Slovenian Economic Mirror

Slovenian Economic Mirror 2/2018

Economic activity in Slovenia remains high at the beginning of the year and the prospects are favourable. The number of employed persons continues to increase; wage growth has also strengthened slightly in the recent period. The average consumer price growth remains moderate year on year. Loans to domestic non-banking sectors continue to rise at the beginning of the year.

The prospects for euro area growth remain favourable at the beginning of this year. Confidence indictors are still relatively high, though there is more uncertainty regarding the continuation of strong GDP growth than at the end of last year. The value of the Economic Sentiment Indicator (ESI) fell slightly for most of Slovenia’s main trading partners but remains considerably above the long-term average. The Purchasing Managers’ Indicator (PMI) also fell but still indicates a continuation of activity growth in manufacturing. The Economic Sentiment Indicator (Ifo) for the euro area rose to its highest level since 2000. Amid favourable prospects, international institutions again revised upwards their forecasts for euro area growth. According to the ECB’s most recent forecast, GDP will rise in real terms by 2.4% and 1.9% respectively this year and next.

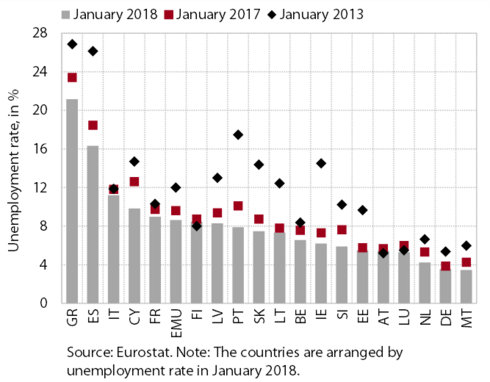

Labour market conditions in the euro area continue to improve. The unemployment rate (8.6%) at the beginning of 2018 is around 1 pp lower year on year and 3.4 pps lower than at the beginning of 2013, when it peaked (at 12.0%). Unemployment is also declining among young people, though it remains very high (17.7%). The employment rate is rising amid the strengthening of economic activity. It was 66.8% at the end of last year.

Economic activity in Slovenia remains high at the beginning of the year and the prospects favourable. Confidence continues to strengthen in construction, where activity rose in all segments at the beginning of the year. The strengthening of foreign demand continues to be reflected in positive export trends, high activity in manufacturing and further turnover growth in some market services (transportation, accommodation and food service activities, and individual sectors of knowledge-intensive services ). Moreover, favourable labour market trends and high consumer confidence are contributing to further growth in private consumption. Despite a deterioration in recent months, confidence in the economy remains high.

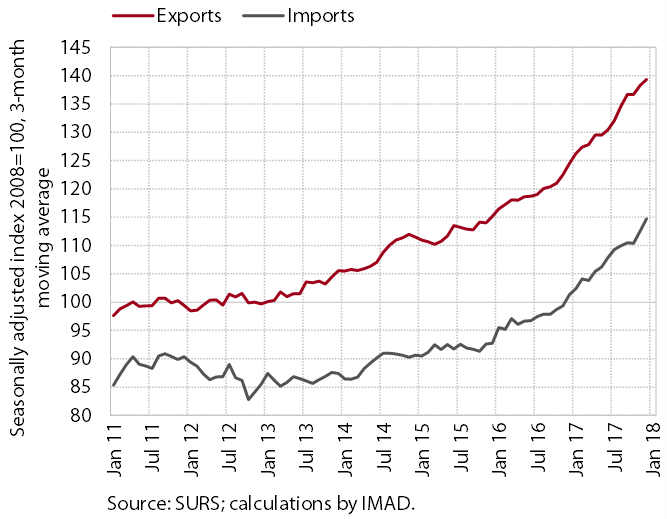

Positive export trends continue at the beginning of this year; goods imports are also rising amid stronger domestic consumption. Real exports and imports of goods were more than 10% higher year on year in January. Last year, higher exports were recorded for all key manufacturing products, particularly motor vehicles and metals. Expectations regarding further exports and foreign orders in manufacturing also remain high. The growth of imports is also picking up under the impact of rising domestic demand and intense export activity.

