Charts of the Week

Charts of the week from 29 September to 3 October 2025: consumer prices, exports and imports of goods, turnover in trade, turnover in market services and other charts

Year-on-year inflation eased slightly in September (2.6%), mainly due to slower growth in clothing and footwear prices. The largest contribution to inflation continued to come from higher prices of food and non-alcoholic beverages (7%). Goods exports and imports (excluding operations involving processing) declined month-on-month in August after real growth in July and were also lower year-on-year. On average, in the first eight months of the year, exports were lower year-on-year, while imports remained broadly unchanged compared with the same period last year. Despite weaker performance in most sectors in July, turnover in trade remained higher year-on-year across all sectors in the first seven months of the year. Total real turnover in market services declined further in July after contracting in the second quarter and was roughly at the same level as in July last year. In the first seven months, year-on-year growth in turnover was recorded only in transportation and storage as well as in professional and technical activities. According to seasonally adjusted data, the number of registered unemployed persons increased for the third consecutive month in September (by 0.5%), mainly due to a higher inflow of persons with temporary protection status into the unemployment register. The number of unemployed was also marginally higher year-on-year (by 0.2%). Yields to maturity on government bonds of core euro area countries rose in the third quarter amid heightened economic uncertainty and expectations of higher public expenditure on infrastructure and defence, while the yield to maturity on Slovenian government bonds declined.

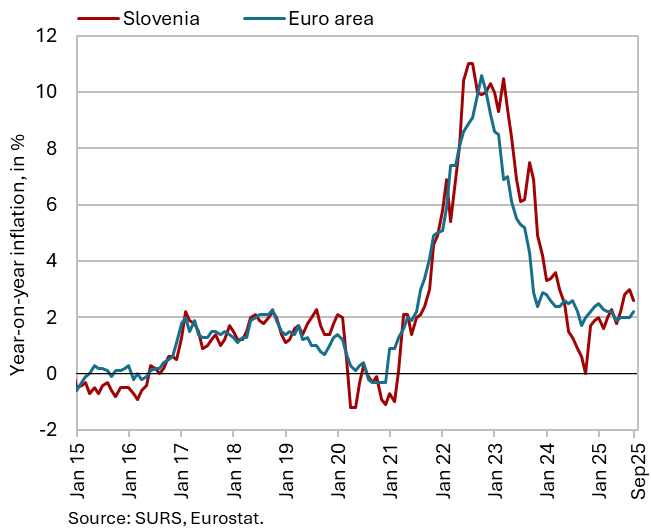

Consumer prices, September 2025

Year-on-year growth in consumer prices eased slightly in September, to 2.6%. Following a modest decline in clothing and footwear prices in August, prices in this group rose again in September (by 8.5%), though their year-on-year growth rate more than halved (to 3%). This contributed to a lower year-on-year increase in semi-durable goods prices (2% compared with 5.2% in August). Price growth in durable goods remained moderate (0.4%). Year-on-year growth in food and non-alcoholic beverage prices also slowed somewhat in September, yet remained the highest among all goods and services groups, at 7%, contributing 1.3 p.p. to the overall 2.6% year-on-year inflation rate. Year-on-year growth in service prices stood at 2.8% and has fluctuated around 3% since the beginning of the year. Year-on-year inflation, measured by the HICP, stood at 2.7% in September, 0.5 p.p. higher than in the euro area. Preliminary data indicate that much of this difference continues to stem from significantly higher growth in food, alcohol, and tobacco prices (Slovenia 6.2%, euro area 3%).

