Charts of the Week

Charts of the week from 10 to 14 July 2023: manufacturing activities, activity in construction, current account of the balance of payments and other charts

Manufacturing output rebounded strongly in May after contracting in April, but remained below the first quarter level on average in the second quarter. In most industries, most notably in energy-intensive ones, it was lower year-on-year, while it was significantly higher in high-technology industries. Electricity consumption in the distribution network showed no signs of a year-on-year recovery of production in June, and electricity consumption in other consumption groups was also lower year-on-year in June. Data on the value of construction put in place show that construction activity increased again in May after a decline in April and was 25% higher year-on-year. The value of fiscally verified invoices at the end of June and the beginning of July was 5% higher year-on-year in nominal terms, mainly due to turnover growth in trade, which had been lower year-on-year in the previous 14-day period, partly due to the timing of the public holiday. The 12-month current account surplus was higher than in the previous 12-month period and arose mainly from a higher surplus in trade in services, especially in trade in transport and travel services and in trade in telecommunications, computer and information services. The volume of road freight transport increased in the first quarter after falling in the previous three quarters, while the volume of rail freight transport continued to decline.

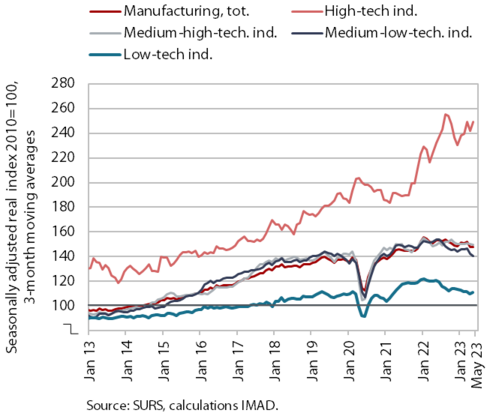

Manufacturing activities, May 2023

Manufacturing output recovered strongly in May after contracting in April, but remained below the first quarter level in the two months as a whole. In May, it increased in all industry groups according to technology intensity. In April and May it was on average below the first quarter average, except in high-technology industries, which exceeded the level of the same period last year in the first five months of this year. Output in most medium high technology industries (with the exception of energy-intensive chemical industry) was also higher year-on-year. Output in all energy-intensive industries and in most less technology intensive industries remained lower in the first five months than a year ago. The outlook for manufacturing remains weak. In June, most companies still did not expect exports to pick up in the coming months.

Activity in construction, May 2023

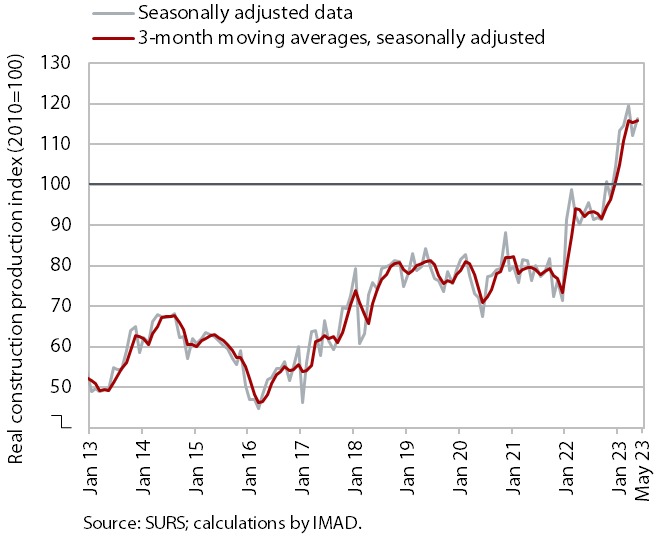

According to data on the value of construction work put in place, construction activity increased by 4% in May. The value rose after falling in April and was 25% higher compared to May last year. In the first five months, it was on average 24% higher than the same period last year. As regards buildings, it went up by 21%, as regards civil engineering by 22% and as regards specialised construction activities by 37%.

However, some other data suggest significantly lower growth in construction activity. Data on the value of industrial production in two activities traditionally strongly linked to construction do not point to such high growth. Production in other mining and quarrying was 14% lower year-on-year in May, while it was 13% lower in the manufacture of other non-metallic mineral products.