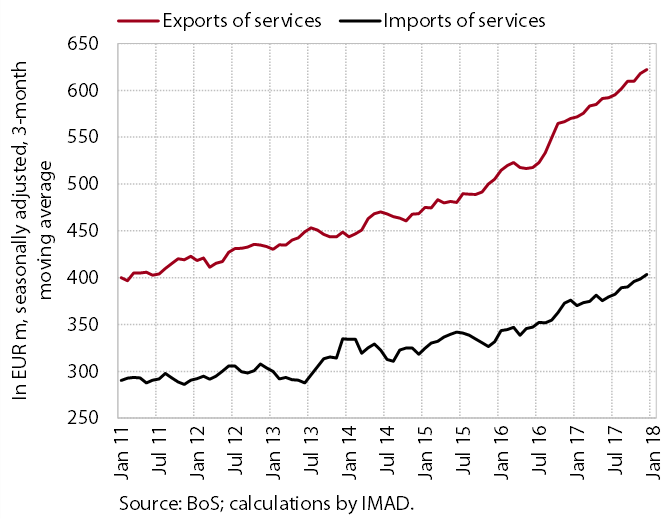

Nominal exports and imports of services remained high at the beginning of the year. In January exports were 11.5% higher and imports 9.0% higher year on year. The year-on-year growth of exports was driven primarily by transport and other business services (technical, trade-related and other business services). The latter also made a significant contribution to import growth.

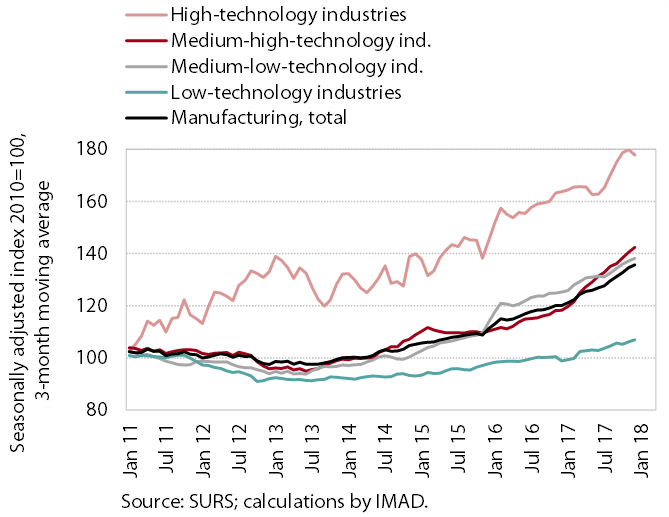

Production volume in manufacturing remained high at the beginning of the year and the prospects favourable. Relative to January 2017, production rose in all industries, the most in medium-high-technology industries, particularly in the manufacture of vehicles (the effect of the commencement of production of a new passenger car model from the first quarter of last year still being felt) and in the manufacture of machinery and equipment (reflecting the strengthening of investment both at home and abroad). The expectations of companies in manufacturing otherwise lowered somewhat at the end of the first quarter, though they remain at one of their highest levels in ten years.

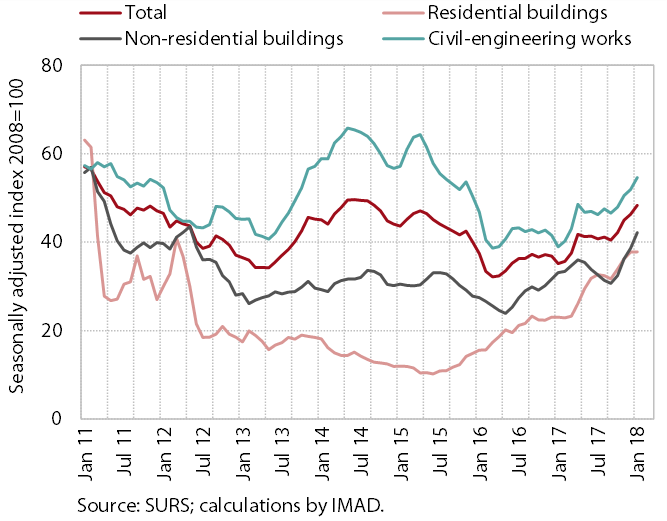

Reflecting favourable weather conditions, construction activity increased further in January. It was up in all three segments. The pick-up in the construction of buildings mainly reflects greater optimism in the private sector, while the higher value of civil engineering output is due primarily to increased investment expenditure by the government. Year on year, activity was up 76%, which was also a consequence of the base effect (activity in January 2017 having been the lowest since 2000).

