Charts of the Week

Charts of the week from 23 to 27 March 2026: economic sentiment, turnover in trade and real estate

Following a marked deterioration in February, the economic sentiment indicator improved slightly month-on-month in March, supported by improved confidence in retail trade and in manufacturing and services. However, compared with March last year, overall economic sentiment was lower, as all confidence indicators declined except for consumer confidence. After increasing in the fourth quarter of last year, real turnover in most trade sectors declined in January and was also lower year-on-year. Growth in dwelling prices moderated last year amid increased transaction volumes.

Economic sentiment, March 2026

The economic sentiment indicator improved slightly month-on-month in March, following a marked deterioration in February. Having strengthened since September last year, the indicator declined sharply in February, falling below its year-earlier level for the first time since August 2025 and dropping below its long-term average. In March, it edged up slightly month-on-month, supported by stronger confidence in retail trade, manufacturing and services. Confidence in construction deteriorated further, while consumer confidence remained unchanged from the previous month. Overall, economic sentiment in March remained weaker than a year earlier, with all confidence indicators lower except for consumer confidence.

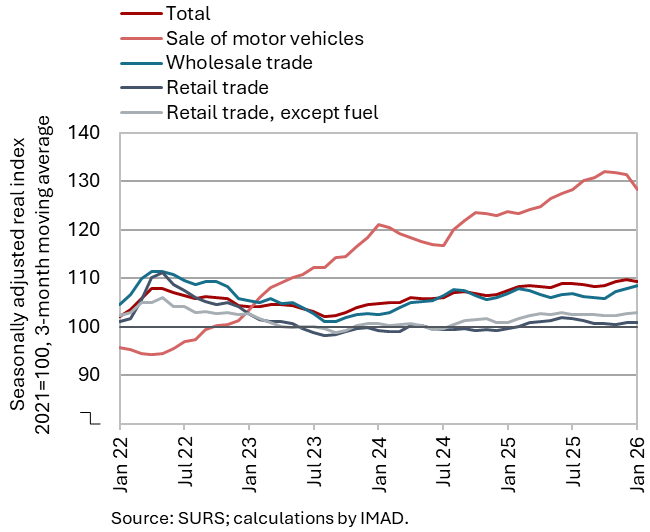

Turnover in trade, January 2026

After increasing in the fourth quarter of last year, real turnover in most trade sectors declined in January and was also lower year-on-year. In motor vehicle sales, turnover decreased for the third consecutive month, following strong growth up to October last year. After relatively strong growth in December, retail trade in food and non-food products also declined. Wholesale turnover remained broadly unchanged from its Q4 2025 level, when it had strengthened considerably (seasonally adjusted). Year-on-year, sales declined across all trade sectors except retail trade in non-food products. The largest decline was recorded in motor vehicle sales, which, amid a 9% increase in sales of new passenger cars, recorded the fastest real growth last year (7%).

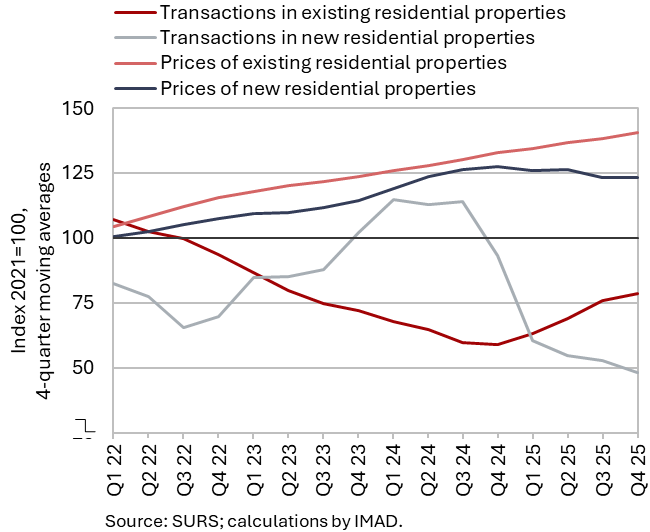

Real estate, Q4 2025

Growth in dwelling prices moderated last year amid higher transaction volumes. On average in 2025, prices increased by 4.3%, down from around 7.5% in 2023 and 2024. Prices of existing dwellings, where the number of transactions increased by one-third from the lowest level recorded in 2024, rose by 5.8% year-on-year (by 7.4% in the previous year). By contrast, prices of newly built dwellings were lower than a year earlier (by 3.3%, following growth of just over 10% on average in 2024), although these accounted for only 4% of all transactions. Average dwelling prices were 110.6% higher than in 2014, when they reached their trough. Over the same period, consumer prices increased by 29.7%, while the average net wage rose by almost 60%.