Charts of the Week

Charts of the week from 26 to 30 May 2025: economic sentiment, consumer prices, turnover in trade and other charts

Year-on-year consumer price growth eased more noticeably in May, falling by 0.5 p.p. to 1.8%, while prices remained unchanged at the monthly level. The decline in inflation was mainly due to year-on-year lower prices in the transport group and a slower increase in prices in the clothing and footwear group. The value of the economic sentiment indicator increased slightly in May, while remaining unchanged year-on-year. The improvement was primarily driven by an increase in consumer confidence. In the first quarter, real turnover in trade increased both on a quarterly and annual basis across all sectors except sales of food products, where it declined year-on-year, mainly due to the different timing of the Easter holidays. Total real turnover in market services declined slightly in the first quarter and was also slightly lower year-on-year. According to survey data, conditions in the labour market deteriorated slightly in the first quarter, amid heightened economic uncertainty. Forty-one thousand persons were unemployed (13.9% more than in the first quarter of last year), and the unemployment rate stood at 4% (up by 0.6 p.p. year-on-year). The number of persons in employment declined slightly year-on-year, particularly among the self-employed and those in other flexible forms of work.

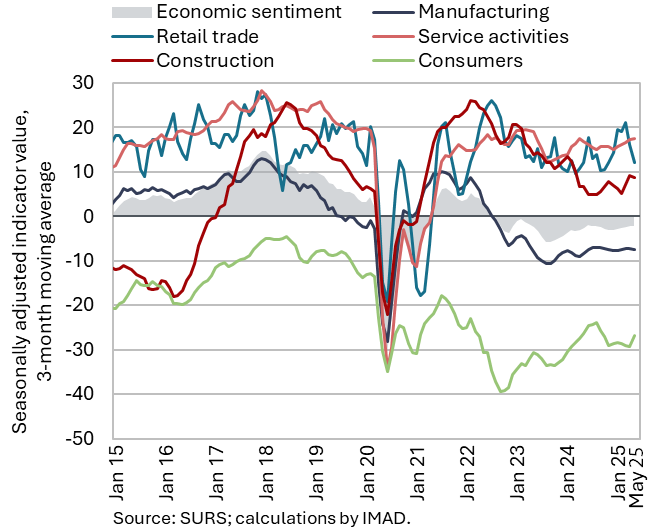

Economic sentiment, May 2025

The value of the economic sentiment indicator increased slightly in May compared to April, while remaining unchanged year-on-year. On a monthly basis, the consumer confidence indicator increased markedly, with improvements recorded across all of its components: the current financial situation of households, expectations regarding the country’s economic situation, expectations regarding households’ financial situation, and expectations concerning major purchases. Confidence in retail trade also increased, while confidence in other sectors deteriorated. The consumer confidence indicator was also higher year-on-year, and confidence in the service sector was higher than in May 2024. The economic sentiment indicator remains below its long-term average, with only the indicators for services and construction still exceeding their respective long-term averages.

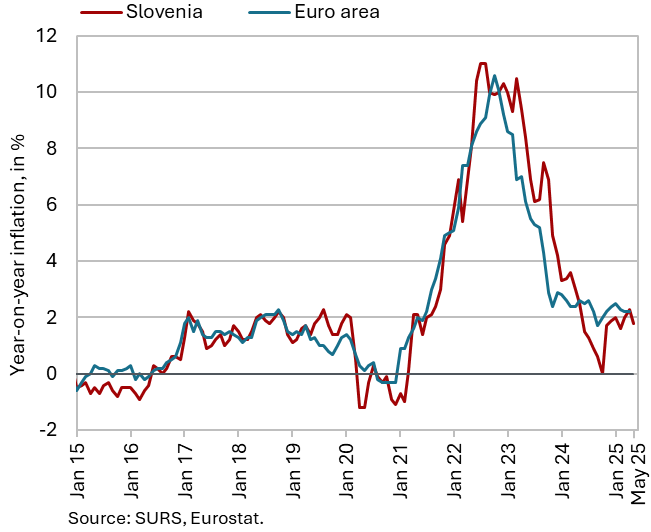

Consumer prices, May 2025

Year-on-year growth in consumer prices slowed more noticeably in May, declining by 0.5 p.p. to 1.8%, while prices remained unchanged month-on-month. The main contributors to the lower inflation rate were the year-on-year decline in prices in the transport group (–1.9%) and the slower growth in prices in the clothing and footwear group (1.3%, compared with 4.2% in April). According to our assessment, the lower prices in the transport group primarily reflect cheaper petroleum products, as well as a decline in motor vehicle prices. Following a marked monthly increase in April in the prices of clothing and footwear (in particular, a 20% rise in footwear prices), prices in this group declined slightly in May on a monthly basis, deviating from the typical seasonal price patterns observed in this group. This also contributed to the moderation in the growth of semi-durable goods prices (1.6%), while prices of durable goods remained lower year-on-year (-0.7%). The growth of food and non-alcoholic beverage prices moderated slightly in May, yet at 5.5% year-on-year, it remained the highest among all groups in the consumer price index. A similar year-on-year growth rate was recorded in the restaurants and hotels group (5.3%). Year-on-year growth in service prices (3.2%) stayed close to levels observed in recent months.