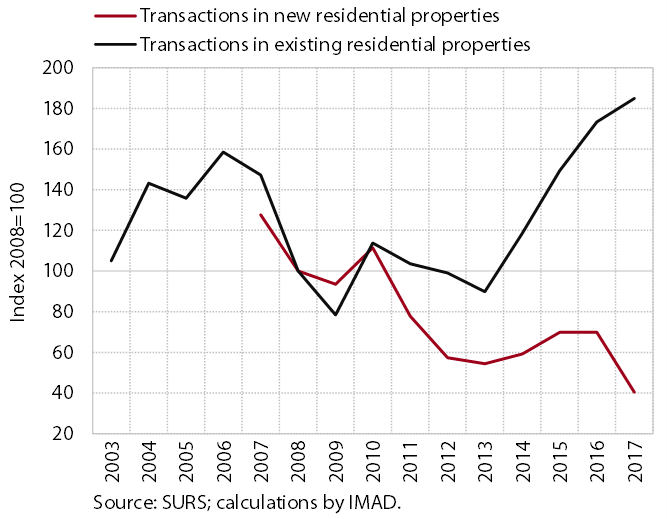

The sales of existing residential properties strengthened further in 2017 and significantly exceeded their pre-crisis levels. The sales of these properties, which accounted for around 90% of all real estate transactions, were 5.2% higher year on year and 15.0% higher than the 2006 peak. On the other hand, amid limited supply, sales of new residential properties were the lowest in the entire period. According to our estimate, further growth of the property market was mainly due to the relatively favourable borrowing terms, good economic situation and positive expectations.

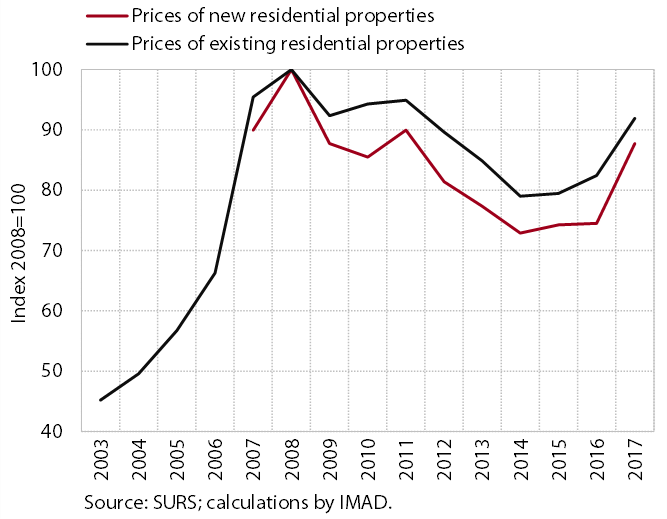

The growth in the average price of residential properties accelerated in 2017. The highest growth was recorded in the last quarter, while in the year as a whole, prices were up 8.0% year on year (compared with 3.3% in 2016). Price rises were recorded for all types of residential properties, the largest being for existing flats in Ljubljana. Prices of new family houses were also up for the first time following eight years of decline.

