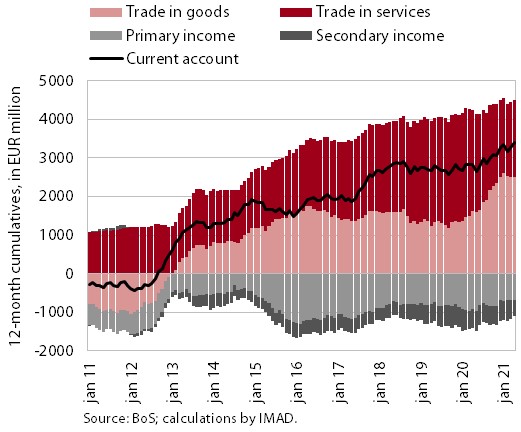

Current account, April 2021

In April, the current account surplus was again higher year-on-year. This is mainly due to the surplus of secondary income (a deficit was recorded last April), mainly due to more government funds received (social benefits from the EU budget). Due to the easing of containment measures, trade in services recovered after a year. The surplus in trade in services was again higher year-on-year, mainly due to a larger surplus in transport and travel services. The primary income deficit was lower in April than a year earlier, mainly due to lower net payments of interest on external debt. The surplus in trade in goods remained at a similar level as in April last year (EUR 168 million). The high year-on-year nominal growth in trade in goods in April was also the result of higher energy prices and the prices of other primary commodities, which have the largest impact on the import price growth. In April, export prices of goods rose by 1.8% year-on-year, while import prices rose by as much as 7% and the terms of merchandise trade deteriorated by 4.8%. The 12-month current account surplus remains high (EUR 3.4 billion; 7% of GDP).