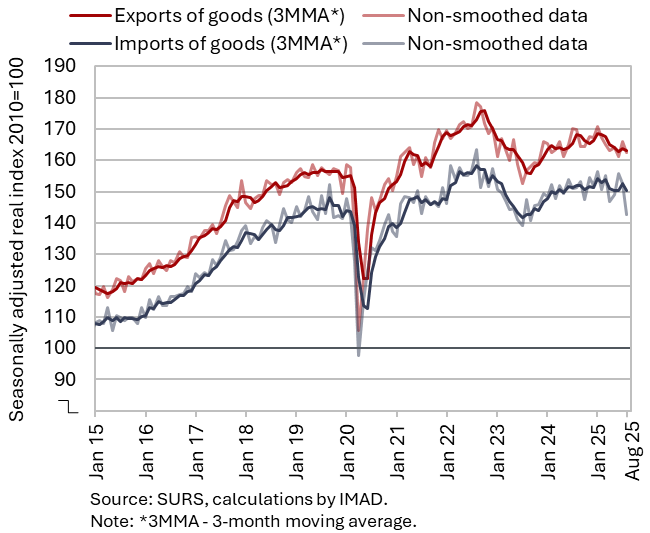

Exports and imports of goods, August 2025

Goods exports and imports declined month-on-month in August and were lower than a year earlier; SURS made a significant downward revision to goods imports for the first seven months of the year, which also affects the balance of goods transactions. After growing in July, real exports fell by 2.0% month-on-month in August. Exports to both EU countries (particularly Italy) and non-EU countries decreased. Exports of metals and metal products, machinery and equipment, and various manufactured goods declined, while exports of pharmaceutical and other chemical products as well as vehicles increased further. Imports fell for the second consecutive month (by -6.6%), with declines seen in imports from both EU and non-EU countries. Imports of consumer goods fell sharply (all seasonally adjusted).

Exports and imports were lower year-on-year in August. In the first eight months of 2025, exports were down by 0.7% year-on-year, while imports remained broadly unchanged compared with the same period last year.

Export orders in manufacturing showed no significant change in September and remained at a very low level, indicating no signs of a faster recovery in exports in the coming months.

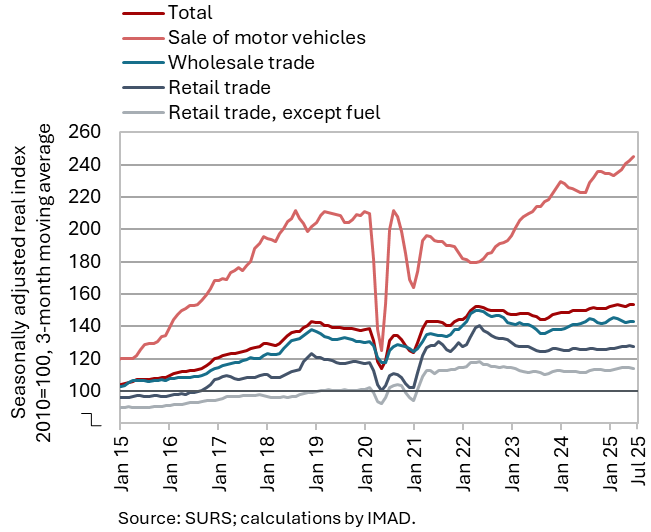

Turnover in trade, July 2025

Despite weaker performance in most sectors in July, turnover in trade remained higher year-on-year across all sectors in the first seven months of the year. Wholesale turnover declined further in July after contracting in the second quarter and, for the first time this year, was lower year-on-year. Turnover also decreased year-on-year in retail trade with food products, which fell slightly in July following weak growth in the second quarter. Turnover from retail trade with non-food products stagnated after recording growth in the first two quarters, while turnover from the sale of motor vehicles increased sharply. Sales across all trade sectors were higher year-on-year in the first seven months. Growth was strong in the sales of motor vehicles (7%) and modest in other trade sectors (on average slightly above 1%).