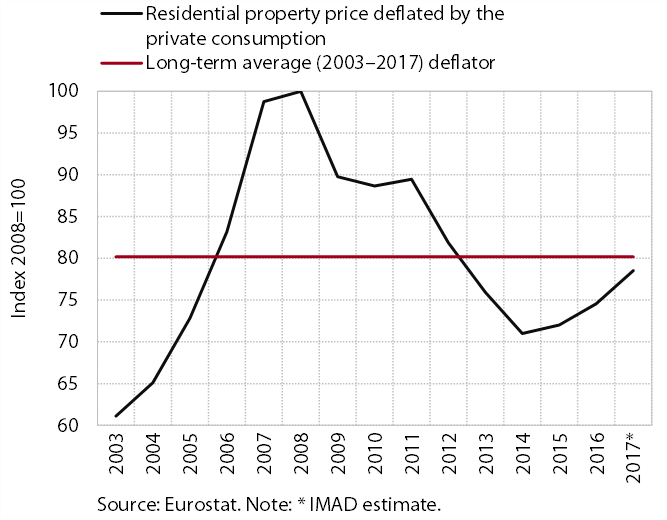

With last year’s increase, the residential property price deflated by the private consumption deflator approached the long-term average. The deflated price of residential properties rose 5.3% last year, which is just below the threshold of 6% used by the European Commission to determine the internal imbalances of EU Member States. Property prices are also recovering from previous declines in most other EU Member States. As this may – in certain cases – lead to their overvaluation, the Commission emphasises that the movement of these prices needs to be closely monitored.

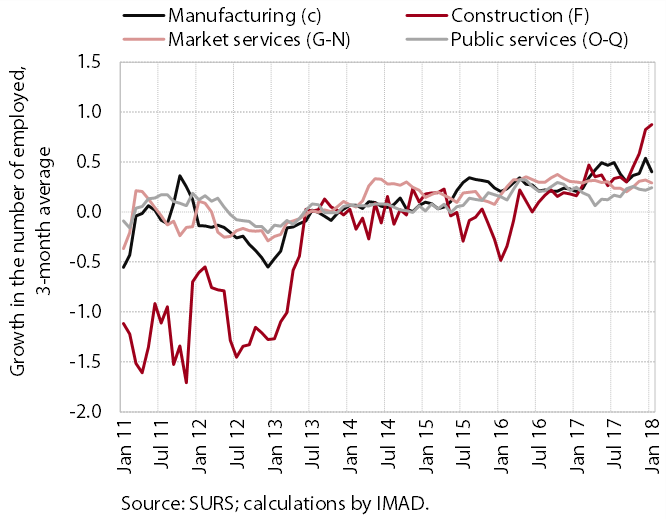

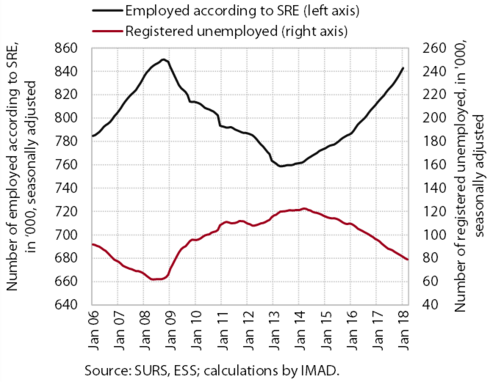

The number of employed persons continues to increase at a rapid pace; at the beginning of this year, it reached the level from the middle of 2008. The growth in this indicator, reflecting both higher participation and increased employment of foreign workers, is influenced by strong economic growth. In January the number of persons employed was up year on year in all private sector activities, particularly manufacturing, trade, transportation and, in the last few months, construction. The short-term expectations of enterprises about future employment remain high. In public service activities, the year-on-year growth in the number of persons employed mainly results from higher employment in the education (particularly primary education) and health sectors.

Amid strong hiring, the number of registered unemployed persons continues to decline rapidly. In the first quarter of this year, the inflow into unemployment dropped further year on year, largely because of fewer expiries of fixed-term employment contracts. There were also fewer first-time jobseekers, which is related both to the improvement in economic conditions and to the smaller generations of young people finishing school. The outflow into employment was also somewhat more modest than in the first quarter of 2017, but the share of the unemployed who found work remained high. At the end of March, 81,220 persons were registered as unemployed, 15.1% fewer than in March 2017.