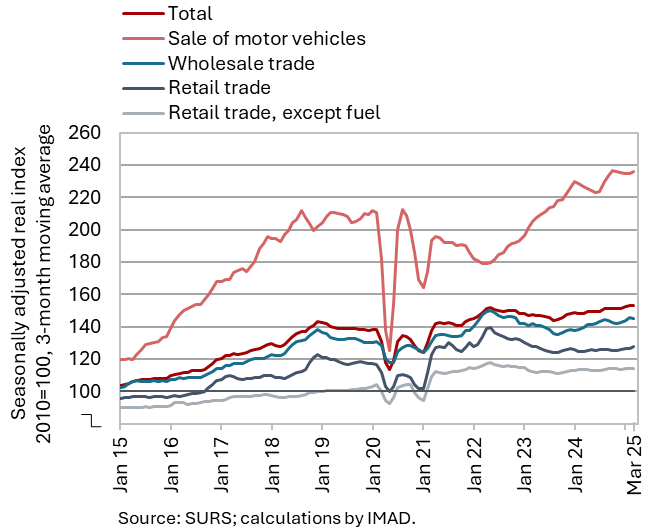

Turnover in trade, March 2025

In the first quarter, real turnover increased quarter-on-quarter and year-on-year in all trade sectors except in retail sales of food products. The 1% year-on-year decrease in turnover from retail sales of food products was driven by a significant year-on-year decline in March (-6%), primarily due to the timing of the Easter holidays and related pre-holiday purchases (last year these took place in March, while this year in April). In all other trade sectors, turnover increased on both a quarterly and year-on-year basis in the first quarter. Real turnover rose by 3% year-on-year in wholesale trade and in the sale of motor vehicles, while in retail trade of non-food products it increased by 2%.

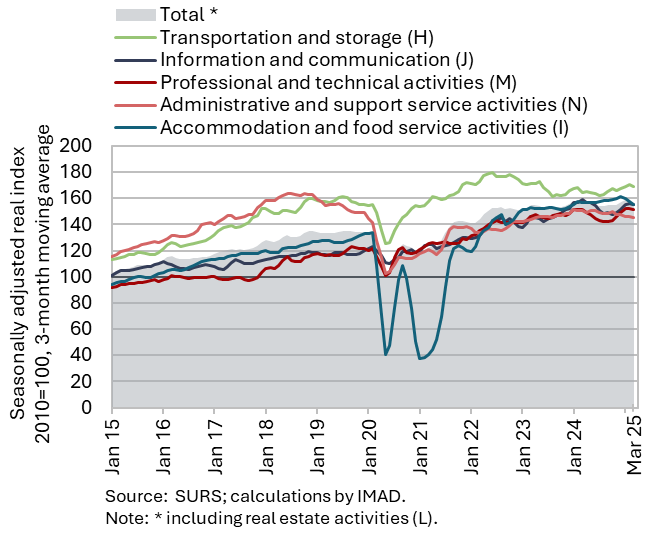

Turnover in market services, March 2025

Total real turnover in market services in the first quarter was broadly unchanged compared with the fourth quarter of last year, but slightly lower on a year-on-year basis (by 0.3%). Following strong growth at the end of 2024, quarter-on-quarter turnover growth further accelerated in the information and communication sector, supported by both main activities – telecommunications and computer services. The turnover growth observed in the second half of last year continued in the transportation and storage sector, this time with particularly strong growth in air transport. In professional and technical services, growth moderated slightly after strengthening in the fourth quarter, although turnover growth in architectural and engineering services remained particularly strong. Turnover in accommodation and food service activities, however, declined more markedly after strengthening in the second half of last year. In administrative and support service activities, where turnover has been decreasing since the second quarter of last year, the downturn deepened further, particularly in employment agencies. On a year-on-year basis, real turnover in the first quarter increased in transportation and storage as well as in professional and technical services.

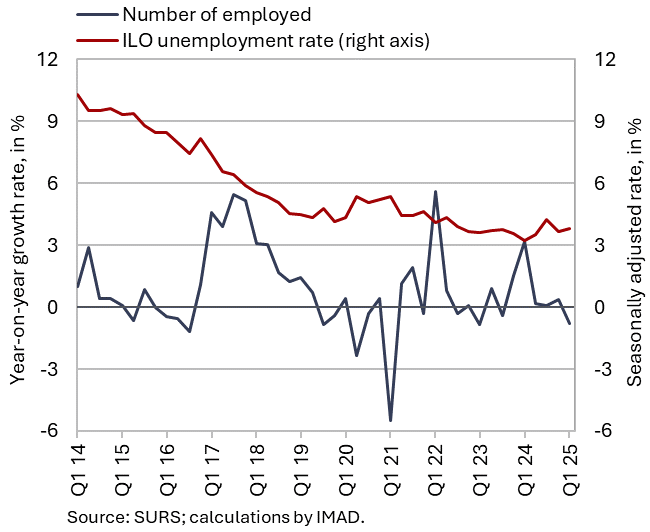

Active and inactive population, Q1 2025

According to survey data, labour market conditions deteriorated slightly in the first quarter of this year, which can also be linked to increased uncertainty in the economic environment. The number of unemployed persons totalled 41,000, representing a 13.9% increase compared with the same quarter of the previous year. The survey unemployment rate stood at 4%, up by 0.6 p.p. year-on-year. The number of persons in employment was slightly lower year-on-year in the first quarter (-0.8%). This reflects a year-on-year increase in the number of employees in labour relation, while the number of self-employed persons and those engaged in other forms of work (e.g. student work) declined. These types of employment are typically the first to transition into unemployment or inactivity during periods of increased economic uncertainty.