Current account of the balance of payments, May 2023

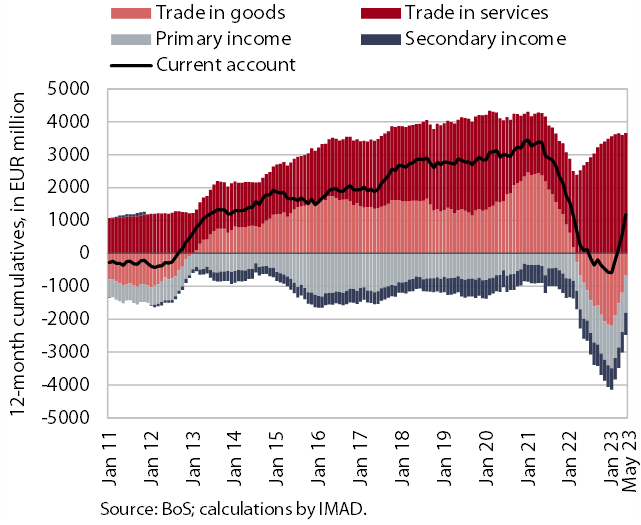

The 12-month current account surplus was higher than in the previous 12-month period, amounting to EUR 1,178.7 million (1.8% of estimated GDP). The year-on-year higher surplus arose mainly from a higher surplus in trade in services, especially in trade in transport and travel services and in trade in telecommunications, computer and information services. The 12-month goods deficit was lower year-on-year, due to the improvement in the balance of trade in goods this year, which was mainly due to a decline in imports. Net outflows of primary and secondary income were higher year-on-year. The primary income deficit was higher mainly due to higher income payments to foreign employees working in Slovenia, while the secondary income deficit due to higher payments to the EU budget from VAT and gross national income, and higher pension payments to pensioners abroad.

Electricity consumption by consumption group, June 2023

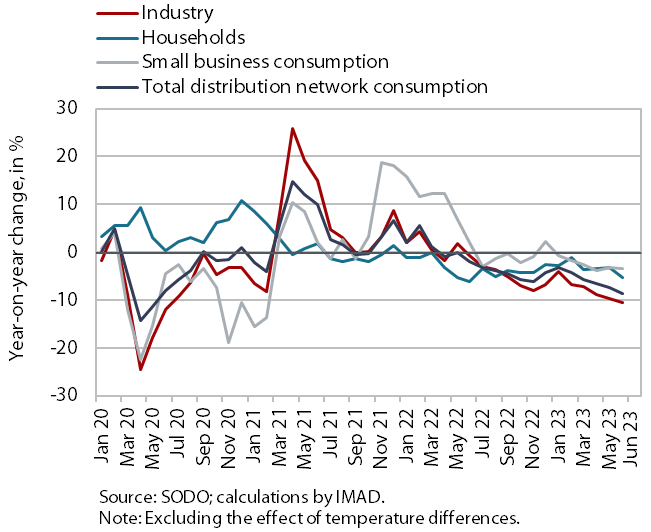

Electricity consumption in the distribution network remained lower year-on-year in June in all consumption groups. As in previous few months, the sharpest decline was seen in industrial consumption (-10.6% year-on-year), which could also indicate a year-on-year decline in industrial production. The year-on-year decline in household consumption in June (-5.3%) was higher than in the previous month (-3.1%), which could be due to a more rational use of energy encouraged by the expiry of the reduced VAT rate on energy. Small business consumption was 3.5% lower year-on-year in June.

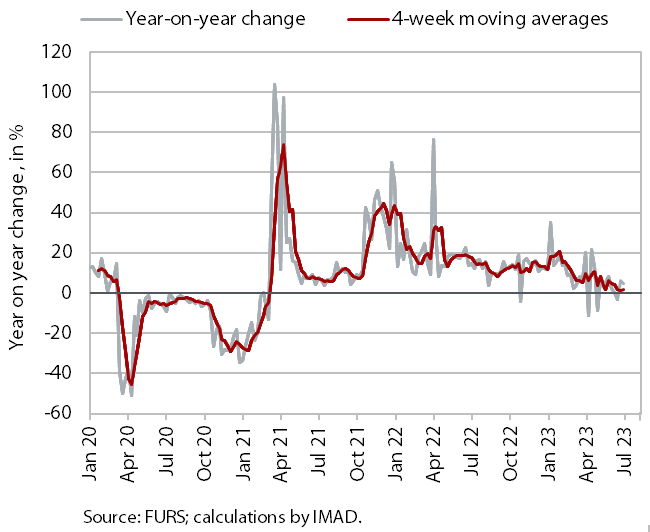

Value of fiscally verified invoices, in nominal terms, 25 June–8 July 2023

The nominal value of fiscally verified invoices between 25 June and 8 July 2023 was 5% higher year-on-year. The year-on-year growth was mainly due to growth in retail trade (7%), which had been lower year-on-year in the previous 14-day period, partly due to the timing of the public holiday. Turnover in retail trade, which accounted for almost half of the total value of fiscally verified invoices, increased by 4%, turnover in wholesale trade by 3% and turnover in the sale of motor vehicles by 28%. For the second time in a row, turnover in accommodation and food service activities was lower year-on-year (by 1%), mainly due to high turnover last year before the expiry of the deadline for the redemption of tourism vouchers.

Road and rail freight transport, Q1 2023

After a decline in the previous three quarters, the volume of road freight transport increased in the first quarter, while the volume of rail freight transport continued to decline. After a long period of decline, the volume of road transport performed by Slovenian vehicles increased quarter-on-quarter due to a renewed increase in cross-trade, while it was still 5% lower year-on-year. It was 7% higher compared to the same quarter in 2019 (cross-trade was 2% higher, while other road traffic performed at least partially on Slovenian territory was 11% higher). The share of cross-trade in total transport, which was above 50% before the epidemic, was thus 44% in the first quarter. Rail freight transport, already declining before the epidemic, was 8% lower year-on-year in the first quarter and 15% lower than in the same quarter of 2019.