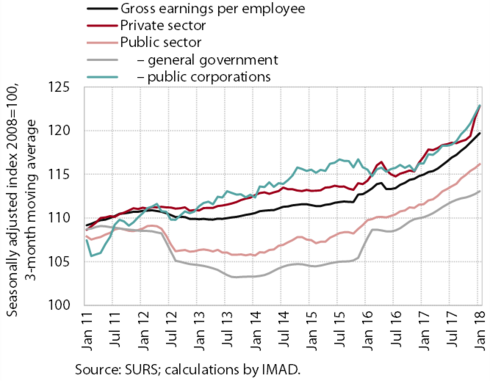

After several years of modest improvement, wages in both the private and the public sectors have recorded somewhat stronger growth in recent months. Wage growth in the private sector is mainly related to high levels of activity and strong business performance. The latter was also reflected in extraordinary payments at the end of last and the beginning of this year, these being the highest since the onset of the crisis. In January earnings rose most notably in manufacturing and some market services (trade, accommodation and food service activities, and financial and professional and technical activities). Wage growth in the public sector, on the other hand, reflected the implementation of agreements with trade unions and the regular promotions of the employed. Total wage growth, however, has not exceeded productivity growth in this period.

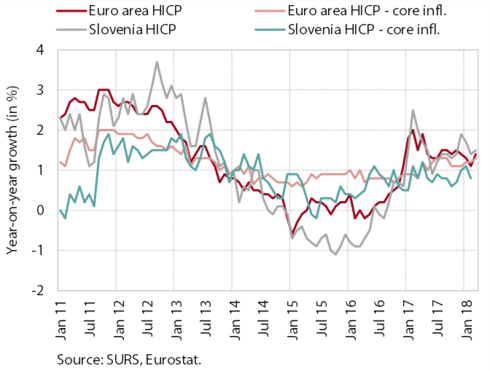

Average consumer price growth remains moderate year on year. Favourable economic conditions are reflected in prices of services, which continue to increase faster than those of goods. Particularly the contributions of price movements in the areas of housing, restaurants and hotels, and education are higher than last year. Price growth for oil products and seasonal products, however, is lower as a result of developments on global markets. Prices of durable goods remain down year on year. The level of core inflation remains low and is lower than the average for the euro area.

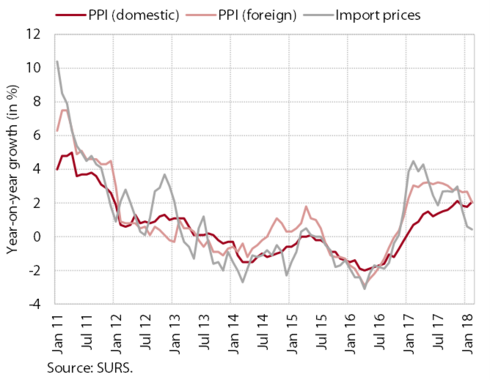

The year-on-year growth in import prices slowed considerably at the beginning of the year, while the growth of domestic industrial producer prices remained at just above 2%. The slowing growth of import prices is attributable not only to lower growth in commodity prices, but also to lower prices of energy. The growth of Slovenian industrial producer prices on the domestic market has strengthened somewhat in recent months; on foreign markets it has slowed slightly, meanwhile, meaning that the two rates are now roughly the same. Total price growth is still driven mainly by higher commodity prices. Growth in these has eased slightly at the beginning of this year, but less than has that of import prices. The highest growth rates are recorded for prices of metal products, which are rising at similar rates both at home and on foreign markets.