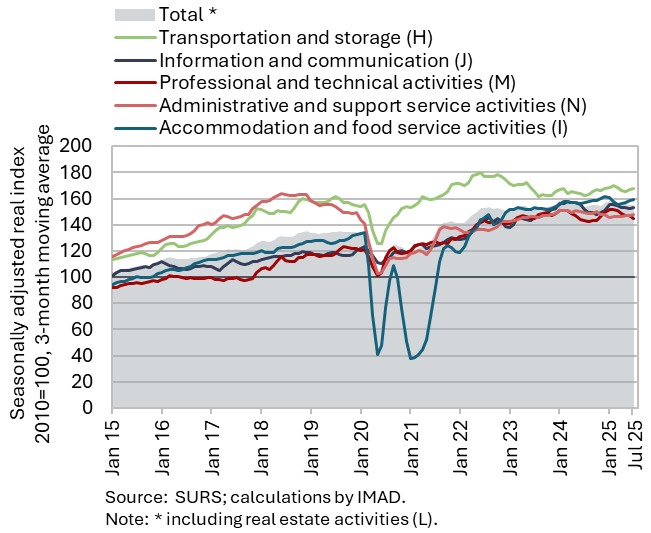

Turnover in market services, July 2025

Total real turnover in market services declined further in July (by 1%, seasonally adjusted) after contracting in the second quarter and remained unchanged year-on-year. The sharpest decline was recorded in professional and technical activities (following a marked downturn in the second quarter), mainly due to a stronger contraction in architectural and engineering services and consultancy services. Turnover also decreased in accommodation and food service activities, after having increased in the second quarter. In transportation and storage, turnover declined slightly in July after falling in the previous quarter, with the largest drop in storage activities. Administrative and support service activities also recorded a decline (after growth in the second quarter). The only increase was recorded in information and communication (continuing the growth seen in the first half of the year), with stronger growth stemming from higher sales of services both in the domestic market (computer services) and abroad (telecommunications). In the first seven months of 2025, real turnover was higher year-on-year only in transportation and storage and in professional and technical activities.

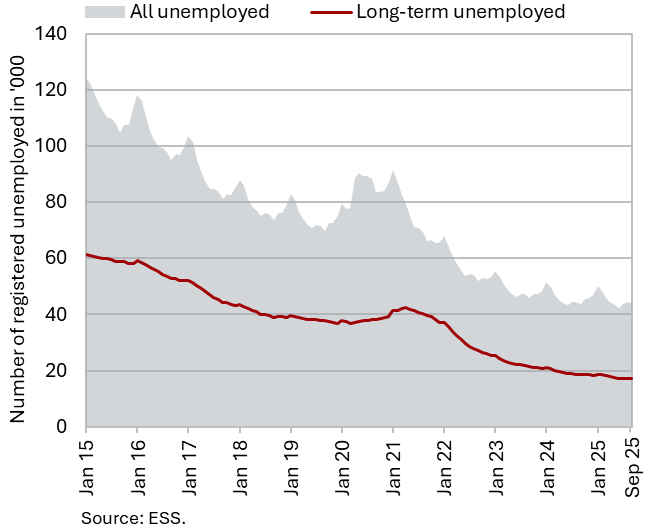

Unemployment, September 2025

The number of registered unemployed persons increased for the third consecutive month in September (by 0.5%, seasonally adjusted). According to the Employment Service of Slovenia, this may reflect an increased inflow of first-time jobseekers into unemployment, which since July this year may have been driven by a larger inflow of foreign nationals with temporary protection status into the unemployment register following legislative changes. According to original data, 43,944 people were unemployed at the end of September, 0.8% fewer than at the end of August, yet 0.2% more year-on-year. The year-on-year declines in long-term unemployment (–6.3%) and in unemployment among persons aged 50 and over (–7.3%) were somewhat smaller than in previous months. Since the end of last year, the number of unemployed young people (aged 15–29) has been above the level recorded a year earlier (in September, it was up 8% year-on-year).

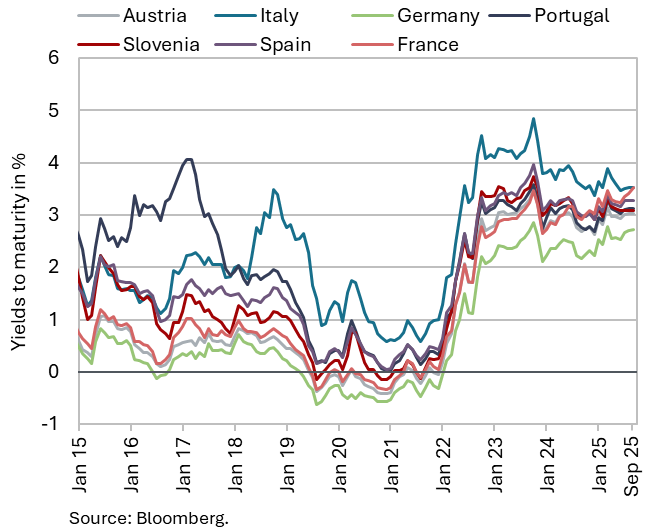

Government bonds, Q3 2025

The yield to maturity on Slovenian government bonds declined by 4 basis points in the third quarter, to 3.09%. The spread to the German bond narrowed by 19 basis points (to 39 basis points), the lowest level in the past four years. This was mainly due to a 15 p.p. increase in the yield on the German government bond. Yields to maturity on bonds issued by core euro area countries (e.g. Germany and France) rose amid uncertain economic conditions and expectations of higher public spending on infrastructure and defence. The ECB, however, did not change its interest rates in the third quarter, given the relatively stable inflation environment.