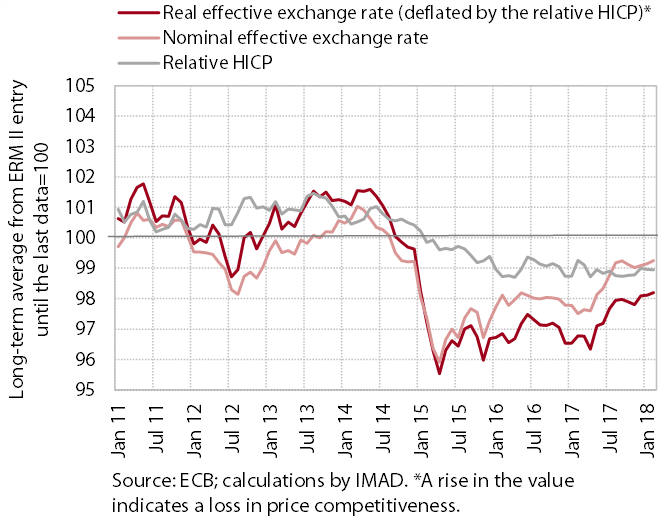

The price competitiveness of the Slovenian economy remains relatively favourable this year. In the first two months of 2018, the euro continued to gain value against the currencies of most of the country’s main trading partners. The nominal effective exchange rate nevertheless remained below the long-term average, its growth being one of the lowest in the euro area owing to the geographic structure of Slovenia’s trade. The decline in relative prices (as measured by the HICP), which had been mitigating the impact of the appreciation of the euro in the previous year, had no significant impact on price competitiveness in the first two months of this year.

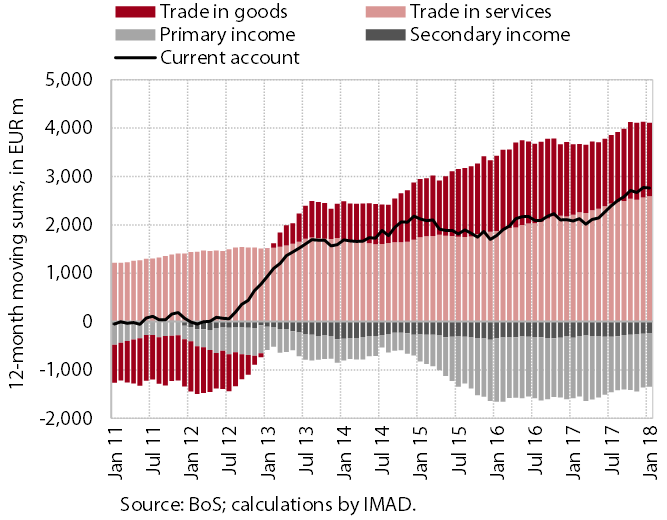

The surplus of the current account of the balance of payments remains high; in the 12 months to the end of January 2018, it was EUR 2.7 billion (5.9% of estimated GDP). The higher surplus in current transactions year on year in January was mainly due to the higher surplus of trade in services as a result of higher net revenues from travel and transport and the surplus of trade in other, trade-related, services. The surplus of trade in goods is also rising amid further growth in goods exports, although goods imports are also strengthening at the same time owing to rising domestic consumption. The deficit in primary income was down largely because of lower net payments of interest on external debt, which is chiefly related to lower yields on government bonds. The deficit in secondary income was also lower year on year, particularly owing to lower payments into the EU budget (VAT-based and GNI-based contributions).

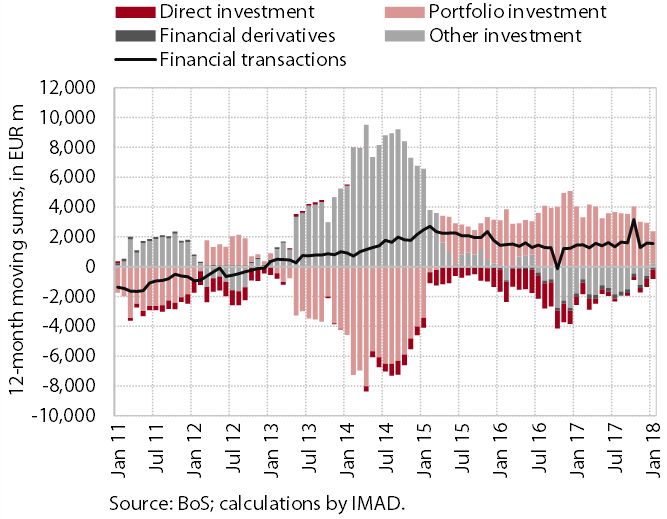

The net outflow in external financial transactions continues. External financial transactions showed a net outflow of EUR 1.5 billion in the 12 months to the end of January. It arose mainly from financial investment of the private sector and the BoS in foreign debt securities. A net outflow was also recorded for other investment, with both the government and the banks repaying foreign loans. In January the government borrowed money by issuing a bond. In direct investment, inflows of equity capital from foreign investors predominated.

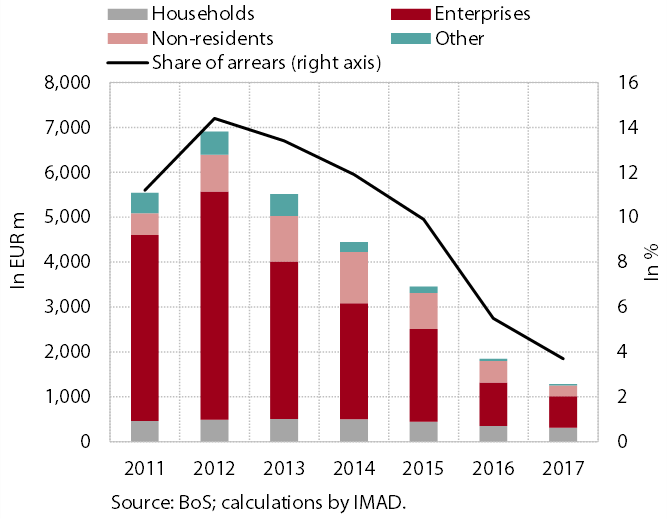

The volume of loans to domestic non-banking sectors continues to rise this year. Year-on-year growth in government loans has strengthened. Growth in loans to non-monetary financial institutions remains high. Growth in household loans, which declined slightly early in the year, also remains high. The volume of loans to non-financial corporations is smaller year on year, but this is largely a consequence of monthly fluctuations, which have a more pronounced impact on year-on-year movements owing to the modest lending activity. On the liability side, deposits by domestic non-banking sectors are rising further, while liabilities to foreign banks continue to fall, at EUR 1.9 billion accounting for less than 5% of the banking system’s total assets. The decline in the share of arrears of more than 90 days intensified somewhat, seasonally, at the end of the year. While non-performing claims against non-residents dropped in particular, those against domestic enterprises also fell slightly more than in previous months.

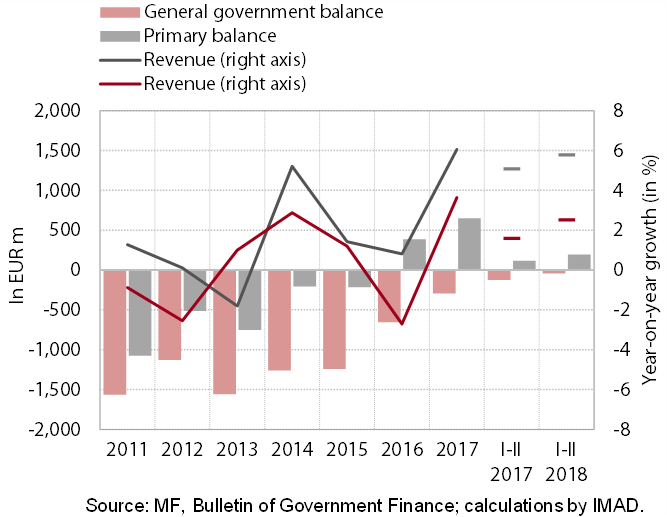

The general government deficit was lower year on year in the first two months of 2018. The main factors behind continued high year-on-year growth in tax revenues and revenues from social contributions were favourable labour market trends, high consumer confidence, improving business results and last year’s increase in the corporate income tax rate. Owing to the one-off inflow in 2017, non-tax revenues were more than a quarter lower year on year; payments from the EU budget were also lower than in the same period last year. The growth of total general government revenue (5.8%) was nevertheless still significantly higher than that of general government expenditure (2.5%). The deficit of the consolidated balance of public finances (EUR 44 million) was therefore considerably lower year on year. General government expenditure was up year on year primarily due to higher pensions, sickness benefits, payments into the EU budget and compensation of employees. Investment expenditure was significantly lower than in the same period last year; interest payments were also somewhat lower.